One of the most common pricing questions we get from late-stage SaaS companies is: should we switch to a usage-based pricing model (also known as consumption-based pricing)?

Often, these companies have an existing subscription model, and usage-based pricing sounds like it would further align their incentives with their customers’. After all, the more their customers use their product, the more revenue they capture.

But just because usage-based pricing has worked for other companies doesn’t necessarily mean it’ll work for yours.

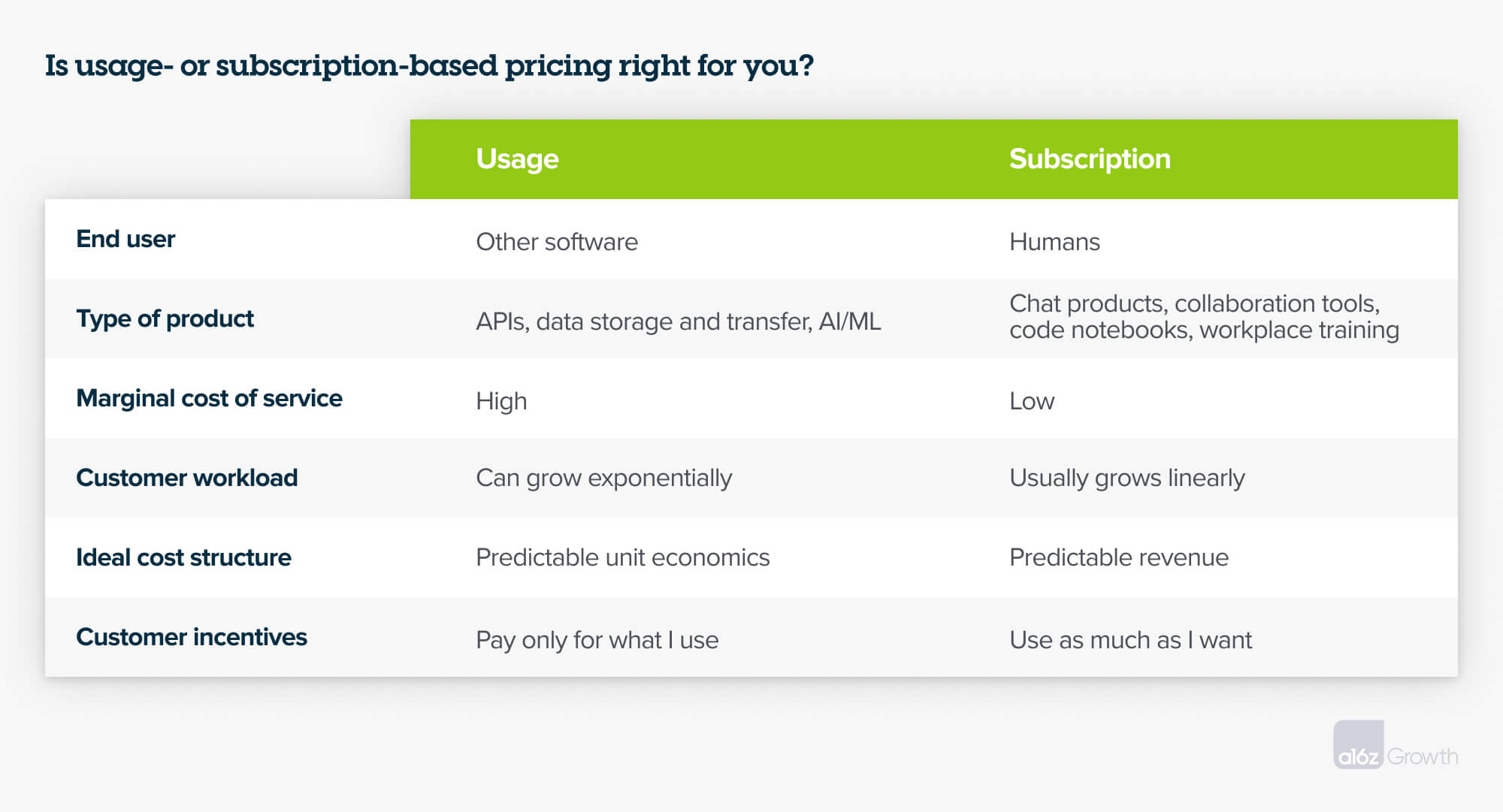

Our rule of thumb: usage-based pricing generally works best for SaaS products whose end user is other software, while subscription-based models tend to work best for SaaS products with human end users.

This is usually because software-to-human products make employees more productive (through collaboration, training, etc.), while software-to-software products tend to power their customers’ products or internal systems.

With software-to-software products, customers want to get access to the products, start using it, and only pay for what they use. These products typically have great product telemetry data, so it’s easy for these companies to set up processes that track, bill, and even cap that usage—which ultimately leads to smoother adoption processes, strong net dollar retention, and a robust land-and-expand motion.

But what removes friction for software-to-software customers actually creates friction for software-to-human customers. The average enterprise has over 100 SaaS apps, and no human user wants to monitor their usage to make sure their IT spend doesn’t surge past a given limit. Individual users also don’t like to be nickel-and-dimed for what they use: imagine if a CRM charged sales reps every time they created an opportunity! That’s why software with human end users typically benefits from subscription models.

There’s also a natural limit to how much a human user will consume a certain amount of software: they can only watch so many training videos or create so many collaborative documents. Use of software-to-software products, like code testing or data transfer, can grow exponentially, however, so usage-based pricing can better capture the value of those kinds of workloads.

And from a vendor perspective, software-to-software products also generally have a higher marginal cost of service than software-to-human products, so charging by usage sets up stronger unit economics that can cover those costs. Imagine the converse: you run an infrastructure company that bills by subscription and, all of the sudden, your customers’ usages skyrocket—it becomes much less cost-effective to serve them.

That said, this isn’t a hard-and-fast rule.

While we’ve outlined an either/or logic above, in reality, pricing is often a spectrum. We often see companies offer hybrid subscription-and-usage pricing models depending on their cost structures, customer needs, or the nature of their product. Our rule of thumb should help you figure out whether to emphasize subscription or usage in your pricing model. And of course, AI is rapidly changing software, how we use it, and how we monetize and charge for it.

There are a lot of questions you’ll need to answer if you want to implement usage-based pricing in your business: how can you best predict usage for both you and your customers? What’s the role of your salesforce? How will you compensate your reps? How do you need to set up your company in order to operationalize a usage model? We’ll touch on all of these topics in forthcoming posts, but this rule of thumb should be a good first step in figuring out if switching to a usage-based model is something you want to consider.