This is a written version of a presentation by Divvy Homes CEO Adena Hefets at the a16z Summit in November 2019. You can watch a video version on YouTube.

I’d like to start by illustrating the importance of homeownership. My dad immigrated to the US in the late 1970s. When he and my mom decided to settle down and form a family, they tried to purchase a home. But when they went out to get a mortgage, they were denied. Fortunately, my parents were able to get seller financing. The house they purchased became the house we grew up in. You see, to my family, homeownership was everything. It was our only form of savings and our only investment vehicle. That was the way we built up wealth.

Homeownership is so core to the American dream. It represents safety, security, and family. However, homeownership is becoming increasingly difficult for many Americans to achieve. Thankfully, there are ways that homeownership is evolving.

The definition of homeownership used to be pretty clear: You own title to the property, you generally put significant equity into the home and, maybe you had a mortgage with the first lien position on the asset. Well, the definition of how we own and, ultimately, utilize assets now seems to be changing across a number of industries.

We first saw this with Uber and Lyft, which redefined what it meant to own or access a car. The utility of a car is ultimately to get you from point A to point B. And if someone could provide this utility in a cheaper and easier manner, well, maybe you didn’t need to own a car anymore. Same thing with Airbnb. Why own a beautiful vacation home when you can Airbnb it, instead? There’s a new guard for how consumers are thinking about large-dollar, fixed asset investments. They are solving for use, experience, and, ultimately, access. Why own an asset when you can access it?

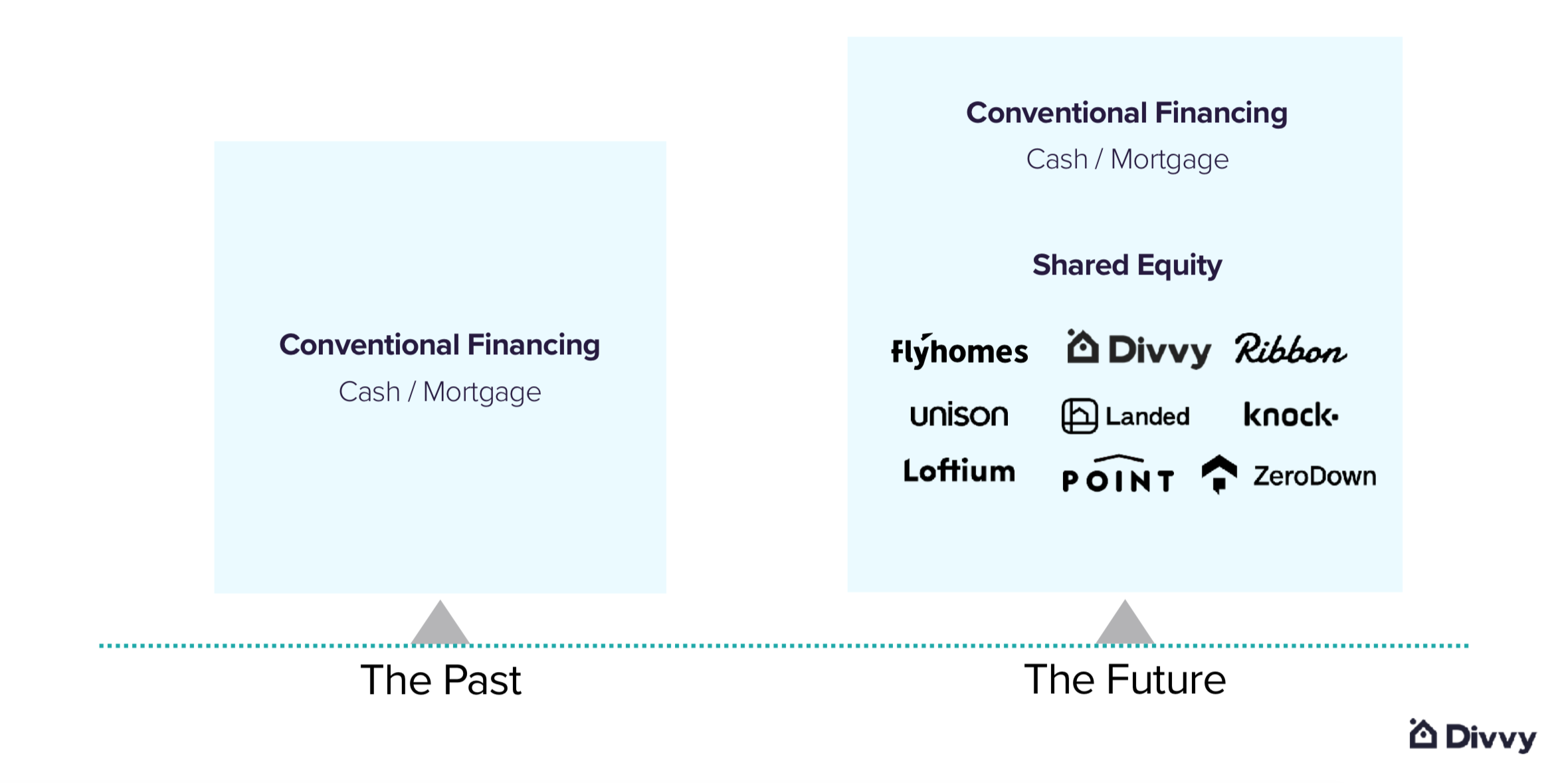

It’s no surprise that we’re seeing threads of this enter how we think about homeownership. We’ve gone from having one option for how you can purchase a home—a mortgage—to having a number of options.

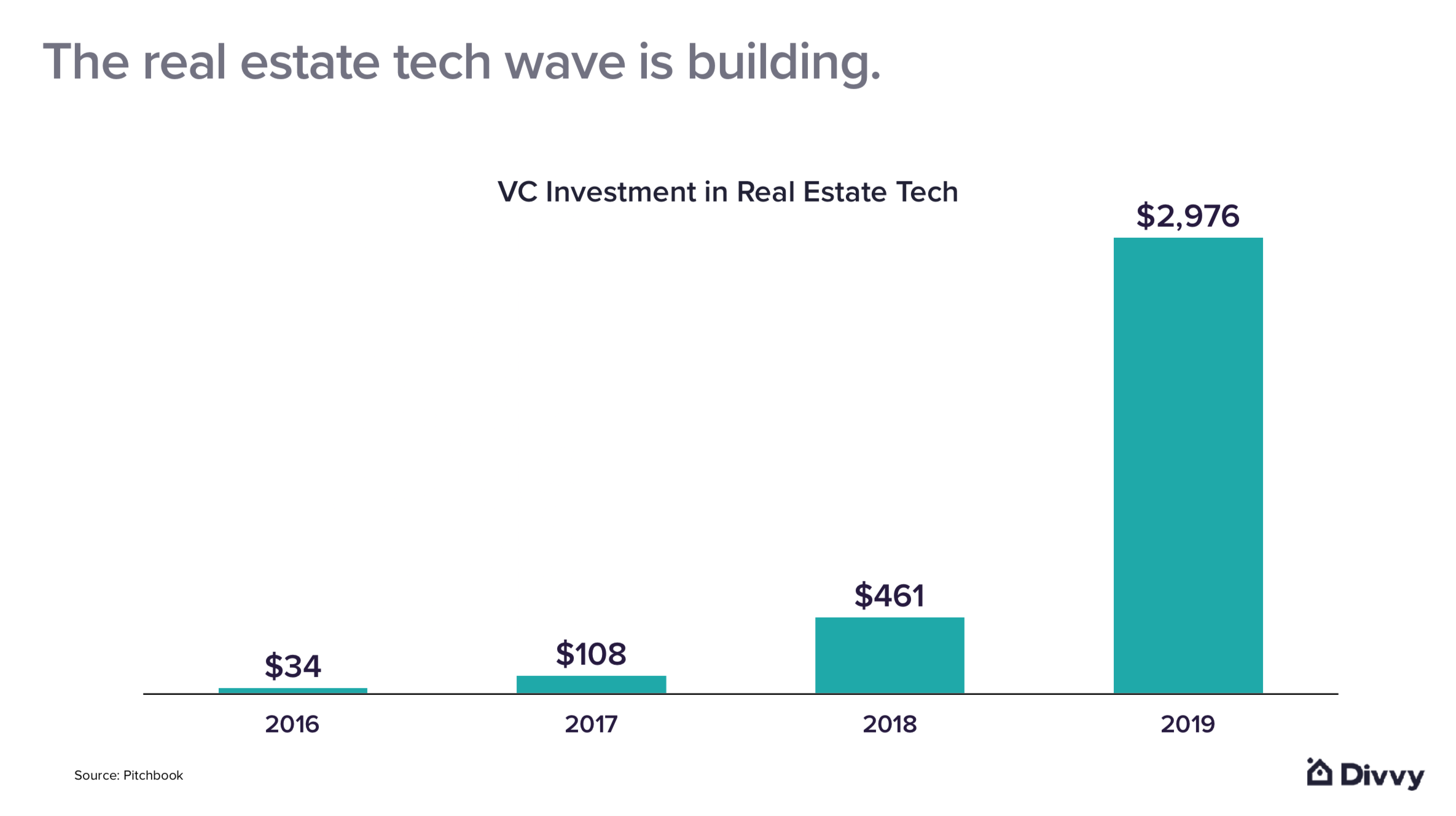

I call the companies at right the “new guard” of homeownership. They’re fundamentally rethinking how we access a home. The nuance here is that they’re not only providing use, experience, and access. They’re also adding a fourth dimension: a return on your financial investment. As you can see from this chart, we seem to be at the start of a wave that is going fundamentally change the way consumers purchase, and ultimately own, a home.

