This is the first post in our new series on digital health go-to-market. For more digital health content, visit a16z.com/digital-health-builders and follow a16z Bio on Clubhouse.

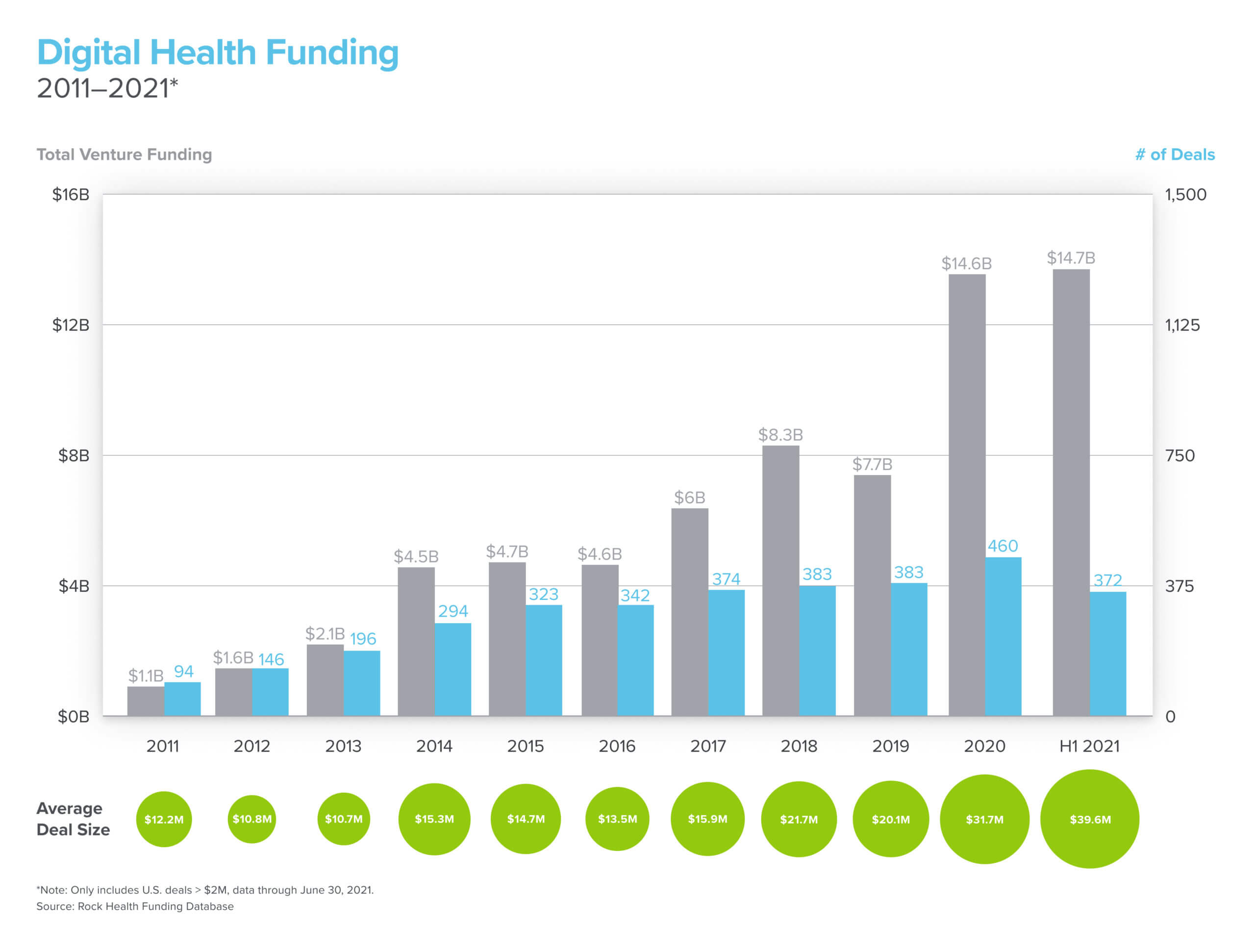

Digital health is currently one of the fastest growing segments in the VC-funded universe, and we’re seeing digital health companies scale to new levels of growth. Many later stage virtual care companies have demonstrated best-in-class growth rates, even relative to the broader consumer and enterprise software space. And healthcare is no longer entirely a local game—new tech-enabled care delivery companies are achieving nationwide scale in their first few years in the market, whereas traditional players might have been in just a handful of states after a decade of existence.

