One of the things that struck me most during our recent pieces on startup employee option plans is how things that impact the value of those options aren’t well understood, even if communicated or known at the onset. Many people reported feelings of a sort of “sticker shock” (or reverse!) on leaving their first startup. Meanwhile, founders genuinely want to do right by their employees and other stakeholders — but owning part of a company isn’t a static, fixed thing; it’s fluid, and there are a number of factors that could change the overall ownership equation over time.

Part of the problem is the sheer amount and complexity of information required to understand equity and ownership in the first place. Which is why many founders are working hard to build trust while navigating shifting ownership — their own, their employees’, their co-founders’, their investors — along the way, often dedicating resources to educating folks. There are also some great overviews, guides, and templates out there now that cover how options and compensation works. So we thought we’d share more here about how the economics behind startup options and ownership works…

Cap Table

The capitalization or “cap” table reflects the ownership of all the stockholders of a company — that includes the founder(s), any employees who hold options, and of course the investors. For most people to understand how much of a company they actually own, all they really need is the fully diluted share count, the broader breakout of ownership among different classes of shareholders, and a couple other details. The fully diluted share count (as opposed to the basic share count) is the total of all existing shares + things that might eventually convert into shares: options, warrants, un-issued options, etc.

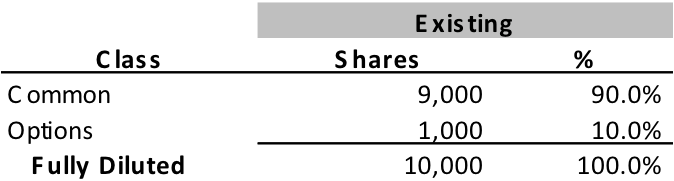

Let’s introduce a hypothetical example that we’ll use throughout this post. Here’s a new company that has no outside investors, and existing stock allocated as follows:

If someone were offered 100 options, those shares would come out of the 1,000-share option pool, and so they’d own 100/10,000 or 1.0% of the fully diluted capitalization of the company.

But that’s just the starting point of ownership, because any analysis of percent ownership in a company only holds true for a point in time. There are lots of things that can increase the fully diluted share count over time — more options issued, acquisitions, subsequent financing terms, and so on — which in turn could decrease the ownership percentage. Of course, people may also benefit from increases in options over time through refresher or performance grants, but changes in the numerator will always mean corresponding changes in the denominator.

Financing History

For each financing round (of convertible preferred stock), there’s an original issue price and a conversion price:

- The original issue price is just what it says: the price per share that the investor paid for its stock. This price tells us what various financial investors believe the value of the company was at various points in time.

- The conversion price is the price per share at which the preferred stock will convert into common stock. Remember, “preferred” stock is usually held by investors and has certain corporate governance rights and liquidation preferences attached to it that the rest of the “common” stock does not have.

In most cases, the conversion price will equal the original issue price, though we’ll share later below where the two can diverge.

The exercise price of employee options — the price per share needed to actually own the shares — is often less than the original issue price paid by the most recent investor, who holds preferred stock. How much of a difference in value depends upon the specific rights and the overall maturity of the company, and an outside valuation firm would perform what’s called a 409a Valuation (named for a specific section in the IRS tax code) to determine the precise amount.

Dilution

Dilution is a loaded word and tricky concept. On one hand, if a company is raising more money, it’s increasing the fully diluted share count and thus “diluting” or reducing current owners’ (including option-holding employees’) ownership. On the other hand, raising more money helps the company execute on its potential, which could mean that everyone owns slightly less, but of a higher-valued asset. After all, owning 0.09% of a $1 billion company is better than owning 0.1% of a $500 million company.

If the company increases the size of the option pool to grant more options, that too causes some dilution to employees, though hopefully (1) it’s a sign of the company’s being in a positive growth mode, which increases overall value of the shares owned (2) it means that employees might benefit from those additional option grants.