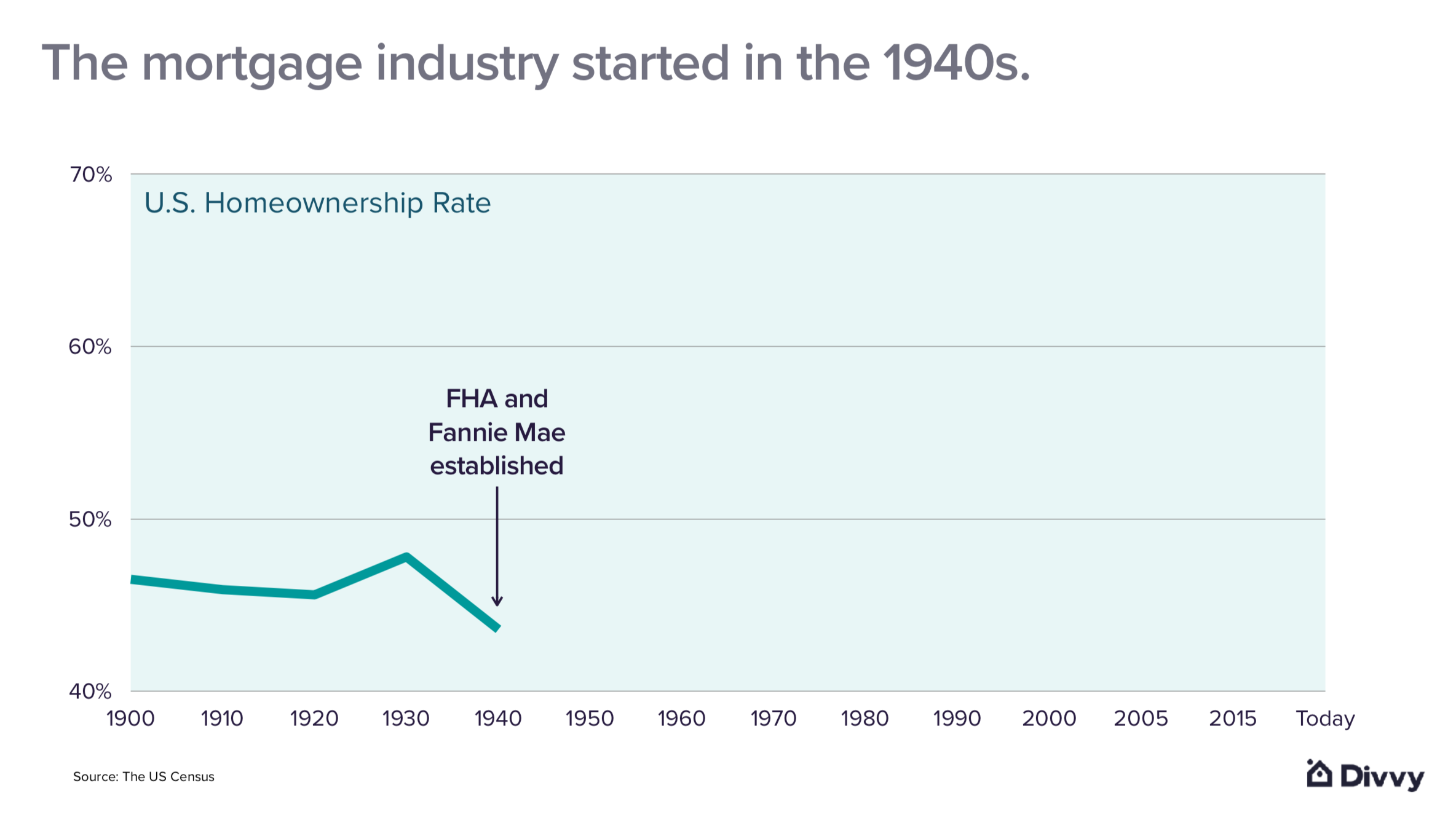

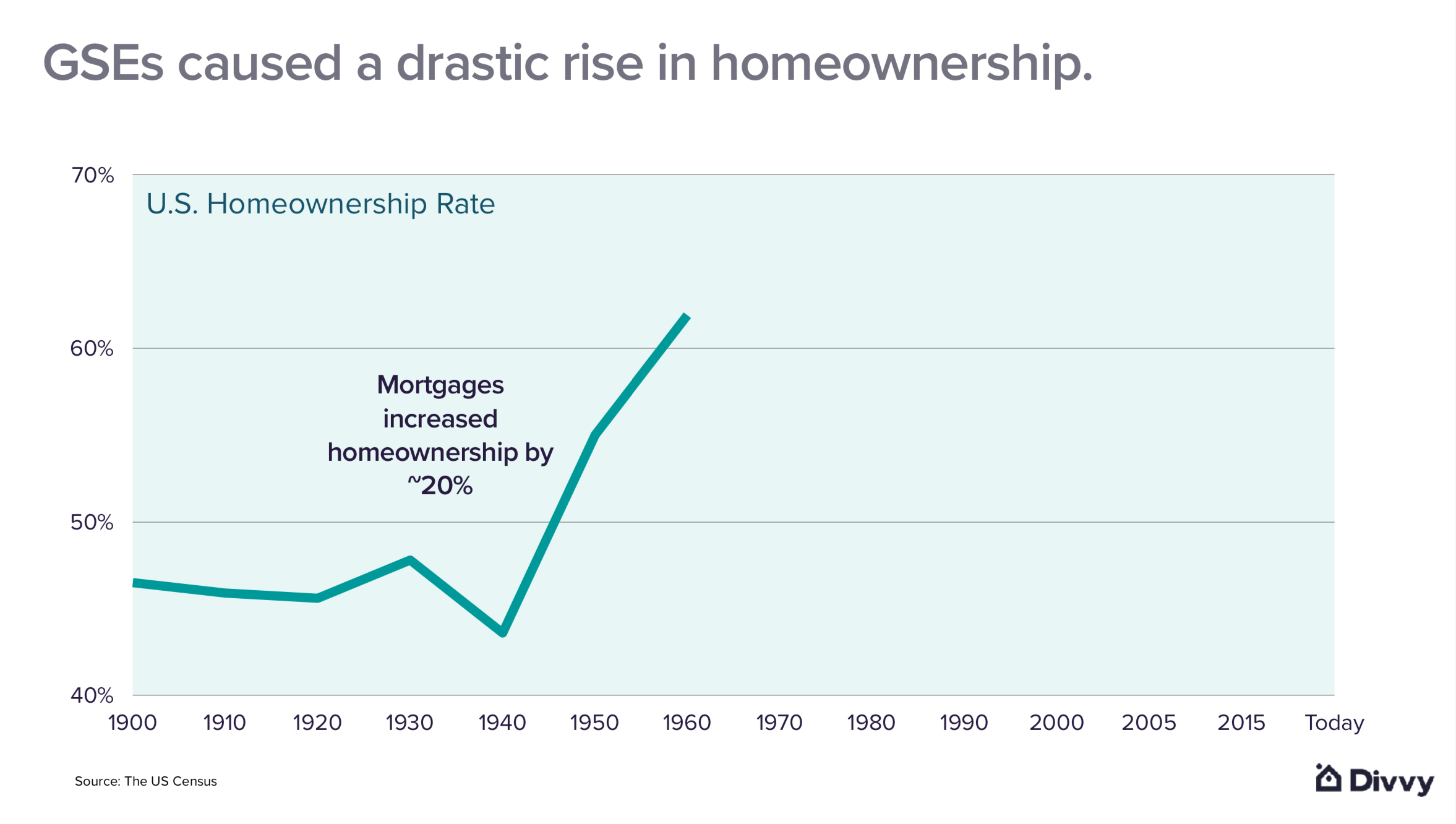

And understanding of history helps us to define the problem. This is the rate of US homeownership:

You can see that the rate was roughly in the mid-40s until the FHA was created. FHA is the Federal Housing Administration, which was formed in 1934, post Great Depression. Government wanted to be able to extend more credit, so the FHA created the fixed 30-year mortgage. They really lowered down payment requirements. This program was so successful that they ended up creating Fannie Mae. Fannie Mae’s job was to purchase those loans and sell them on the open financial markets. And voila, it worked! We saw about a 20 percent jump in the rate of homeownership over time.