But this market wasn’t always this hot—over the last 10 years, multiple generations of healthcare technology companies struggled to get lift-off, not because their products and services weren’t transformative, but because they failed to find an executable path for sustainable distribution and value capture. Distribution—arguably the most important driver of failure or success in the fast-growing digital health domain—was historically a very steep hill to climb. Some of that was simply due to the overall immaturity of the market and its inability (or resistance) to absorb and pay for novel, technology-based products that didn’t slot easily into existing budgets and care plans. Some of it was that companies lacked the capital to be able to survive long enterprise sales cycles that were the primary path for going to market.

Behind the current growth of the digital health market is a revolution in how digital health companies go-to-market. A wave of innovative companies are fundamentally re-envisioning what healthcare looks like, and it’s time that the GTM playbooks for digital health of yore be rewritten to acknowledge what’s happening in the current (and future) market. In this blog, we explain how and why the go-to-market motion has changed for digital health, as well as an introduction to the new GTM motions in digital health. In the coming weeks and months, we will present a series of Go-To-Market Playbooks for Digital Health Builders to share insights and wisdom from leading digital health founders and builders.

A decade ago, digital health lacked the capital for companies to raise enough financing to live out long B2B sales cycles.

The evolution of digital health: How did we get here?

These evolutions in go-to-market are part of the overall evolution of the digital health space. In the early 2010s, the primary distribution channel for digital health products was through incumbent providers, payors, and life sciences companies, as well as early activity with self-insured employers. The go-to-market motions were akin to traditional enterprise sales, with field sales teams, long sales cycles, and land-and-expand strategies that would ultimately result in enterprise-wide deployments with multiple products. As a result, digital health companies were limited to supporting legacy players in the form of internal workflow tools or behind-the-scenes managed services. They had very little reach into actual patient-facing experiences, which made it hard for them to capture value because they were so far removed from the end users.

As the overall consumer tech revolution gained momentum and healthcare infrastructure started to mature, the next wave of digital health startups in the mid-2010s began going “full stack” to compete directly with legacy players for patients and providers. Some companies (e.g., Noom, Headspace, and Ro) sold directly to consumers, while others (e.g., One Medical and Lyra) found success with large employers, who would offer the services to their employees as covered benefits.

