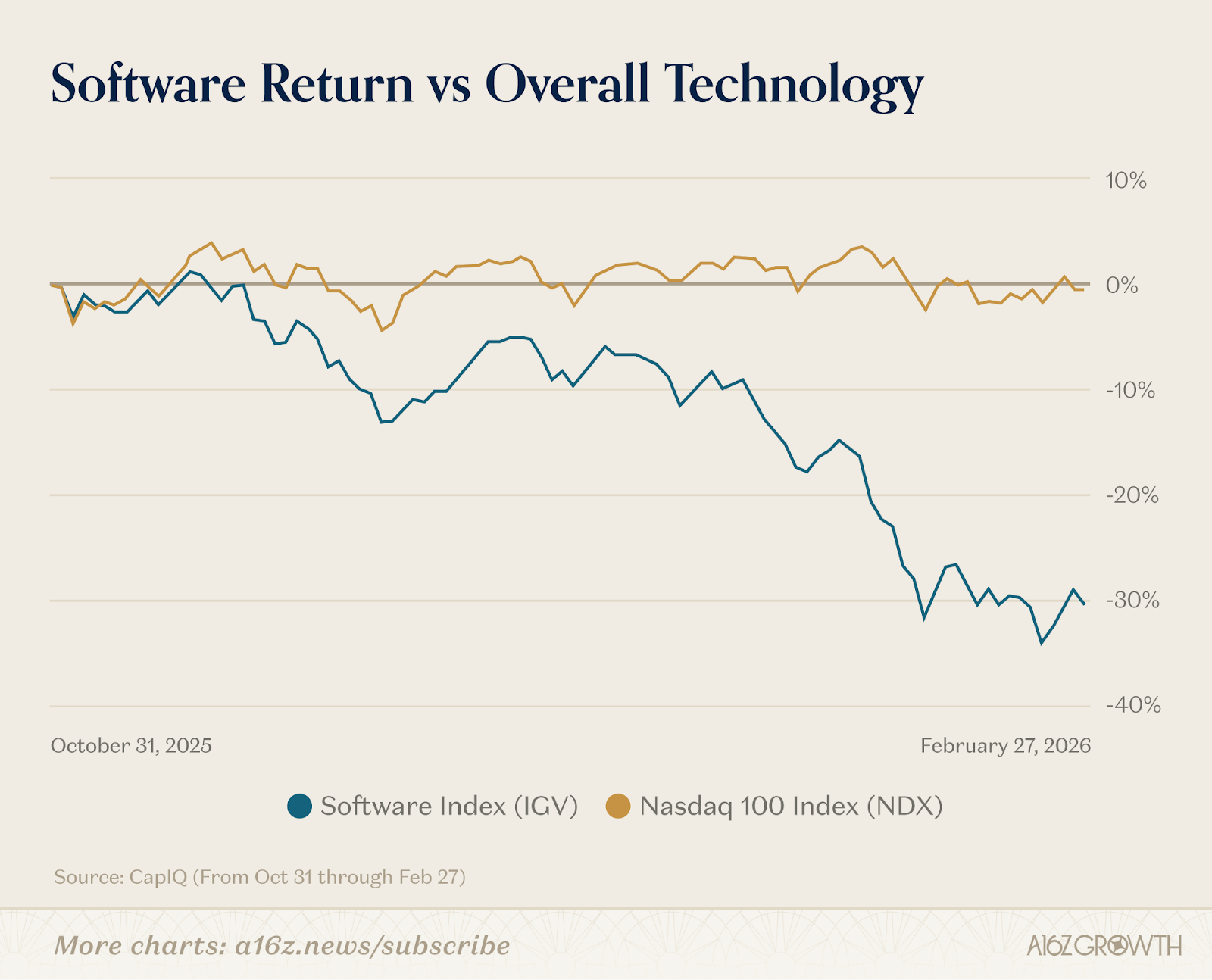

The software industry is having a panic attack. Since the start of 2026, ETFs for public software companies have fallen by 30 percent, erasing all the gains since the launch of ChatGPT. Companies like Salesforce, Adobe, Intuit, ServiceNow, and Veeva—bellwethers that have compounded investors’ capital for a decade or more—are down 25 to 30 percent in a matter of weeks. Viral Substack posts imagine a world where the customer base for enterprise software is hollowed out and the S&P enters a massive years-long drawdown. They’re calling it the “SaaSpocalypse.” It’s rapidly become the market consensus: AI is going to kill the software industry.

Yes, AI is a big deal. But the conclusion that AI is going to kill the vertical and functional software business model simply makes no sense. The truth is that AI simply isn’t going to kill software companies: after all this panic has passed, we’ll see that AI is the best thing that ever happened to the software industry.

Why is that?

The bear case rests on a basic misunderstanding of what software companies actually sell. The market is treating “software” as though it were a commodity input—as if the value of a software company resided in its code, and cheaper code meant more competition and therefore cheaper companies. But code is never where the value has lived: if code is where the value was, these companies would have never gotten so big in the first place. They would have been killed years ago by open-source software or by competition from cheap software engineering labor in developing countries.