From the government’s perspective, this was great. When you own a home you pay property taxes. It also helps create jobs and drives community development. From the customers’ perspective, it’s also really helpful. It’s a forced savings mechanism in an appreciating asset. And, by the way, you can live inside this asset. No one lives inside the S&P 500.

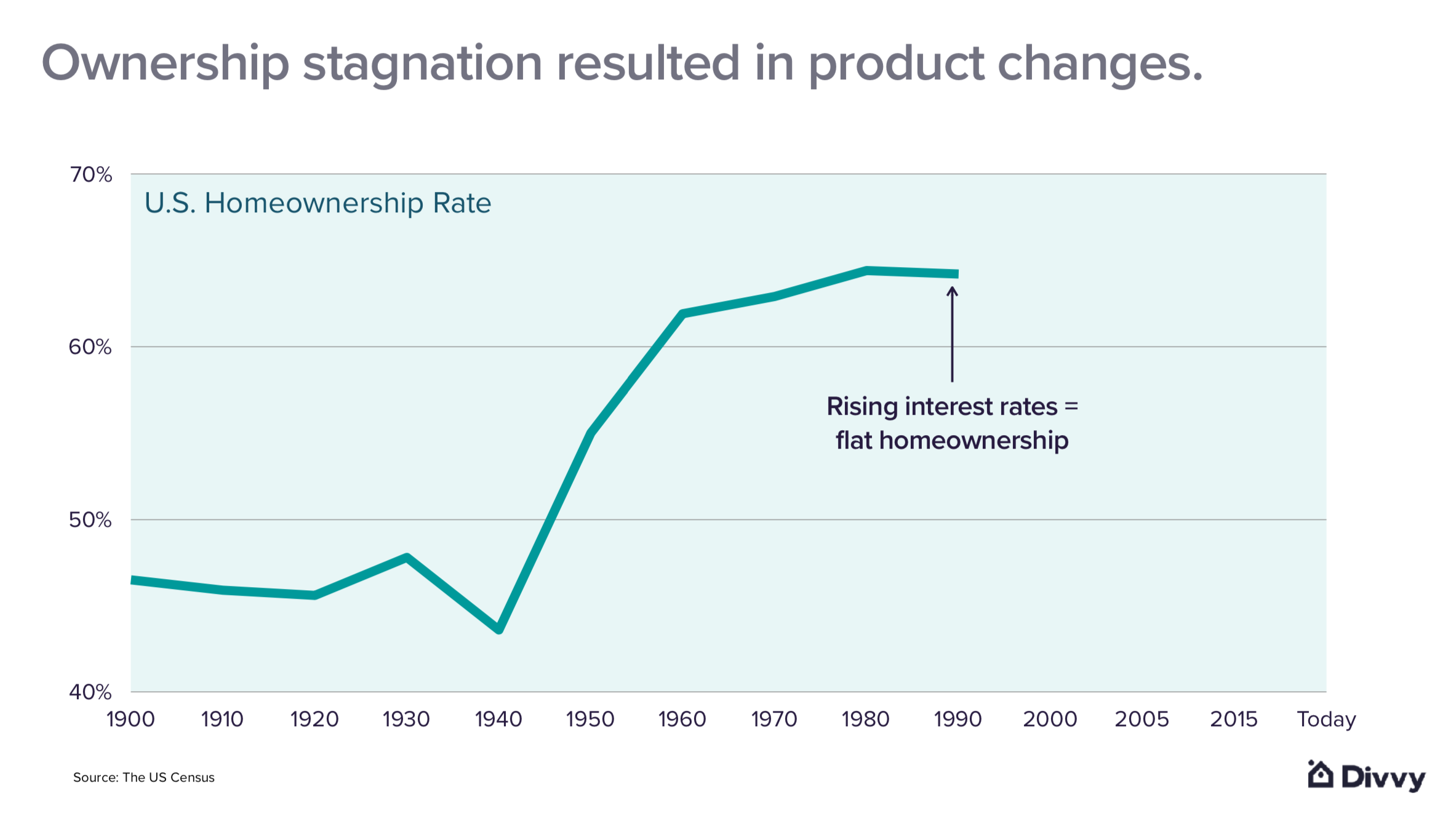

While this seemed really great, there was a period afterwards in which we saw the rate of homeownership stagnate. The 1990s had really high-interest rates, which meant that no one wanted to pay a 20 percent interest rate on a 30-year fixed-rate mortgage.

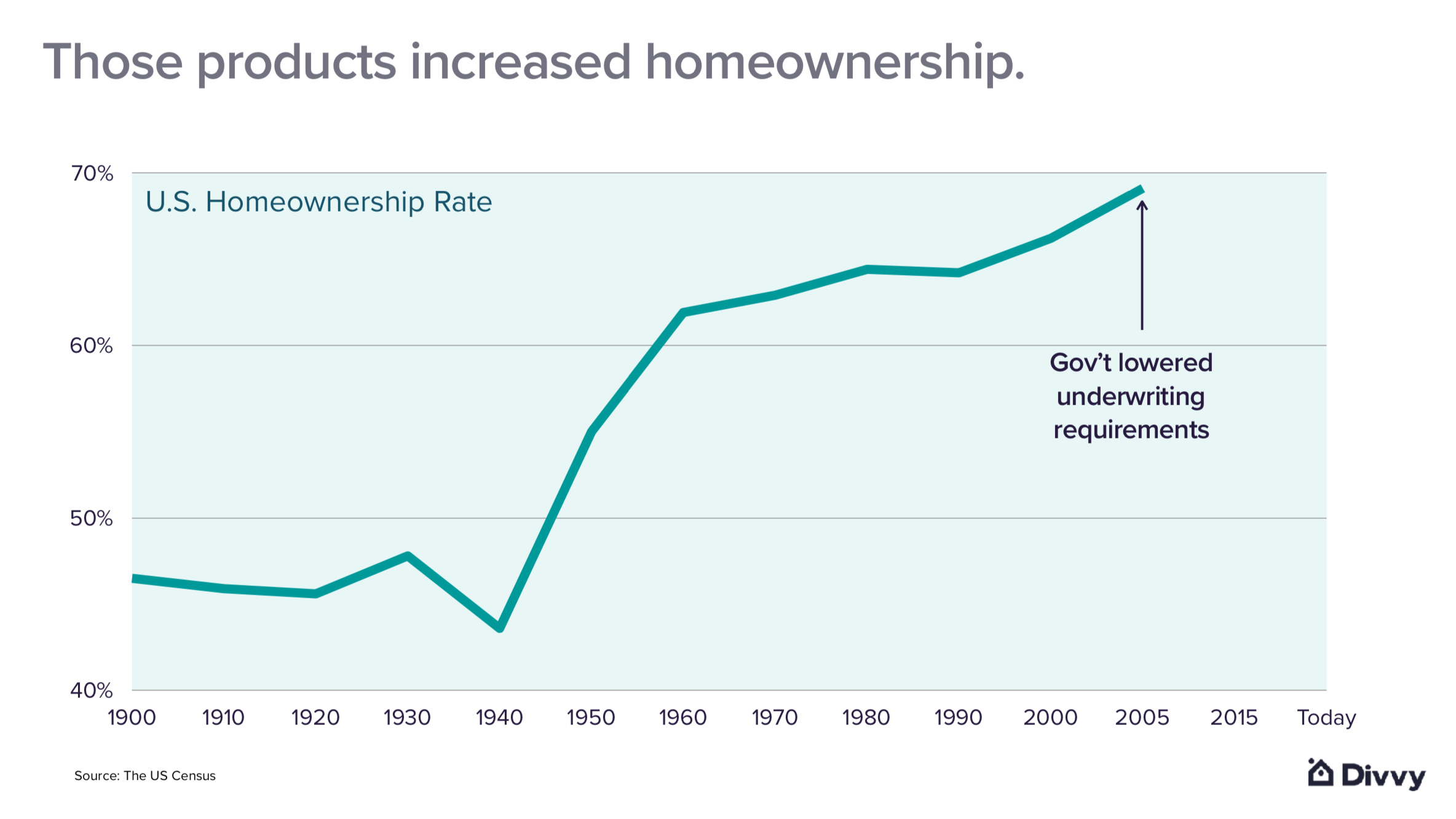

So the government said, “Hey, we did this once before. Let’s try doing it again.” It lowered underwriting requirements and started subprime lending. And the government achieved the desired impact: homeownership increased.

