The internet opened up a major consumer market by providing services more cheaply, and to more people, online. Now, AI is kicking off a colossal wave of opportunities for startups by making it possible to build scalable online experiences that replicate the benefits of being in person.

Having a highly personalized experience is what consumers value the most about in-person services—think of tutors, personal trainers, and doctors. Though companies offer some customized features like recommendation engines, they haven’t yet had the technology to deeply personalize their services.

But generative AI will change this and open up a massive opportunity for consumer startups. There are technical hurdles to overcome, but as companies introduce multi-modality and improve model memory, latency, and steering, they can tailor their services to each individual’s preferences and usage over time.

As a result, we’re now entering an era where AI-native services can and will be personalized to each user. Though we think most of the value created by these AI-native companies will accrue to consumers in the form of consumer surplus, we roughly estimate the total opportunity will soon be 5–20x+ higher than it is today.

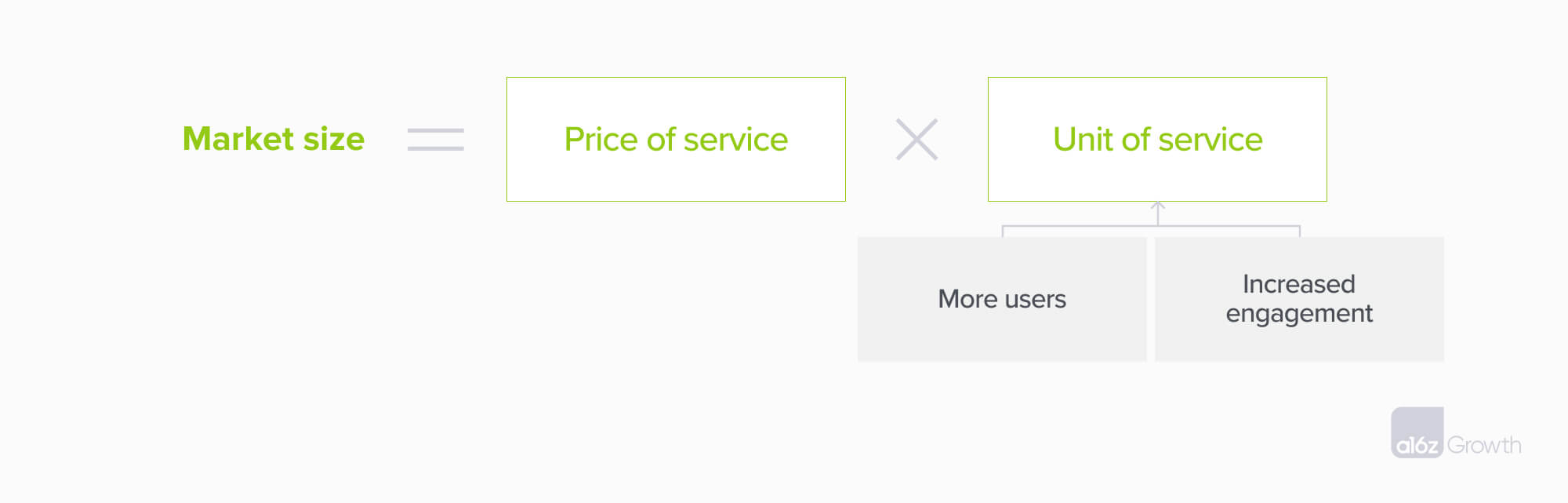

To calculate the size of the market, we use the equation price of service x unit of service (e.g., users, time spent). We expect personalization with AI will increase both the price of service and units of service by unlocking:

- More users. Personalization will compel users to switch from in-person services to AI-native ones and attract users who were unable to access in-person equivalents.

- Higher prices. Users will pay more for personalized digital services than for existing online options.

- Better retention and engagement. Users will use more personalized products, more often.