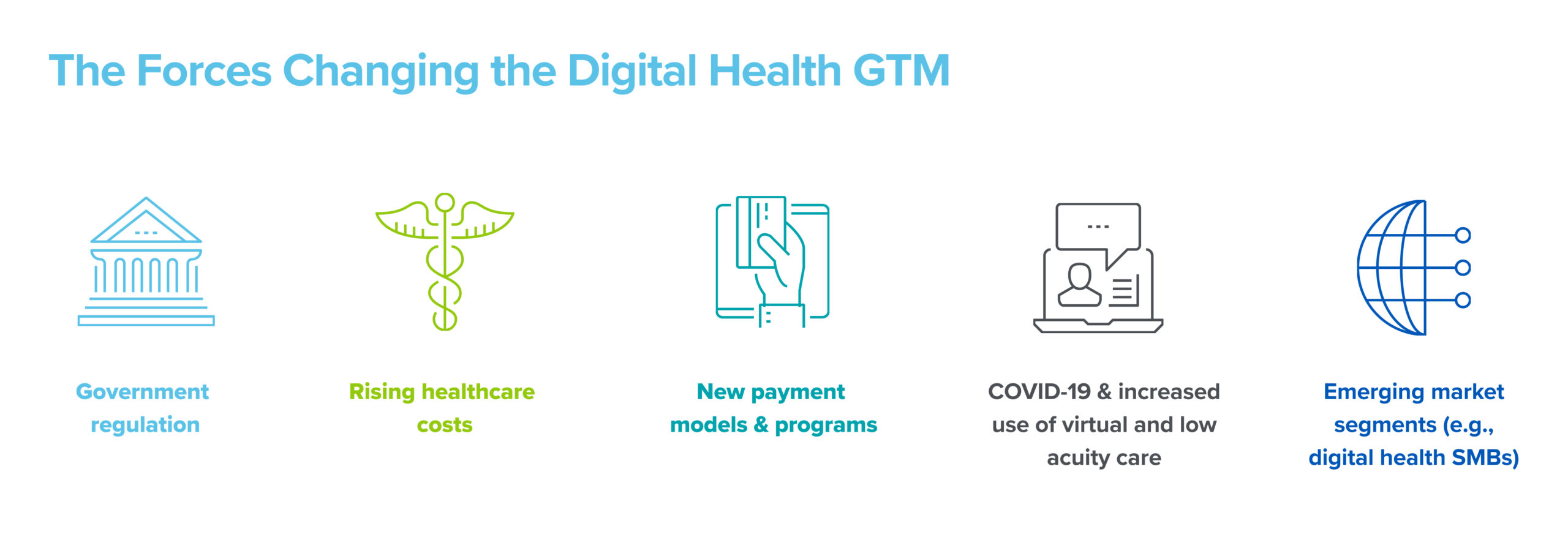

Fast forward to today, and a dizzying number of new and compelling care options for patients in new formats have hit the market. Novel payment models, rising healthcare costs, shifting financial responsibilities, a consumer preference for virtual-first experiences, and emerging market segments with new buyer dynamics have opened up new distribution channels that have fundamentally rewired the healthcare value chain. For instance, new virtual care regulations related to reimbursement policy have made it possible to bill for services that historically were not monetizable, so startups can take the form of a virtual-first clinic and acquire patients directly through digital marketing, while getting reimbursed as an in-network provider on the backend. Additionally, COVID-19 has accelerated the transition to virtual and lower acuity care, and consumers have become a major payor of sorts, representing nearly $500B of out-of-pocket healthcare spend in 2021, and growing 10% year over year. Cash pay services and telehealth marketplaces have emerged to fill the void of affordable, consumer-friendly offerings that patients can purchase directly while they’re still below their health plan deductibles. These new digital health companies represent an emerging market segment of small businesses that are potential end customers for new digital health infrastructure solutions.