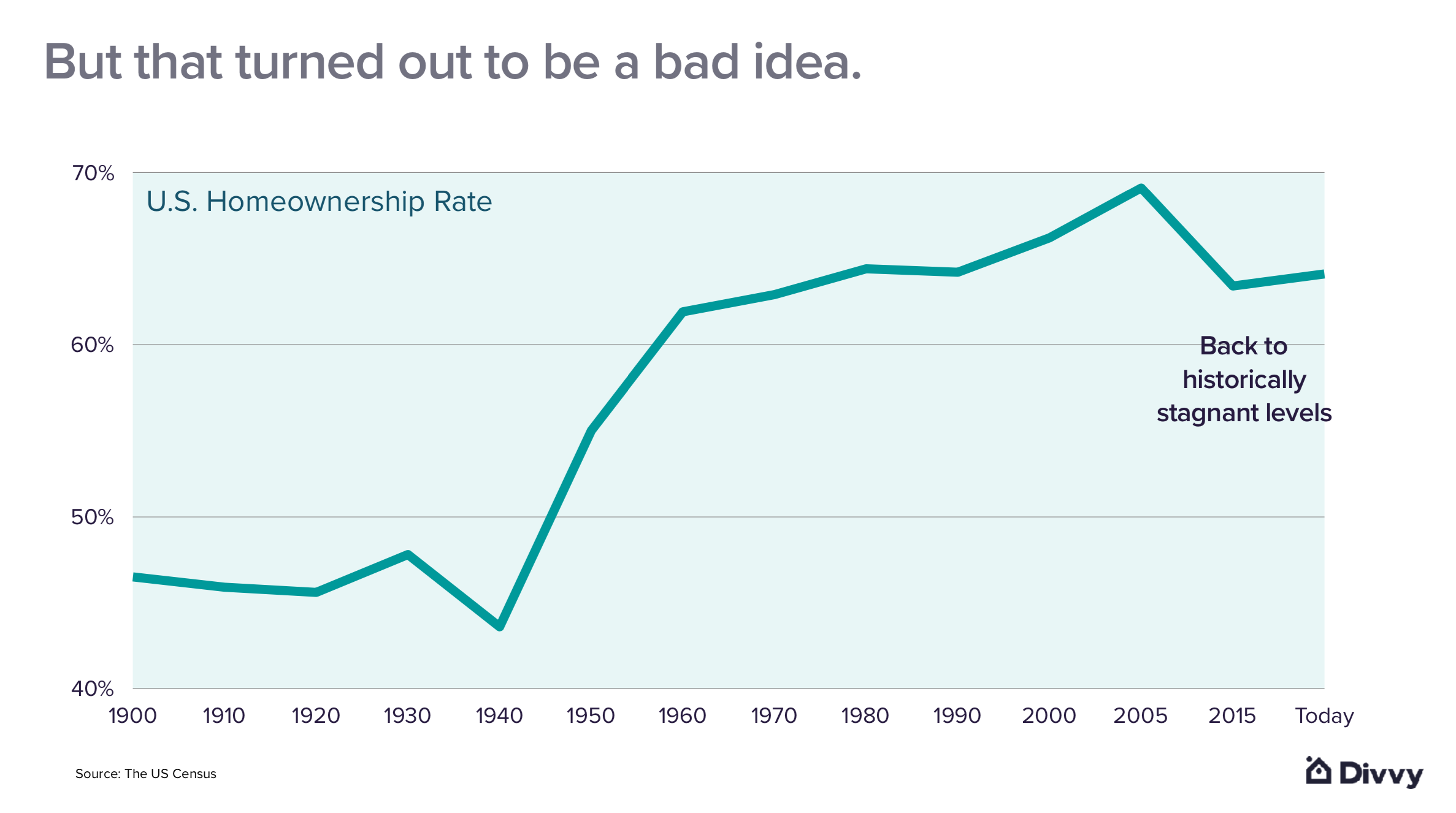

However, as a result, we lent to some consumers who weren’t creditworthy, which created a global, housing-led recession. Since then, the rate of homeownership has stayed roughly flat.

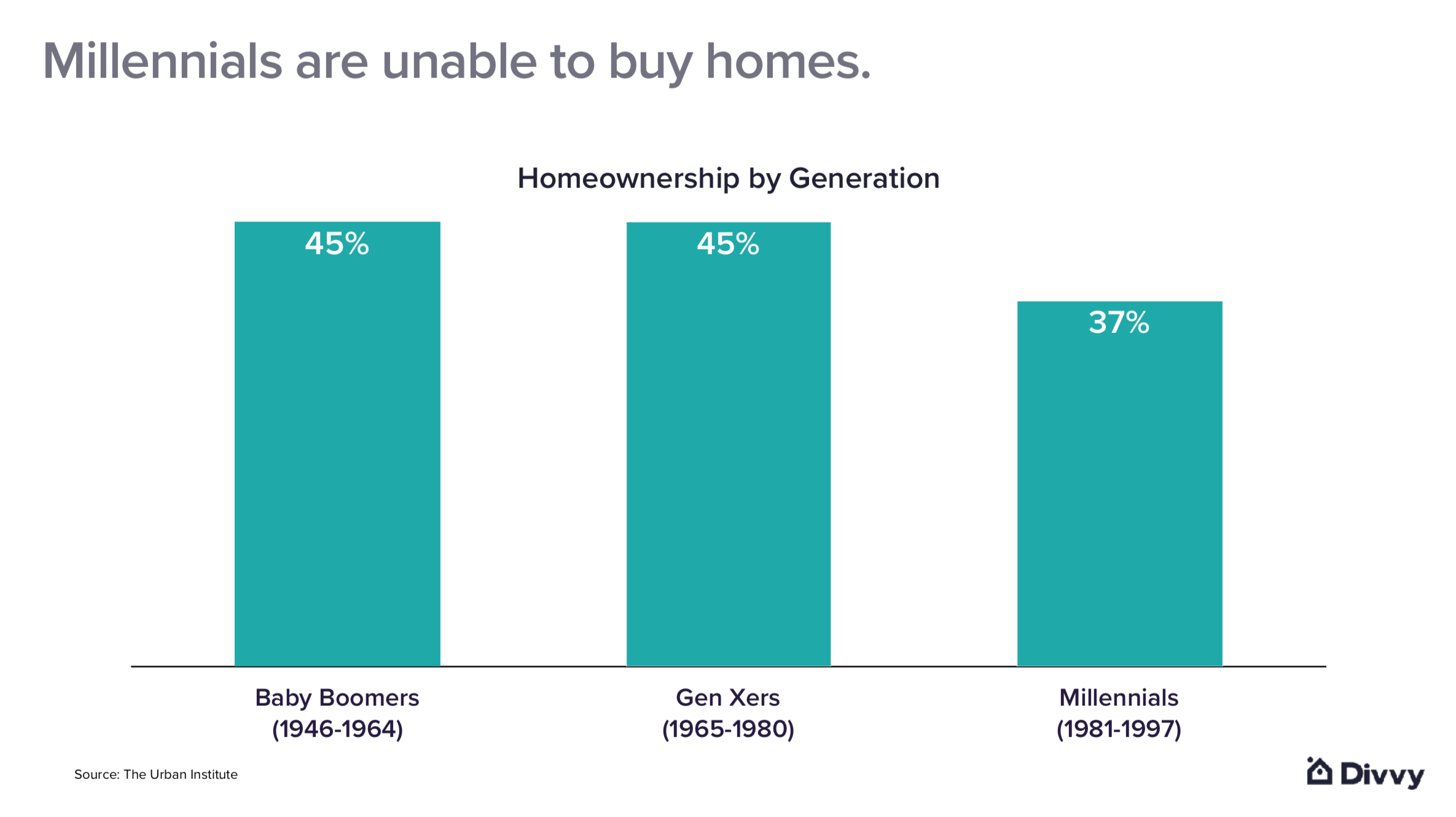

It would have been one thing if this decline in homeownership had impacted everyone consistently. But it disproportionately impacted two groups: millennials—those who are 25 to 35 years old—and first-time homebuyers. This chart is the rate of homeownership on a constant age basis. You can see that millennials today have a homeownership rate of about 37 percent, which is a much lower rate than Gen-Xers and baby boomers.