More users

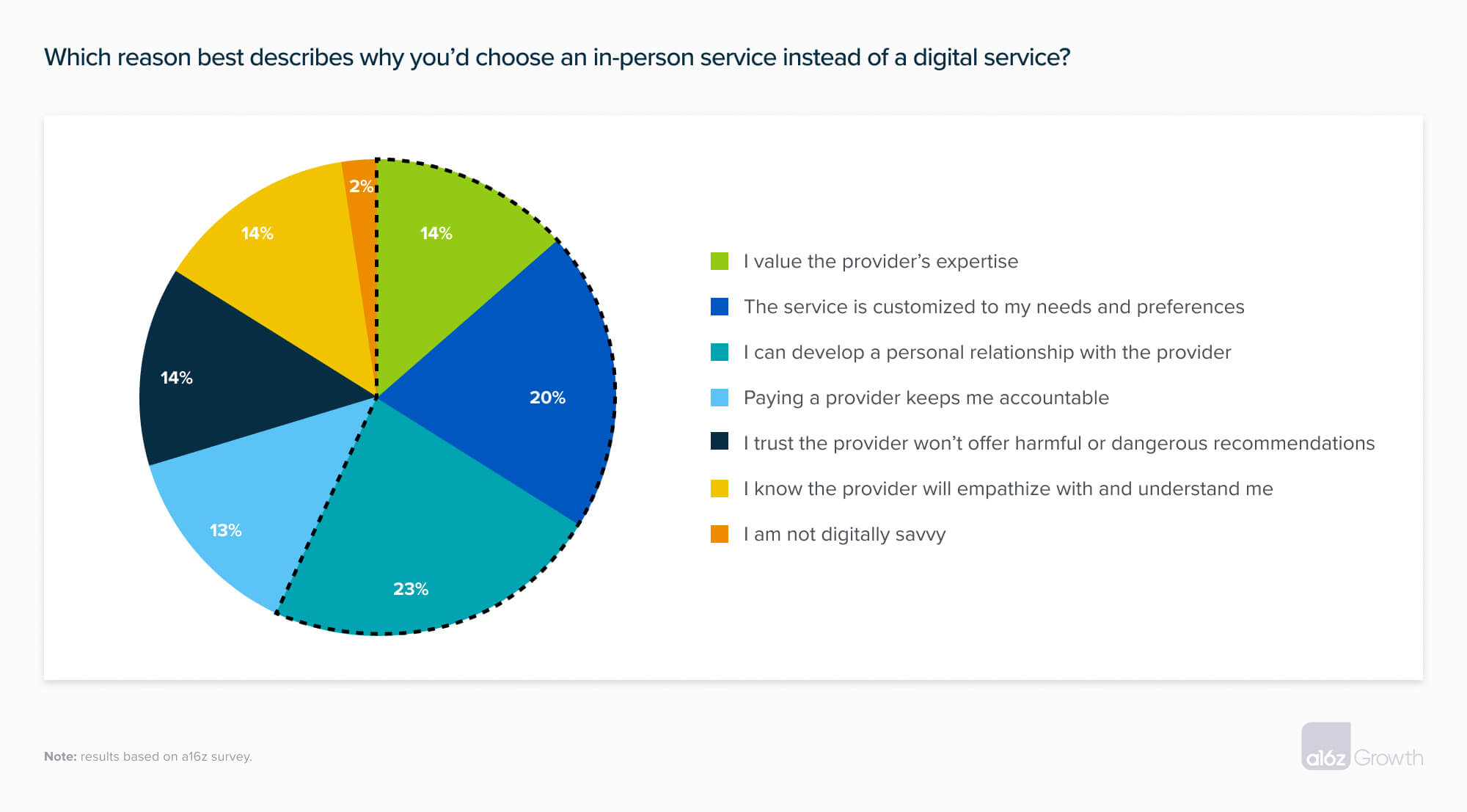

We ran a broad survey to understand when and why consumers prefer 1:1 in-person or digital services for mental health, fitness, tutoring/education, and music instruction. 57% of respondents identified customization, expertise, or developing a personal relationship with a provider as the primary reason they preferred 1:1 in-person services—all preferences generative AI currently seems well-positioned to address. Over time, we expect that generative AI will also help companies build empathy and trust, 2 of the other reasons why people choose in-person options.