Let’s return to the example we introduced above, only now our company has raised venture capital. In this Series A financing, the company got $10 million from investors at an original issue price of $1,000 per share:

The fully diluted share count increases by the amount of the new shares issued in the financings; it’s now 20,000 shares fully diluted. This means the employee’s 100 options now equate to an ownership in the company of 100/20,000, or 0.5% — no longer the 1% she owned when she first joined. But… the value of that ownership has increased significantly: Because the price of each share is now $1,000, her stake is equal to 100 shares * $1,000/share, or $100,000.

While not all dilution is equal, there are cases where dilution is dilution — and it involves the anti-dilution protections that many investors may have. The basic idea here is that if the company were to raise money in a future round at a price less than the current round in which that investor is participating, the investor may be protected against the lower future price by being issued more shares. (The amount of additional shares varies depending on a formula.)

Most anti-dilution protections — often called a weighted average adjustment — are less dilutive to employees because they’re more modest in their protection of investors. But there’s one protection that does impact the other shareholders: the full ratchet. This is where the price that an investor paid in the earlier round is adjusted 100% to equal the new (and lower) price being paid in the current round. So if the investor bought 10 million shares in the earlier round at a price of $2 per share and the price of the current round is $1 per share, they’re now going to get double the number of shares to make up for that, equaling a total of 20 million shares. It also means the fully diluted share count goes up by an additional 10 million shares; all non-protected shareholders (including employees) are now truly diluted.

By the way, this isn’t just theoretical: We saw the effects of such a full ratchet in the Square IPO, where the Series E investors were issued additional shares because the IPO price was half the price at which those investors had originally purchased their shares.

Ideally, anti-dilution protections wouldn’t come into play at all: That is, each subsequent round of financing is at a higher valuation than the prior ones because the company does well enough over time, or there aren’t dramatic changes to market conditions. But, if they do come into play, there’s a “double whammy” of dilution — from both the anti-dilution protection (having to sell more shares, thus increasing the denominator of fully diluted share count) as well as the lower valuation.

Liquidation Preferences

Some investors may also have liquidation preferences that attach to their shares. Simply put, a liquidation preference says that an investor gets its invested dollars back first — before other stockholders (including most employees with options) — in the case of a liquidity event such as the sale of the company.

To illustrate how such a preference works, let’s go back to our example, only now assume the company was sold for $100 million. Our Series A investor — who invested $10 million in the company and owns 50% of the business — could choose to get back its $10 million in the sale (liquidation preference), or take 50% of the value of the business (50% * $100 million = $50 million). Obviously, the investor will take the $50 million. That would leave $50 million in equity value to then be shared by the common and option holders:

Given the high sale price for the company in this example, the liquidation preference never came into play. It would, however, come into play under the following scenarios:

Scenario 1. If the sale price of a company is not sufficient to “clear” the liquidation preference, so the investor chooses to take its liquidation preference instead of its percentage ownership in the business.

Let’s now assume a $15 million sale price (instead of the $100 million) in our example. As the table below illustrates, our Series A investor will elect to take the $10 million liquidation preference because its economic ownership (50% * $15 million = $7.5 million) is less than what it would get under the liquidation preference. That leaves $5 million (instead of the $50 million) for the common and option holders to share.

Scenario 2. When a company goes through several rounds of financing, each round includes a liquidation preference. At a minimum the liquidation preference equals the total capital raised over the company’s lifetime.

So, if the company raises $100 million in preferred stock and then sells for $100 million, there’s nothing left for anyone else.

Scenario 3. There are various flavors of liquidation preference that can come into play depending on the structure of the terms. So far, we’ve been illustrating a 1x non-participating preference — the investor has to make a choice to take only the greater of 1x their invested dollars or the amount they would otherwise get based on their percentage ownership of the company.

But some investors do more than 1x — for instance, a 2x multiple would mean that the investor now gets 2x of their invested dollars off the top. The non-participating can also become “participating”, which means that in addition to the return of invested dollars (or multiple thereof if higher than 1x), the investor also gets to earn whatever return their percentage ownership in the company implies. The impact of this on other stockholders can be significant.

