This case study is designed for founders and builders to share lessons and insights from operating companies. See disclosures at the end of the content for more information.

As growth investors, we often say great companies start with their numbers. In Revolut’s case, they are required to publish annual financials as a UK company – and their numbers are outliers, to put it mildly:

- Revenue grew 46% to £4.5 billion

- Profit before tax grew 57% to £1.7 billion, realizing a 38% margin

- Retail customers grew 30%, having added 16 million in 2025 alone

- Revolut has Euro-wide penetration with no single country accounting for more than 25% of fee revenue

- Likewise, revenue is now distributed across 6 segments, with no single category responsible for more than 22%

- 11 different product lines exceeded £100 million revenue

- Return on equity (ROE) is a category-breaking 35% (despite over capitalization)

Revolut continues to grow quickly and efficiently—its rule of 75% (defined as revenue growth + net profit margin) is in the highest tier among modern and established financial institutions.

Perhaps more importantly, we believe Revolut still has ample room to run in its existing markets, on both customer growth and monetization. And that says nothing of all the new markets that are potentially ripe for the taking—Revolut just applied for its US charter and has truly global ambitions.

The point is: this is not your grandma’s neobank. Revolut has the potential to become one of the largest banks in the world. There is more ground to break to get there, but we believe the foundations are there.

Throat-clearing aside, let’s dig in.

I. One of the fastest growing financial institutions in the world

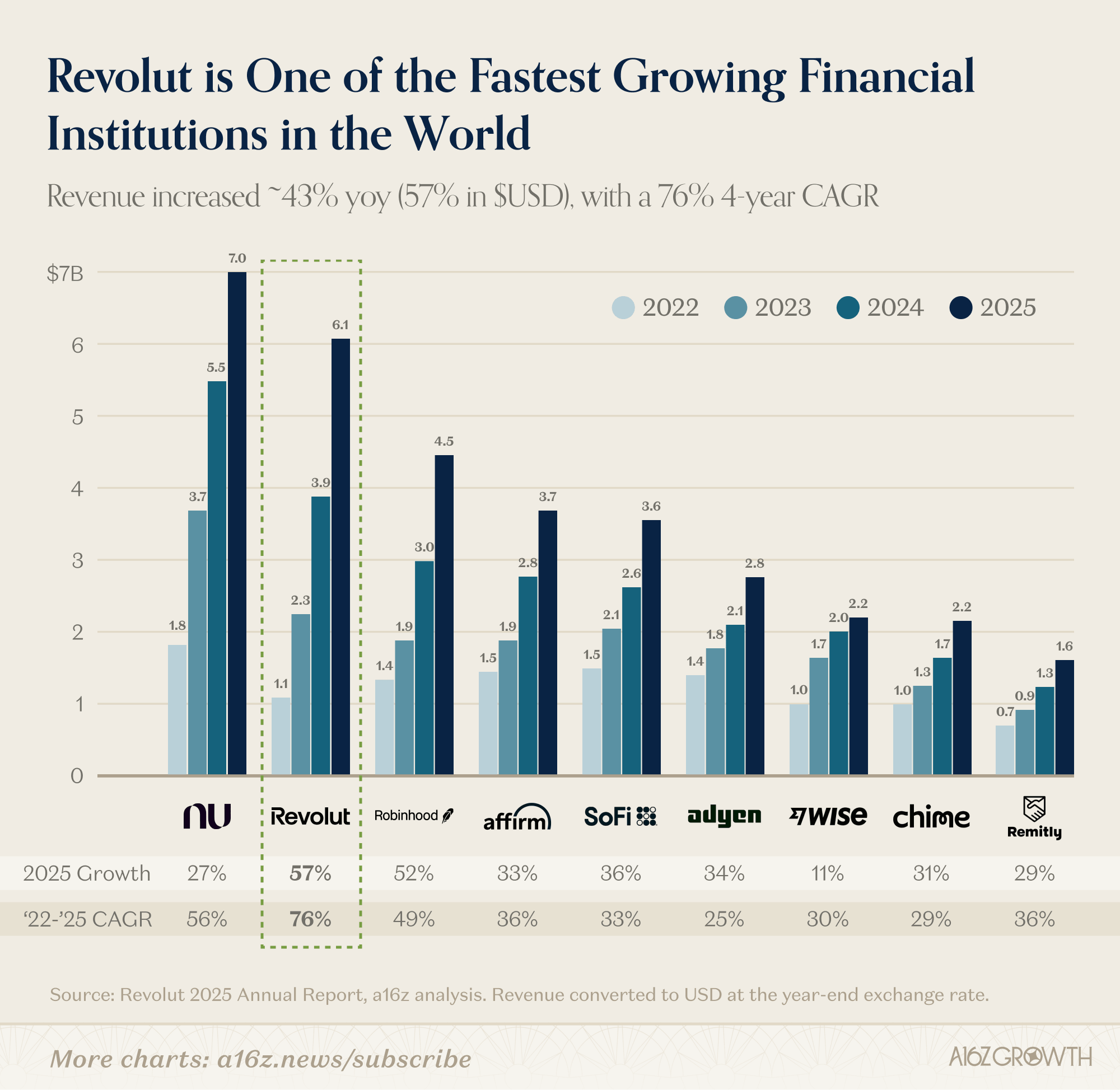

Let’s start with the topline. Revolut is growing revenue at an incredible clip.

Together with NU, they stand in a league of their own relative to the rest of the consumer fintech industry (as demonstrated in the chart below). Since crossing USD $1B of revenue in 2022, Revolut has compounded at a remarkable 76% CAGR (or 70% in GBP) in the subsequent four years, making it one of the fastest growing companies after crossing $1B. That growth is particularly notable when you consider that Europe has a very mature consumer banking industry (unlike developing markets, where NU operates).