The new go to markets in digital health

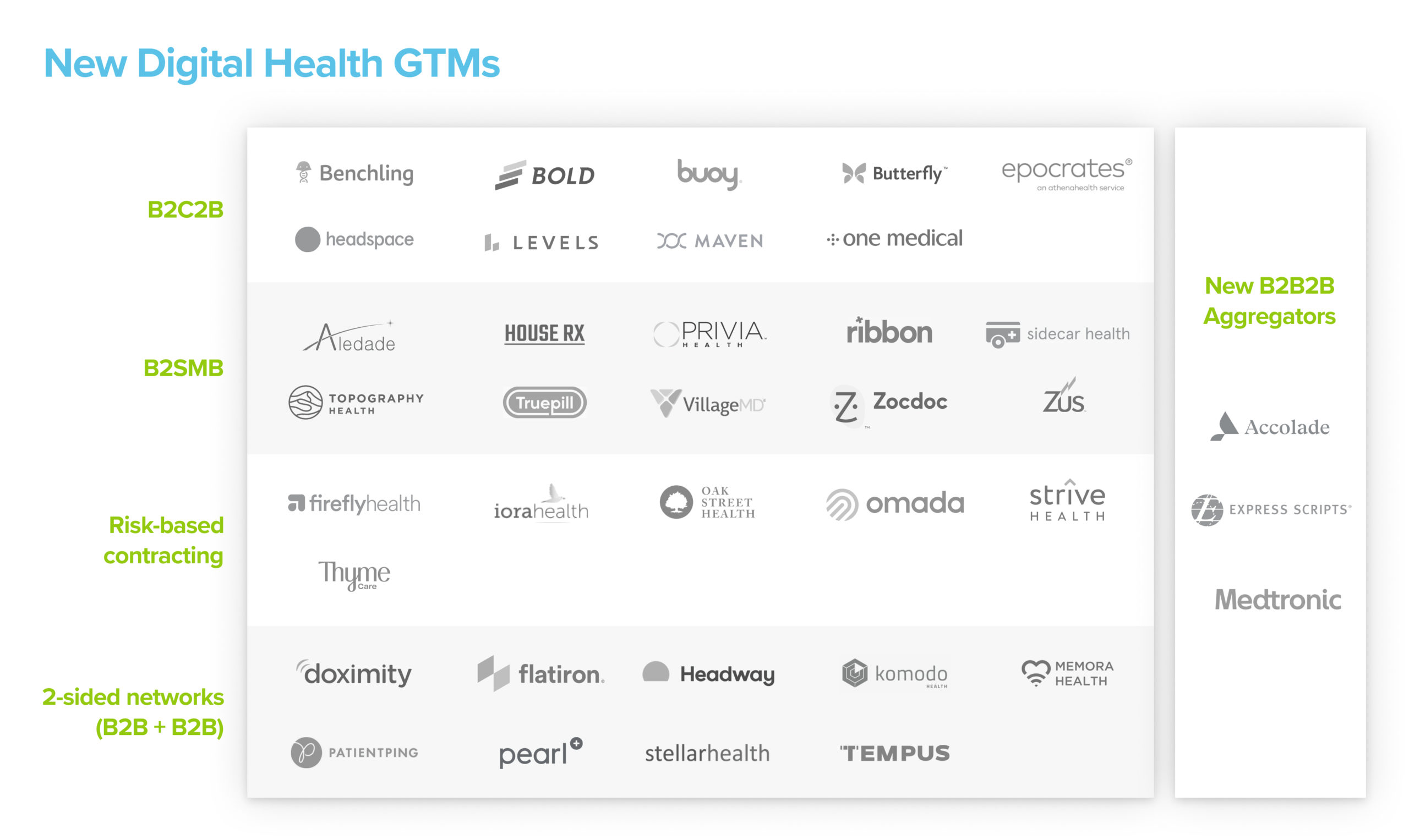

We are seeing five new go-to-market motions in digital health—B2C2B, B2SMB, risk-based contracting, two-sided networks, and distribution partnerships through aggregators. While we describe these below as distinct motions, go-to-market is complex and varies for each company. In reality, companies might even draw on multiple go-to-market strategies from this list, and that mix may change as the company matures.

For example, Firefly Health experimented early on with a B2C2B motion, but then eventually vertically integrated into a full risk-based contracting model once they garnered sufficient proof points with their early payor partners. Our aspiration here is not to be prescriptive, but rather to empower digital health builders with insights that help them make strategic decisions about how to distribute their products and services.

- B2C2B / bottom-up sales: B2C2B companies acquire patients directly with a full-stack service, then leverage their user base to negotiate enterprise contracts to subsidize or fully cover the price of the service, and earn the right to make it available to a broader pool of users in one fell swoop.

- B2SMB: New digital health clinics have themselves become a new SMB segment for infrastructure companies like Zus, Ribbon Health, and TruePill to sell into. Additionally, many “provider enablement” startups like Pearl Health, Topography, and HouseRx are pursuing smaller provider practices with products and services to help them remain independent through diversification of revenue streams. Small business sales generally have shorter sales cycles and faster feedback loops, but also higher churn, smaller average contract values, and pressure on cost structure to maintain high margins.

- Risk-based contracting: For years incumbents have been slow to adopt value-based care models. Digital health startups are at the tip of the spear of implementing risk-based payment schemes, where they take full financial responsibility for an episode of care, or the comprehensive care for a given patient. Companies such as Oak Street Health involve contracting with health plans to delegate clinical and financial responsibility for entire patient populations, while wrapper models like Omada get paid by their employer and carrier customers only when they deliver specific outcomes for a cohort of patients with a specific condition.

- Two-sided networks: This go-to-market approach builds a product or service that is valuable to one market constituent, and then leverages that network of users, and/or the data generated by those users, into a sale to a second market constituent. These business models typically engender network effects and have mutually reinforcing dynamics based from the two complementary customer sets. For example, Flatiron sells a suite of software tools to providers to help them more effectively care for their patients, and then provides a separate set of products and services—enhanced by learnings from its provider-facing business—in order to help life sciences advance new medicine research.

- Distribution partnerships through aggregators: In any industry, there exist massive players who own distribution to major swaths of users, and therefore become key distribution platforms for startups (e.g., Google, Amazon, and Facebook are amongst the most notable examples). In healthcare, vendor fatigue with the proliferation of digital health point solutions is driving a select set of incumbents to step into the mix and monetize their position as a dominant distribution channel by consolidating purchasing decisions through their platforms. For instance, Express Scripts’s Digital Health Formulary and Accolade’s Partner Platform enable distribution of digital health solutions to their employer customers, while Innovaccer’s Partner Program does the same for health systems and health plans.

For digital health builders, we are in a time of unprecedented opportunity with the potential to not only provide better products and services, but to rebuild our healthcare system. We are incredibly excited to support the next wave of digital health founders and startups. In the coming weeks and months, we’ll be interviewing some of the best digital health leaders and sharing their advice for how to best execute these new go to markets.

For more of our digital health series, visit a16z.com/digital-health-builders.