The bearish arguments today usually fall into one of four categories. Maybe the foundation model labs will move up the stack and own every function-specific application. Or maybe enterprises will “vibe code” replacements for their internal tooling, or at least use the option of doing that to reduce software businesses’ pricing power. Or maybe existing players will use AI to massively expand their product breadth, rubbing against each other. Or maybe a flood of new entrants—the famous “single-person billion-dollar company”—will undercut incumbents on price. Pile on top of this agents won’t care about brand loyalty or familiar names, only the cheapest options for any particular task.

AI might increase competition; but it’ll also dramatically expand what software companies can do, how fast they can do it, and how large the markets they serve can become. The end result won’t be margin compression to zero. Software will be a much bigger industry, with durable competitive advantages for the companies that earn them.

The moats that matter aren’t going away

The classic contemporary book on business moats is Hamilton Helmer’s Seven Powers. He lists seven distinct ways in which companies develop robust competitive advantages: Scale, network effects, counterpositioning, switching costs, brand, cornered resources, and process power. Let’s go through them:

Switching costs are perhaps the one moat that really is going to change. It’s definitely true that AI is changing the friction and the cost-benefit analysis associated with switching vendors: agents can assist with a lot of migration work that used to be a headache. So it means legacy companies with “hostages, not customers,” to borrow a phrase from our colleague Alex Rampell, will feel a lot more pressure than they’re used to.

But that is a good thing for software as a whole. When companies have to earn their customers’ loyalty instead of relying just on vendor lock-in, the result is better products, faster innovation, and a healthier competitive ecosystem that grows faster and delivers more value to its customers. We expect AI will shift some customers to new winners, but it won’t impair industry profit pools at large: companies will just get better.

Network effects are a classic moat. And they aren’t going away. We tend to invoke network effects for social media platforms or marketplaces —the more nodes in the network, the more attractive it is to be on it. But the same applies to application software offerings that exhibit ecosystem, collaboration, and data network effects. On the surface, Salesforce is a CRM database; but anyone who has worked in an enterprise setting knows that Salesforce is also an ecosystem. When everyone uses one platform, the network becomes self-reinforcing: you use Salesforce because everyone uses Salesforce. And the more companies use Salesforce, the more valuable the ecosystem of third party applications built on top of Salesforce and platform administrators experts in Salesforce. In recent years, a similar thread is true for Figma: every designer, then every engineer, product manager, marketer buys Figma because everyone is collaborating there – go to the annual Config conference and witness the value of the ecosystem firsthand.

And the same dynamic is emerging in the AI-native generation. Harvey and Hebbia are building finance and legal collaboration spaces that connect service providers and clients, and soon their agents, on a single system: the more people and agents who use these platforms, the more valuable the platforms become. EliseAI’s maintenance product is a multi-sided network that becomes more valuable with every unit and vendor added. As migration gets easier, aggregation gets easier, but these network effects simply don’t go away in a world where software is free. In fact, insofar as AI makes the network more powerful—you can just do much more with a network than you could before—we should expect to see AI make these network effects more powerful than they were before.

Scale was never the defining moat in software—it’s just not as important for Salesforce as it is for a cloud provider or for an industrial company. But to some extent, it may matter more for AI applications where compute spend exceeds labor costs, driving a unit cost advantage to the larger consumers of tokens. In addition, there are places where scale will still help: it’s a straightforward economy of scale to concentrate that maintenance burden in one place, since productivity gains from specialization don’t go away in an AI world. Stripe highlights the value of centralized infrastructure benefitting all of its clients. Its compliance infrastructure absorbs the cost of navigating regulations across dozens of countries so that individual businesses don’t have to; its payment optimization algorithms, which route and retry transactions to maximize authorization rates, improve with every dollar of volume—and they can pass those savings on to their customers. Finally, scale will continue to benefit companies at the intersection of bits and atoms; Anduril, Flock Safety and Waymo will continue to see lower unit costs as they produce higher volume of their hardware offerings.

Brand endures. For better or worse, “no one got fired for buying IBM” remains a fact of life in most enterprises. And if every industry gets more crowded—if there’s suddenly an explosion of fly-by-night solopreneurs selling vibe-coded ERPs—we should expect the power of strong brands to increase. Brand is how you signal reliability in a world of infinite optionality. No upstart is going to instantly replicate the trust and recognition that companies like Stripe or Shopify or ServiceTitan have built. The closer you sit to business-critical functions—people really don’t want to get creative when it comes to payment processing—the more powerful brand effects will be. If you are a startup and you charge customers, you build on Stripe by default.

We do acknowledge the power of brand might change as more decisions are delegated to AI agents that optimize for price without the soft considerations that humans have (agent-led growth!). But as long as they report to humans who have to worry about getting fired, the “no one got fired for buying IBM” principle still holds.