First-time homebuyers used to make about half of the offers on homes. Today, it’s only about a third. What’s even more depressing is that when first-time homebuyers do put offers on houses, 76 percent of the time they are providing less than the recommended 20 percent down payment.

All of this is happening despite the fact that we’re at the lowest 30-year fixed-mortgage rate in history. So, the government is fundamentally trying to drive up homeownership, but something isn’t working. And while I’d love to give you the perfect answer, like all really challenging questions, there seems to be a confluence of factors that is causing this:

-

Lack of Affordable Housing

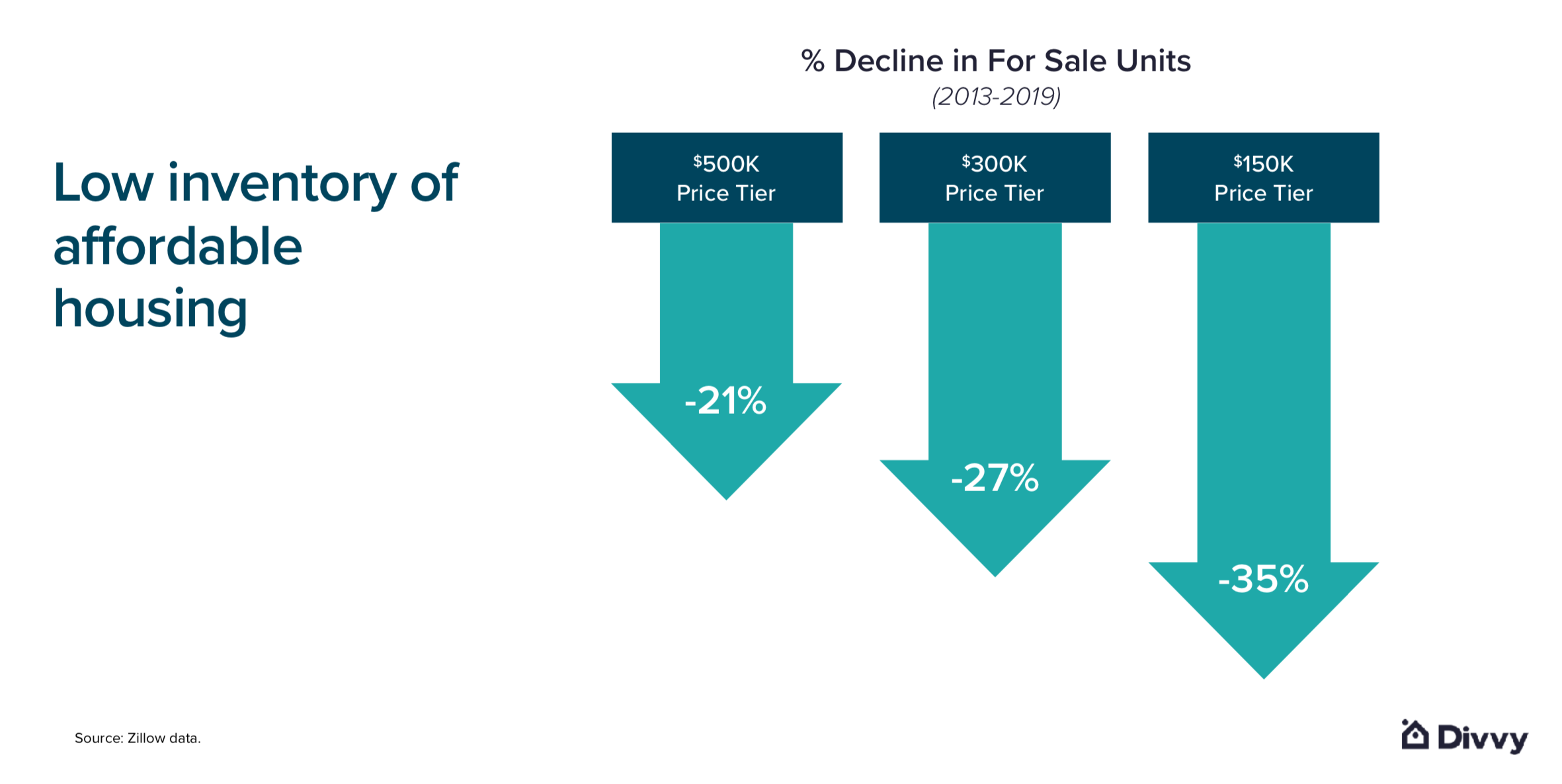

The chart below shows the percent decline in the number of for-sale units from 2013 to 2019. We’ve had a decline in the amount of inventory for sale, across the board. So, if you’ve ever felt like there’s a dearth of homes for sale, you’re not imagining it; it’s real. But if you look at the decline in the $150,000 price tier, you can see that the decline there was almost 35 percent, which was greater than the decline we saw in $300,000 homes and $500,000 homes.

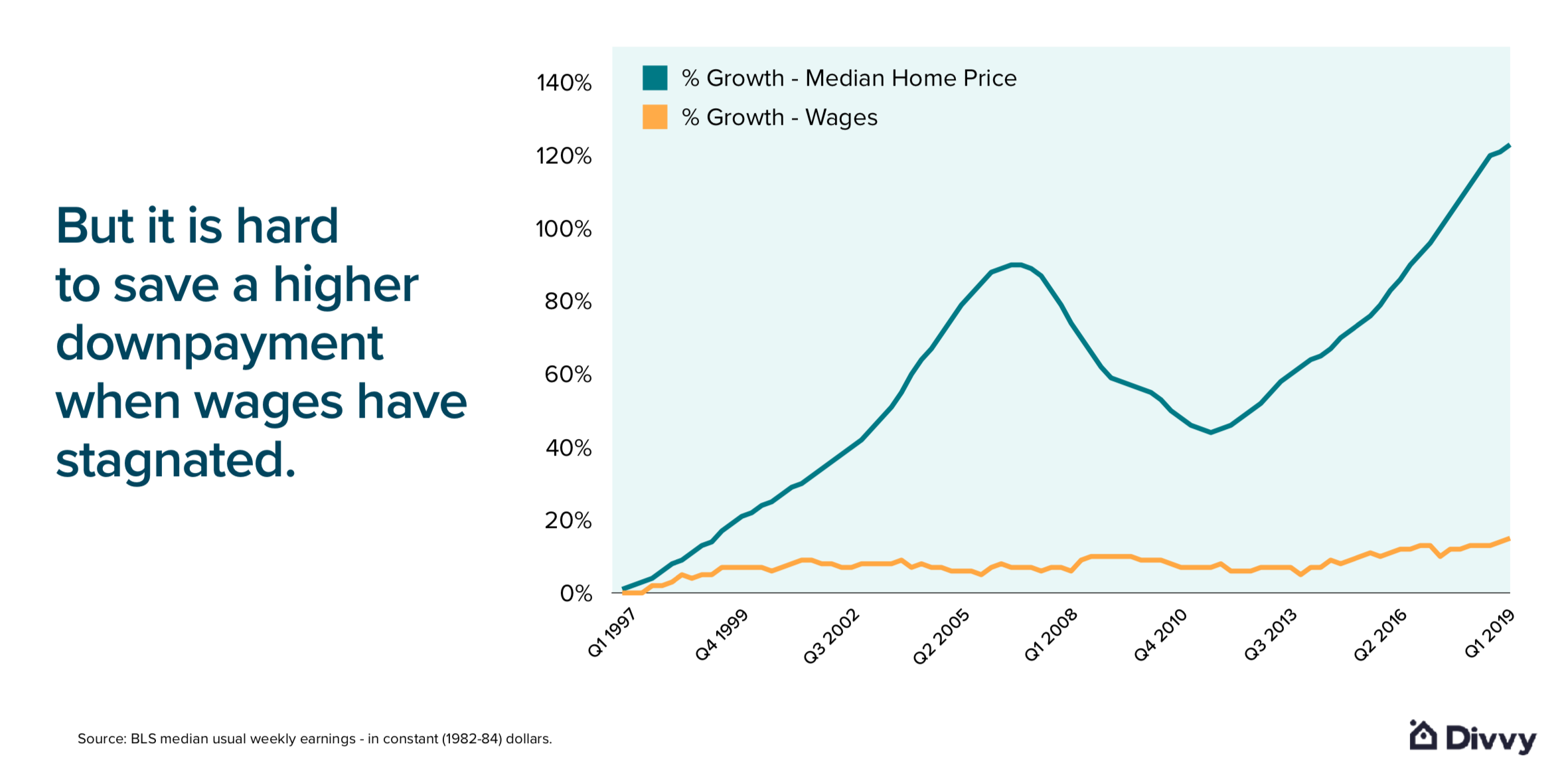

The median home price has grown by 120 percent since 1997. A higher median home price means that, in absolute dollars, you’re going to have to put more money down. But it’s really hard to put more money down when wages have stayed roughly flat. You’re asking the American consumer to save up more money.