To isolate the effects of these terms, let’s first look at what happens when our Series A investor gets a 2x liquidation preference. In the $100 million sale scenario, that investor will still take its 50% since $50 million is greater than the $20 million (2 x $10 million liquidation preference) it’s otherwise entitled to. The common and option holders are no worse off than they were when our investor had only a 1x liquidation preference:

But, if the sale price were the much lower $15 million, the investor is going to capture 100% of the proceeds. Its 2x liquidation preference still equals $20 million, but there’s only $15 million to be had, and all of that goes to the investor. There’s nothing left for common and option holders:

Finally, let’s take a look at what happens when we have participating preferred, colloquially referred to as “double dipping.”

In our $100 million sale scenario, the Series A investor not only gets its $10 million liquidation preference, but also gets to take its share based on its percentage ownership of the company. Thus, the investor gets a total of $10 million (its liquidation preference) plus 50% of the remaining $90 million of value, or $55 million in total. Common and option holders get to share in the remaining $45 million of value:

In the $15 million scenario, the common and option holders get even less. Because the Series A investor gets its $10 million in preference plus 50% of the remaining $5 million in proceeds, for a total of $12.5 million, only $2.5 million is left for the rest of the shareholders:

IPOs

There are a bunch of non-economic factors — legal, tax, and corporate governance-related issues — that we aren’t addressing here: which stockholders are required to approve certain corporate actions like selling the company; raising more capital; and so on. They’re important considerations, but we’re focusing here only on economic factors in options and ownership.

However, there is one factor still worth paying attention to because it’s really an economic issue cloaked as a governance issue — the IPO auto convert. This is the language that determines who gets to approve an IPO. In most cases, the preferred stockholders, voting as a single class of stock, get to approve an IPO: Add up all the preferred stockholders together and the majority wins. This is a good check on the company as it ensures one person/one vote, though each preferred stockholder has a say proportional to their economic ownership of the company.

Sometimes, however, different investors can exercise control disproportionate to their actual economic ownership. This typically comes into play when a later-stage investor is concerned that the company might go public too soon for them to earn the type of financial return they need having entered late. In such cases, that investor may require that the company get its approval specifically for an IPO, or if the price of the IPO is less than some desired return multiple (like 2-3x) on its investment.

And that’s how a seemingly governance-only question quickly turns into an economic one: If an investor’s approval is required for an IPO, and that investor is not happy with its return on the IPO, this control can become a backdoor way for the investor to agitate for greater economic returns. How would they do this? By asking for more shares (or lowering the conversion price at which its existing preferred shares convert into common). This increases the denominator in the fully diluted share count.

To be clear, none of this is to suggest nefarious behavior on the part of later-stage investors. After all, they’re providing needed growth capital and other strategic value to the business, and are looking to earn a return on capital commensurate with the risk they’re taking. But it’s yet another factor to be aware of among all the other ones we’re outlining here.

ISOs vs non-quals (and exercise periods)

Besides the financing and governance factors that could impact option value, there are also specific types of options that could affect the economic outcomes.

In general, the most favorable type of options are incentive stock options (ISOs). With an ISO, someone doesn’t have to pay tax at the time of exercise on the difference between the exercise price of the option and the fair market value (though there are cases where the alternative minimum tax can come into play). Basically, ISOs mean that startup employees can defer those taxes until they sell the underlying stock and, if they hold it for 1 year from the exercise date (and 2 years from the grant date), can qualify for capital gains tax treatment.

Non-qualified options (NQOs) are less favorable in that someone must pay taxes at the time of exercise, regardless of whether they choose to hold the stock longer term. Since the amount of those taxes is calculated on the exercise date, employees would still owe taxes based on the historic, higher price of the stock — even if the stock price were to later fall in value.

So then why don’t all companies only issue ISOs? Well, there are a few constraints on ISOs, including the legal limit of $100,000 of market value that can be issued to any employee within a single year (this means getting NQOs for any amount over $100,000). ISOs also have to be exercised within 90 days of the employee’s leaving the company. With more companies thinking about extending the option exercise period from 90 days to a longer period of time, companies can still issue ISOs — but if they’re not exercised within 90 days of exiting the company, they convert to NQOs regardless of the company’s exercise time, at least under current tax law.