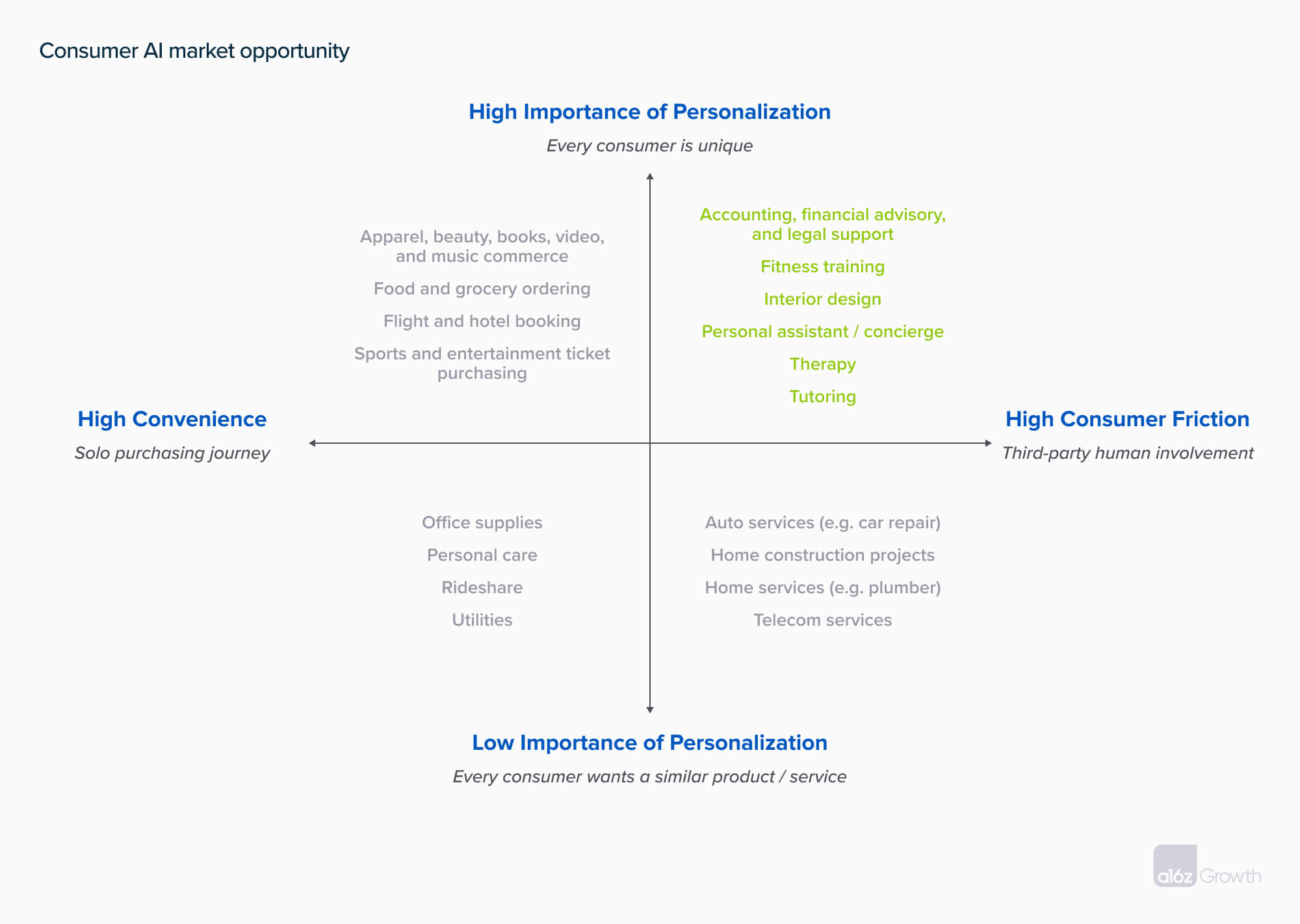

Though generative AI will unlock opportunities across consumer services, it will have an outsized impact in industries that haven’t been penetrated by e-commerce. To date, e-commerce has penetrated industries with transactions that require limited third-party expertise, like paying utilities or booking flights. We see outsized opportunities in high-touch industries where personalization matters the most to consumers, represented by the top-right quadrant below.

Higher prices

Today, there’s a massive price gap between digital and in-person services. Although existing digital services often aren’t direct substitutes for in-person services, they offer similar experiences.