-

Tighter underwriting requirements

We’ve gone from having a 690 average FICO score for mortgages to about a 740 average FICO today. While this might not seem like a tremendous jump, it actually cuts out about 20 percent of US consumers.

-

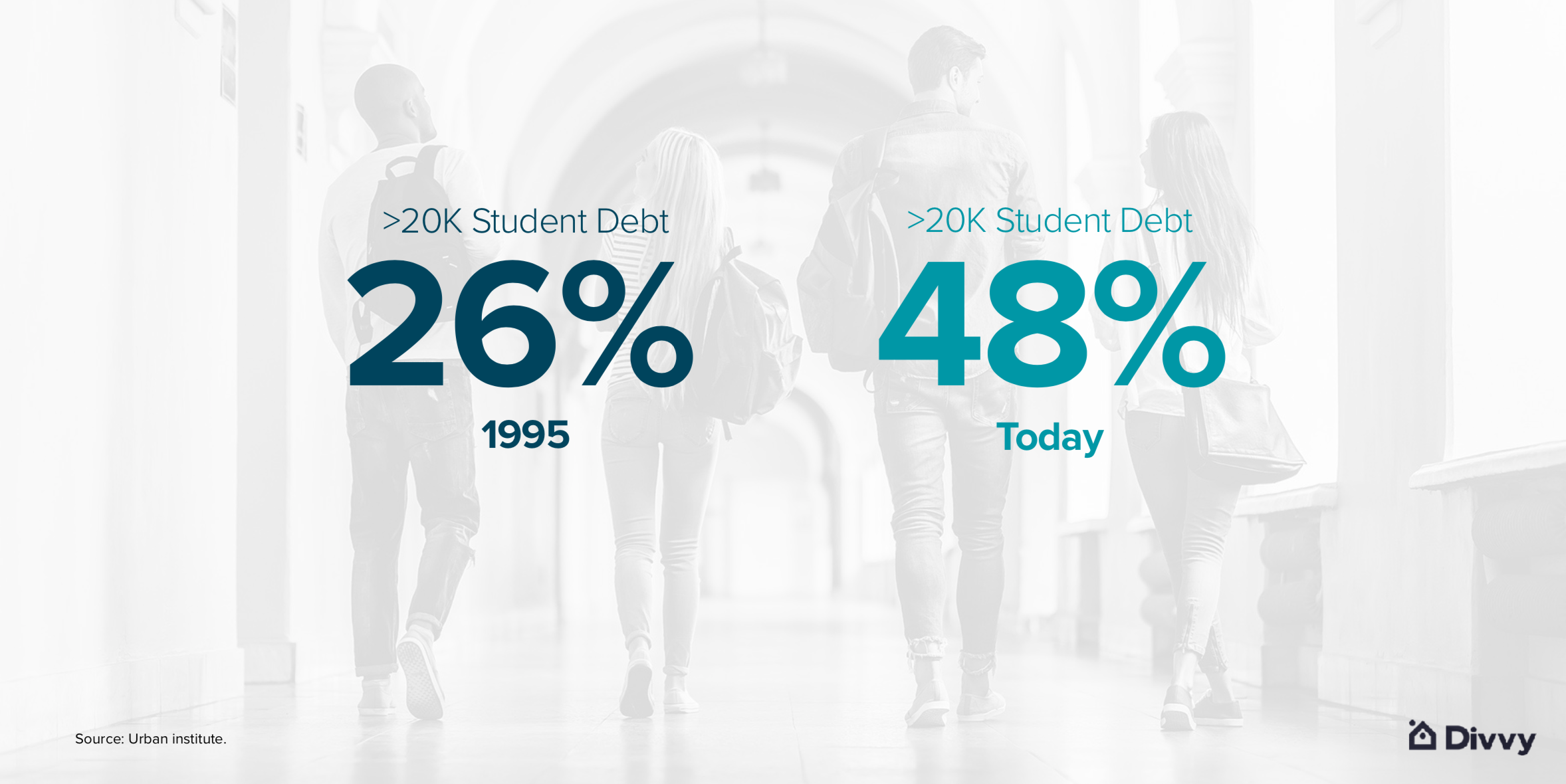

Millennials are more financially complex than past generations

Millennials are coming out of school saddled with more student debt than ever before. When you have more student debt, your debt-to-income ratio is now higher, which means you can only afford cheaper homes. But, as we’ve seen, there really isn’t a lot of affordable housing. That means you’re stuck in a Catch-22: there aren’t homes to buy, even if you were in the position to do so.

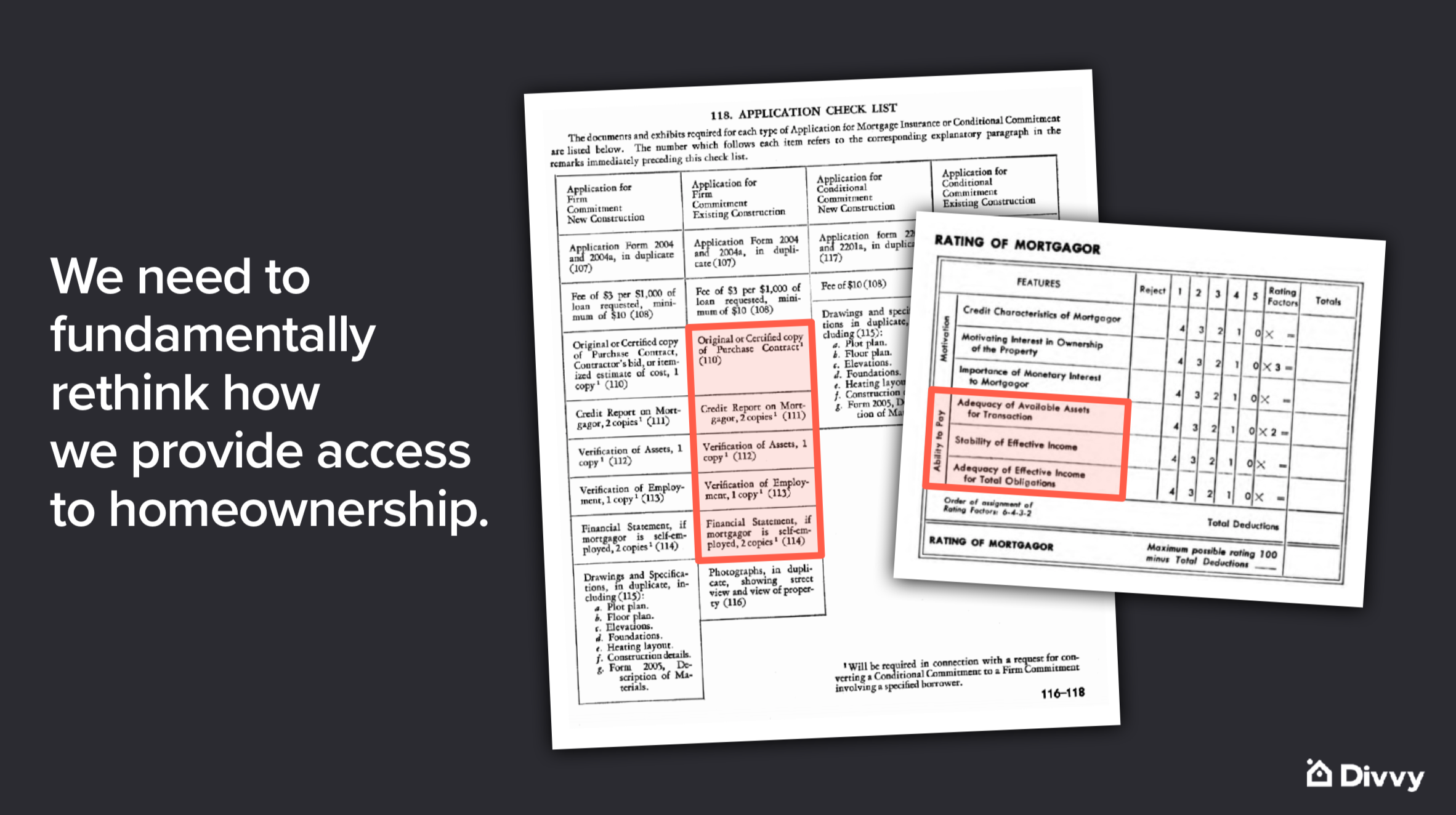

In order to better understand this problem, I went back to the underwriting requirements from the 1940s. These dated underwriting requirements are fundamentally the same today:

I personally applied for a mortgage last week. I applied to three different banks and was rejected from all three. I was told that, as a founder, my current income was too low to support a mortgage. (You’re welcome, Andreessen Horowitz. I’m keeping our burn rate nice and low.) This is the same problem that we’re seeing for, say, an Uber driver who has 1099 income, or a physician who just graduated from med school with hundreds of thousands of dollars in debt. We’re all in the same boat.

I believe that we need to fundamentally rethink how we provide access to homeownership. That is the past. The future—and the fix—is going to look quite a bit different.

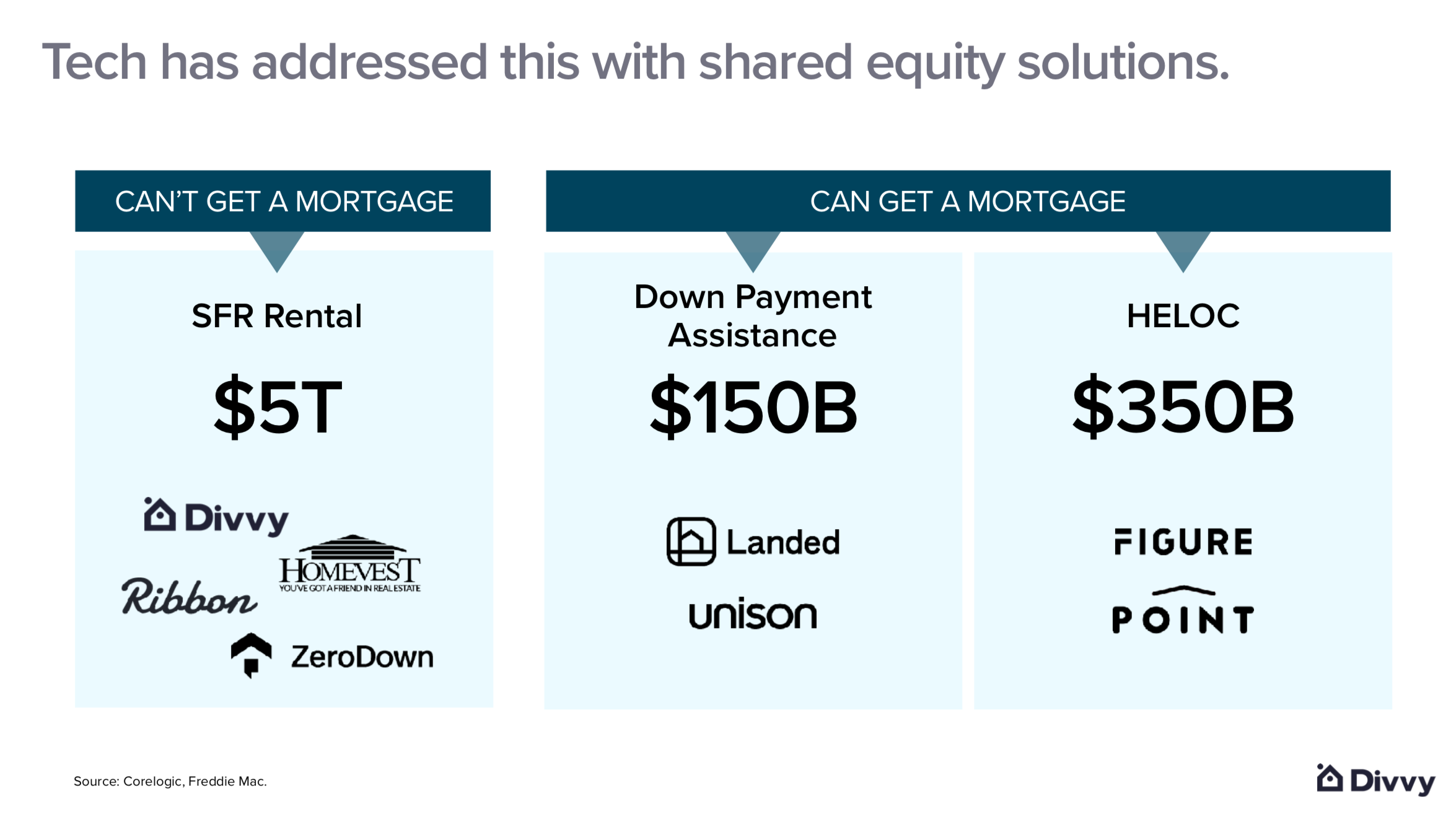

The way you would typically tackle this tremendous problem is to break it down into smaller pieces, which is exactly what the industry has done. On the right, you can see companies that have attempted to provide a solution for people who can get a mortgage by creating more liquidity in the market. On the left, you can see companies that have gone after consumers who haven’t been able to get a mortgage. Divvy falls into this category.

At Divvy, our goal is to create a stair-step between renting and owning a home. The industry today is very binary: You either rent a home or you dive into the deep end and get a mortgage. There is no in-between. What Divvy provides is something truly unique, which is access to the home you want today, without having to take on the financial risk of a mortgage. We still give you upside in the property.

Today, we’re operating in six locations: Tampa, Dallas, St. Louis, Memphis, Cleveland, and Atlanta. We’re squarely a product for Middle America, which we’re really proud of.

Here’s how Divvy works: You pick out a home and Divvy buys it on your behalf. You put down 2 percent at closing. We keep a synthetic equity account, where we show that you own 2 percent and Divvy owns 98 percent. That first month that you move into the house, we auto-pull your rent, just like you would pay anywhere else, but we parse that payment into an equity component and a rent component. Rent is how we make profit. The equity component goes toward building up your ownership in the home, piece by piece.

So, you go from 2 percent ownership when you start off, to 2.2 percent the first month, to 2.4 percent the next month, to 2.6 percent the next month, and so on. We’d like to build up to 10 percent over the course of three years. At the end of three years, or anywhere along the way, you can always buy out the house from us, if you’d like. Additionally, if you want to walk away, we’ll cash you out for your percent ownership in the house.

I think the key with Divvy is that we fundamentally make renters feel like homeowners. And the result of this is better business returns.