M&A

One of the most frequently asked questions about options is what happens to them if a startup is acquired. Below are some possible scenarios, assuming four years to fully vest but the company decides to sell itself to another company at year two:

Scenario 1. Unvested options get assumed by the acquirer.

This means that, if someone is given the option to stay with the acquirer and choose to stay on, their options continue to vest on the same schedule (though now as part of the equity of the acquirer). Seems reasonable… Unless of course they decide this wasn’t what they signed up for, don’t want to work for the new employer, and quit — forfeiting those remaining two years of options.

Scenario 2. Unvested options get cancelled by the acquirer and employees get a new set of options with new terms (assuming they decide to stay with the acquirer).

The theory behind this is that the acquirer wants to re-incent the potential new employees or bring them in line with its overall compensation philosophy. Again, seems reasonable, though of course it’s a different plan than the one originally agreed to.

Scenario 3. Unvested options get accelerated — they automatically become vested as if the employee already satisfied her remaining two years of service.

There are two flavors of acceleration to be aware of here, single-trigger acceleration and double-trigger acceleration:

- In single trigger, unvested options accelerate based upon the occurrence of a single “trigger” event, in this case, the acquisition of the company. So people would get the benefit of full vesting whether or not they choose to stay with the new employer.

- In double trigger, the occurrence of the acquisition alone is not sufficient to accelerate vesting. It must be coupled with either the employee not having a job offer at the new company, or having a role that doesn’t quite match the one they had at the old company.

Note, these are just general definitions. There are specific variations on the above triggers: whether everything accelerates or just a portion; whether people accelerate to some milestone, such as their one-year cliffs; and so on — but we won’t go through those here.

Not surprisingly, acquirers don’t like single triggers, so they’re rare. And double triggers give the acquirer a chance to hold on to strong talent. Still, it’s very unusual for most people to have either of the above forms of acceleration. These triggers are typically reserved for senior executives where it’s highly likely in an acquisition scenario that they won’t — or literally can’t (not possible to have two CFOs for a single company for example) be offered jobs at the acquirer — and thus wouldn’t have a chance to vest out their remaining shares.

The simple way to think about all this is that an acquirer typically has an “all-in price” — which includes up-front purchase price, assumption of existing options, new option retention plans for remaining employees, etc. — that it is willing to pay in the deal. But how the money ultimately gets divided across these various buckets can sometimes diverge from what the initial option plan documents dictate as acquisition discussions evolve.

* * *

As mentioned earlier, anything related to compensation and ownership boils down to building and navigating trust — whether it’s through education, communication, or transparency. There’s also an important S.E.C. rule that is in play here: Rule 701, the exemption for issuing employee stock options. This rule says that up to about $5 million in annual option issuances, a company must provide the recipient a copy of the options plan; and then once a company goes beyond the $5 million annual limit, it must also provide a summary of the material terms of the plan, risk factors, and two years worth of GAAP financial statements. Which is great.

But times have changed, and the 701 requirements that were put into effect April 1999 have failed to keep pace. Companies are now staying private longer and are therefore raising more capital, often from new entrants to venture investing with more complicated terms. So simply reviewing a company’s last two years of financial statements doesn’t say much about the ultimate potential value of options. Rule 701 should be updated to better reflect the information people need to understand options.

The good news is that if a company goes public, all of the above different rights that preferred stockholders have go away because everyone’s shares convert into common shares. There may still be different classes of common stock (such as dual classes with different voting rights to protect founder-driven long-term innovation) — but those don’t impact an individual’s economics.

Startup outcomes are, by definition, unpredictable. Every startup is unique, every situation has unknown variables, and new data will always change the economic outcomes. Working at a startup means getting in early for something that has yet to be proven, which means it could have great risks … and potentially, great rewards.