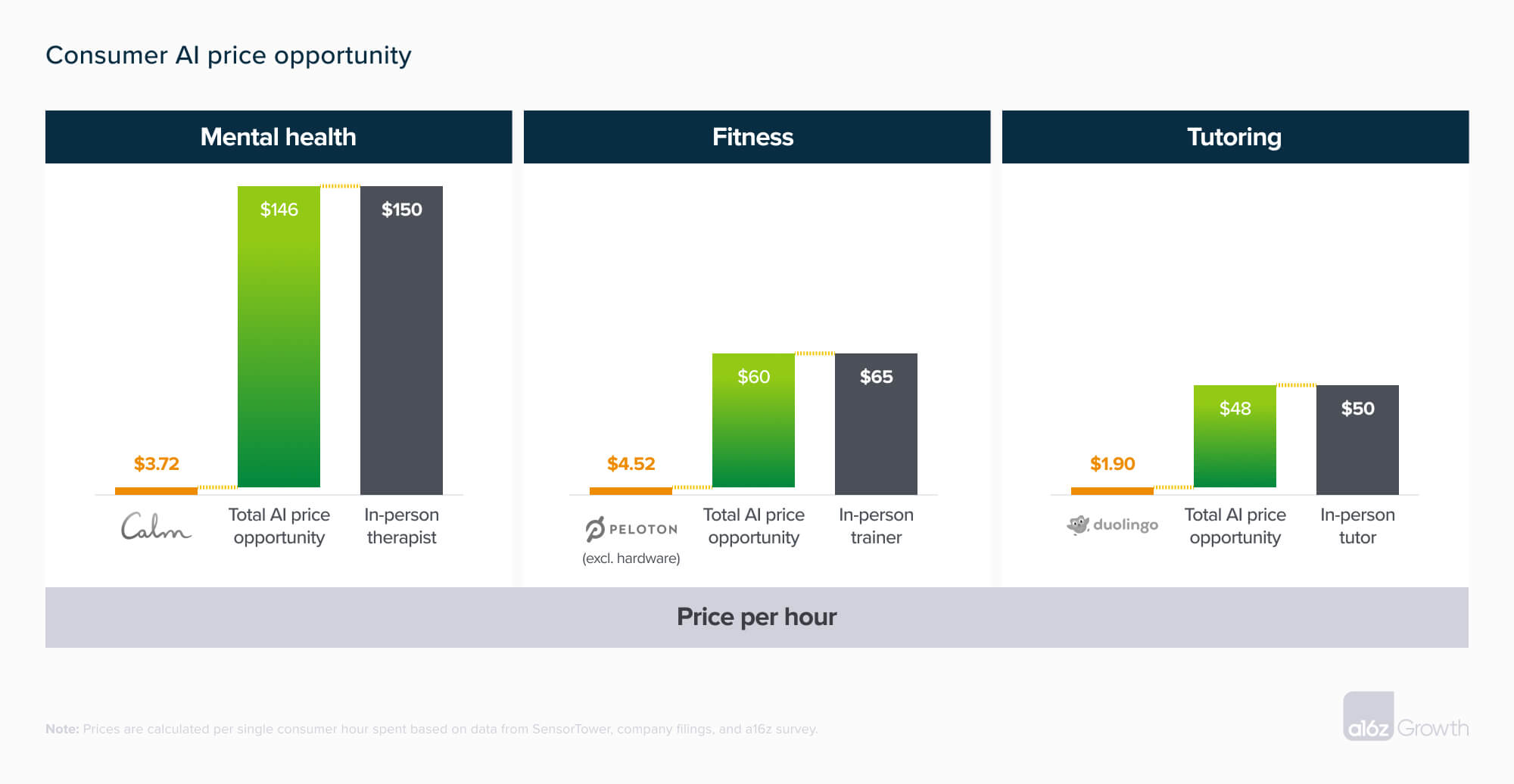

We’re in the early days of this market, and we don’t know how much of this delta consumers will pay and how much will accrue to consumer surplus. Right now, however, we’re seeing consumer AI apps commonly charge a 2–3x premium over their non-AI equivalents. While it’s possible that AI apps will cost the same as existing apps over time, consumers may pay the existing digital price plus some portion of the delta between the current digital and in-person prices. To illustrate the potential size of this total opportunity—consumer surplus included—let’s estimate that consumers would pay half of what they currently pay for in-person services. Looking at mental health, fitness, and tutoring, then, the current total AI pricing opportunity would be ~$77 for mental health ($3.72 + $73.14), ~$35 for fitness ($4.52 + $30.24), and ~$26 for tutoring ($1.90 + $24.05).

While AI-native services may be able to command higher prices, it’s generally more expensive for those companies to serve their customers. Supporting AI-native services includes paying compute costs for training and inference, as well as compensating human labor to address the long tail of use cases. In short, offering more personalized products will cost more, but consumers will be willing to pay much more for those products, which should translate to a larger overall profit pool.

Better retention and engagement

Better personalization could also help companies attract more users and encourage those users to spend more time on their products. Therapy is a great example. There’s a shortage of therapists in the US, and these services have historically been offered in 1:1 or small group settings. Many people who want to see a therapist aren’t able to because it’s often prohibitively expensive and there can be a stigma associated with seeing a therapist. AI will provide a step-function improvement in these cases. An AI-native therapy app can offer personalized, on-demand, world-class expertise in the comfort of your home, at a price point that’s dramatically lower than the in-person—and perhaps lower-quality—alternative. Plus, the convenience of the online service means that users may spend more time on the AI therapy app. After all, your AI therapist has the knowledge of every expert therapist, remembers all your sessions perfectly, and is always on call.

Though we’re in the early days of this new wave of e-commerce, we’ve already seen some AI-native companies enjoy some success. Character.AI is seeing success as an AI companion and many users are using the platform as a tutor and therapist, Perplexity serves as your research assistant, and Speak offers a step-function improvement on language learning apps. As researchers improve model capabilities and companies develop more established relationships with users, we can expect AI to not only improve the quality of personalization, but also approximate other elements of in-person experiences, like empathetic communication. This will, in turn, attract more users willing to pay more for these services. As our partner Marc argued, “every person will have an AI assistant/coach/mentor/trainer/advisor/therapist that is infinitely patient, infinitely compassionate, infinitely knowledgeable, and infinitely helpful. The AI assistant will be present through all of life’s opportunities and challenges, maximizing every person’s outcomes.” We’re excited to see new companies build, experiment, and grow in this space.

Special thanks to Olivia Moore and Santiago Rodriguez for their contributions to this piece.