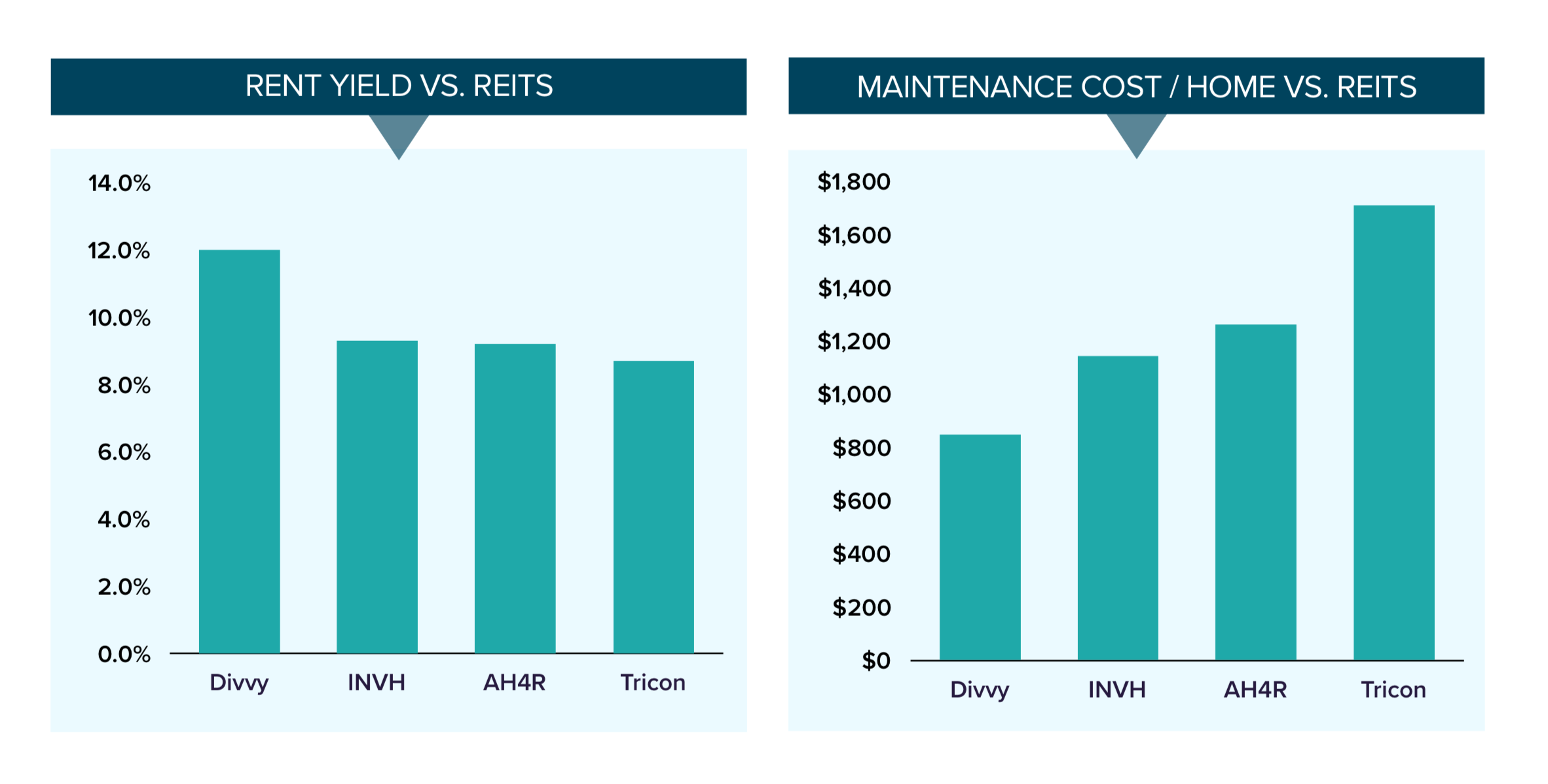

On the left-hand side (above) is our rent yield versus public single-family REITs. Right now, there’s just rent divided by the purchase price of the house. You can see that we add more rent per home on a constant purchase price basis, versus any of the public grids. Additionally, when renters think and act like homeowners, it results in lower vacancy, lower turnover, and lower maintenance costs per home.

On the left-hand side (above) is our rent yield versus public single-family REITs. Right now, there’s just rent divided by the purchase price of the house. You can see that we add more rent per home on a constant purchase price basis, versus any of the public grids. Additionally, when renters think and act like homeowners, it results in lower vacancy, lower turnover, and lower maintenance costs per home.

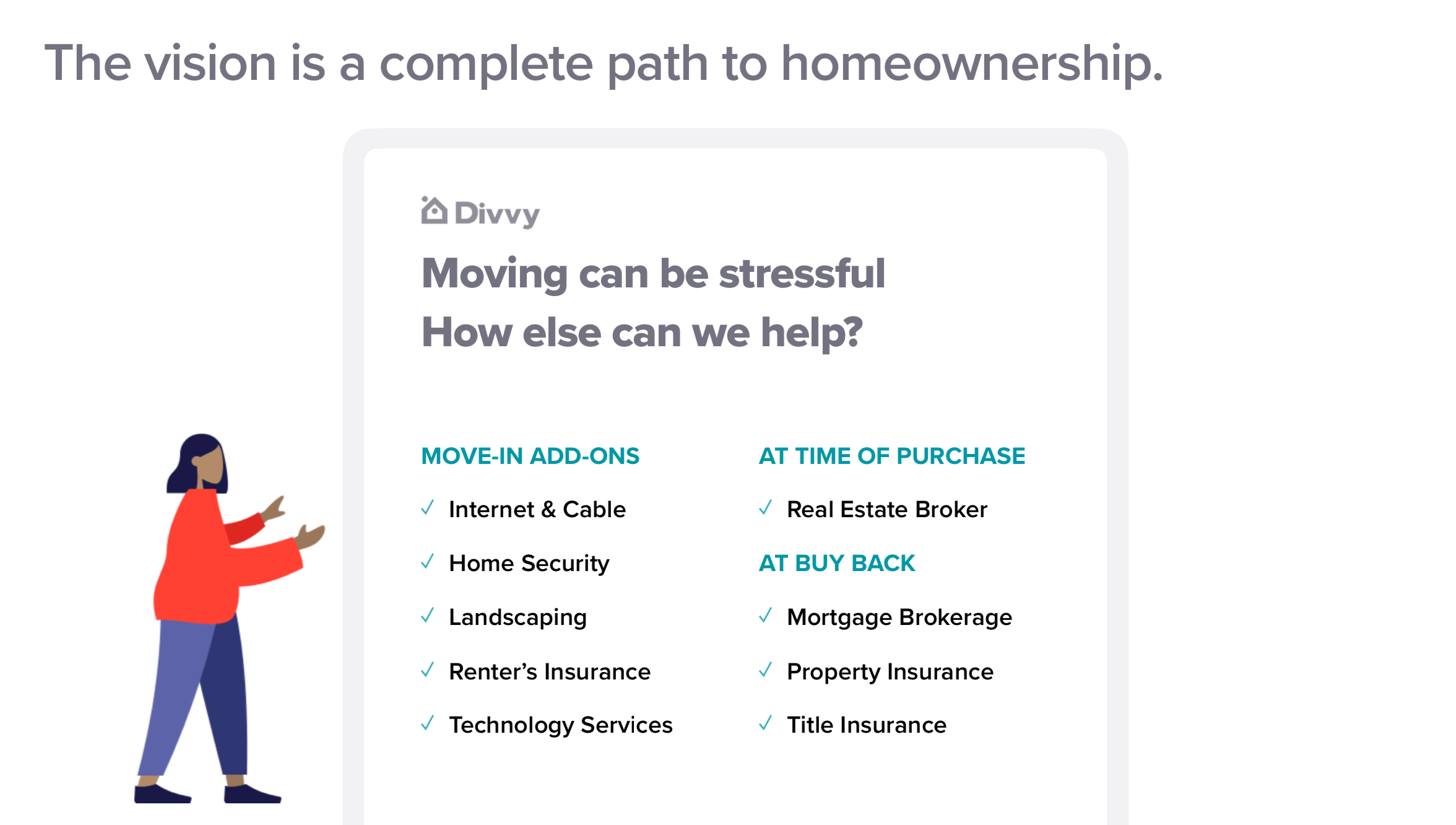

This is what Divvy has built to date. In the future, we aim to create not just a stair-step between renting and owning, but a complete path towards homeownership. In that case, not only would you go pick out the home that you want—and have Divvy buy it on your behalf—but before you moved in, you would get an email from us that says, “Do you want cable and internet setup? How about a landscaping package? How about renter’s insurance? Would any of that be helpful?”

Then, when you move into the house and the inevitable happens—say, a pipe bursts and water is leaking from your ceiling—Divvy is there to cover those maintenance costs and help you through it.

Ultimately, when you’re ready to buy a home and Divvy is able to underwrite your mortgage, we’ll send you a DocuSign that says, “Hey, here’s your Divvy mortgage. If you want to own this home, you can. If you’d rather keep the flexibility of renting, you can continue to do so.” From a first principles perspective, that is the way the industry should work.

I often come back to the idea that Divvy customers truly act and feel like homeowners, despite being renters. The reason behind that, I believe, is that Divvy provides a fundamentally unique experience. We give you access to the home you want today, without taking on the risk of a mortgage. But we still give you upside in the investment of the property.

The traction that Divvy and others have seen thus is proof that the real estate revolution has begun. Consumers can now get the home they want, when they want it, and are set up on a better path to homeownership.