Cornered resources, like high-quality proprietary data, aren’t going to stop mattering either. If friction goes to zero, simply consolidating publicly available data into a usable interface becomes less valuable, because anyone can do it. But if AI enables doing much more with high-quality data than you could before, then the stuff that you can’t get easily becomes extremely valuable. We have observed the power of Bloomberg’s live market data, Abridge’s millions of clinical conversations, OpenEvidence’s vast medical library, and VLex’s legal database.

And perhaps the strongest moat of all in this new era is process power—or as George Sivulka of Hebbia calls it, “process engineering.” Application software can be thought of as a stored process—it encodes opinions about how the function of an organization should operate, and those opinions calcify over years and decades of use into something that is inseparable from the organization itself. Successful app software companies are the ones that co-evolve with their clients around these workflows. As those workflows penetrate ever-deeper into an organization, process engineering only becomes more important. And more difficult for challengers to replicate.

Consider Harvey. If Harvey deeply understands how a particular law firm structures its work—the templates, the review processes, the institutional preferences, the way a specific partner likes her memos done—there is simply no way a new entrant can replicate that overnight, even with the cost of code being zero. That kind of embedded workflow knowledge becomes more powerful, not less, as software moves from a system of record to a system of action, because you can just do much more with that knowledge. So as the underlying models improve, Harvey’s orchestration layer—the scaffolding that routes model output through specific professional workflows—compound in value. Better models don’t make the application layer thinner: they make it more capable, because the hard part was never raw intelligence. It was knowing what to do with it.

Platform shifts create new winners—and new moats

But there’s one final source of durable competitive advantage that we find particularly exciting as investors. And that is counterpositioning.

Counterpositioning is a kind of power that can be summoned and wielded by new entrants to a market. It’s when the new company has a business model which, for whatever reason, is unattractive for the incumbent company to compete against. Disruption theory from Clay Christensen is a classic type of counterpositioning, but it doesn’t always have to be “low cost” as the differentiated counterposition. In software, a new technology stack could create the opening for a startup to create new kinds of products and business models that are difficult for incumbents to replicate – like Databricks and their “Lakehouse” model.

The “agent” model of doing work and replacing tasks is certainly going to create some counterposition opportunities for new startups to challenge incumbents. There’s been a lot of ink spilled on the disruption of “per seat pricing” at the hands of agentic upstarts with value-based pricing. Let’s take customer service as an example. Decagon prices its customer support product per conversation handled, not per agent seat, and will eventually price per resolution achieved: that’s fundamentally a better alignment of incentives between vendor and buyer. An incumbent like Zendesk can’t easily make that same move without cannibalizing its own seat-based revenue. Just as Blockbuster couldn’t match Netflix’s subscription model without destroying its existing economics or Peoplesoft couldn’t match Workday’s SaaS model without upending its monetization. Companies that start with the new business model don’t face that dilemma, and it’s the core reason why platform shifts so reliably produce new winners.

But guess what? The total amount of “end state pricing power” in the market didn’t necessarily decrease; it just means customers now have a choice of business models they’d like to subscribe to, and the better one will win. That’s how competitive markets have always worked! AI is not the first time that a wave of creative destruction has rearranged markets and shifted the playing field. But here’s the thing: the business models that result almost always dwarf the old ones in the scale of the total opportunity.

The great software bifurcation is coming

So yes, AI will definitely change vertical and functional software. But it won’t look like a massacre. Maybe gross margins settle into a different steady-state: maybe pricing power is diminished because switching costs give procurement teams more leverage in vendor negotiations, but AI also supports margin expansion due to a much more efficient use of labor. But no matter where margins end up, we expect that scale will expand dramatically: because as our colleague Anish Acharya likes to say, the world is still short software. We are nowhere near saturating the world’s demand for high-quality software. And as code becomes cheaper, we should just expect to see the market demand more.

On the other side of this AI transition, we’ll be looking at a much bigger software industry that provides much more value to its customers. Companies will be able to serve more customers, enter adjacent markets, and automate workflows that were previously far too complex or too expensive to touch. Customers that were previously too low ACV will suddenly have attractive economics. Ideas that would once have gone in the “too hard” pile suddenly become interesting and feasible. There will still be moats, and as long as there are moats there’s plenty of reason to expect hugely successful and highly durable businesses to survive and thrive.

AI isn’t going to destroy the software industry; it’s going to split it into two parts. There really will be some categories of software companies that face genuine pressure. Frontend tools that serve primarily as thin wrappers around commodity functionality and do relatively little beyond presenting data in a slightly more convenient format are vulnerable. Incumbent systems of record that still operate on archaic interfaces but raise prices every year should be worried. So should software companies that have an outdated pricing model and value proposition that’s just inferior to what AI-native competitors can offer. The companies that win in this environment will be the ones delivering genuine value, not the ones that built the highest walls around their customer base.

But that’s just creative destruction: it’s great for the industry that these companies are facing pressure that they weren’t facing before. Some of them will figure things out and get stronger ; others won’t and will die. That’s good! The rest of the software ecosystem—the companies that are committed to delivering real value for their customers—is set to grow massively.

So yes, some individual companies will lose. But the industry will win, and win big. The SaaSpocalypse isn’t the death of software. It’s the start of something much bigger.