Source: publicly reported financials, Revolut annual report. Revenue converted to USD at the year end exchange rate

To put that in perspective, in 2022, Revolut had less (or about the same) revenue than any of Robinhood, Affirm, Sofi, Adyen, Wise or Chime. Now it has anywhere from 33% more revenue to nearly 3x more than any of those other well-known consumer fintechs.

II. Dissecting Revolut’s Growth Algorithm: A Six-Trick Pony (and Counting)

An important differentiator for Revolut is that it’s no one-trick-pony (any more). It has multiple revenue drivers firing, all at once.

Revolut started out by addressing an acute pain point for Europeans: FX fees. With Revolut, Europeans traveling in and out of the eurozone or sending money abroad no longer had to face payment delays or 5% fees charged by their banks.

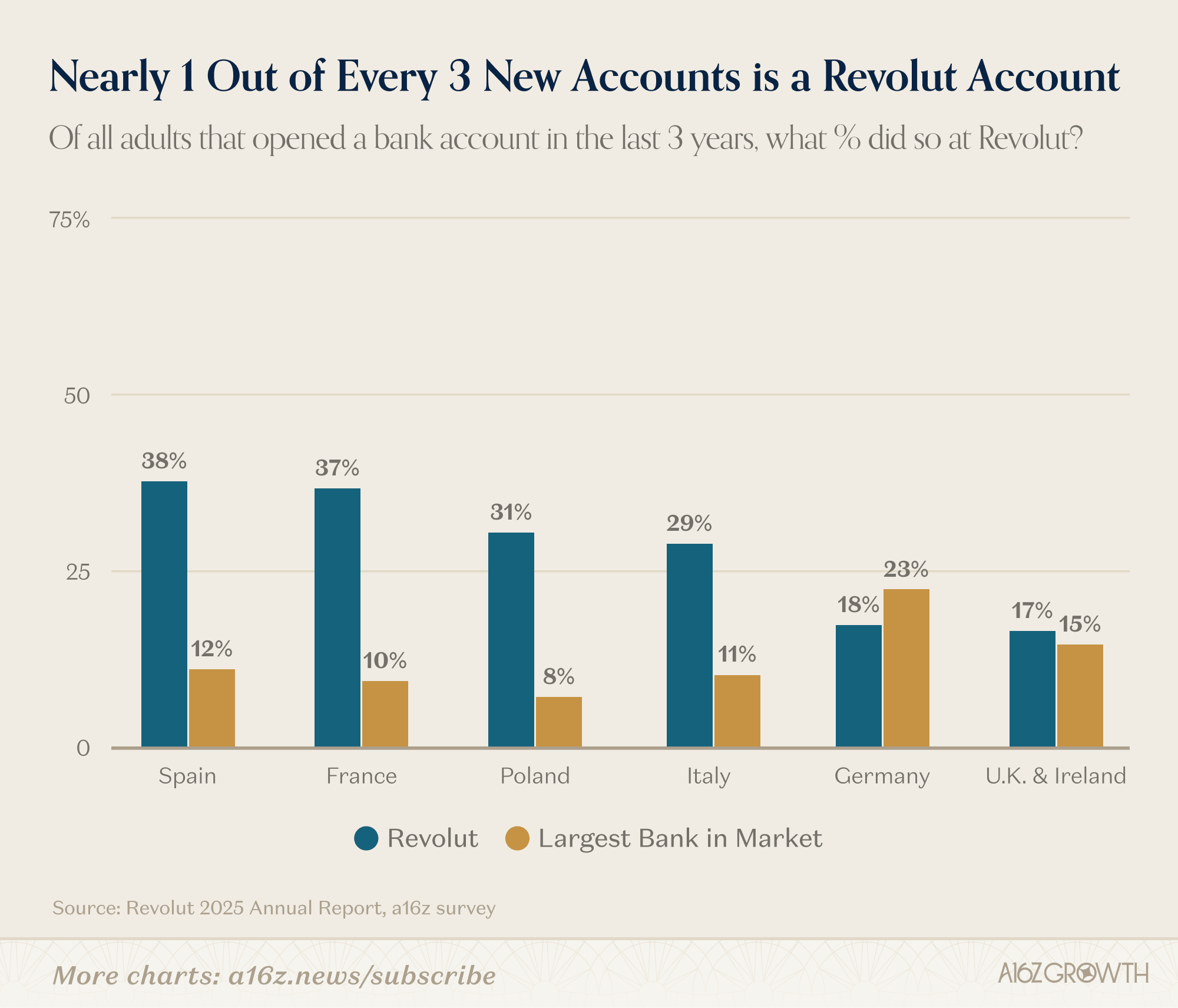

What was once a single-product, geographically concentrated nice-to-have, has become a full-feature business and personal bank that now captures ~1 in every 3 new accounts opened in Europe (the main region where Revolut operates today):

Source: a16z European banking survey, July 2025 (N = 3,500). Survey was conducted in the markets highlighted with a general adult population panel. Respondents indicated where they have open accounts and when each of those accounts was opened.

In Europe, 1 in 5 working age adults now uses Revolut. Revolut’s euro-wide appeal reflects the company’s product velocity and execution, which has been a thing to behold.

Revolut has delivered a full-suite of both personal and business-banking features that are driving growth in very different markets across Europe. Importantly, Revolut’s product suite now increasingly attracts users within the eurozone that may not care about the original FX value prop at all. We’d call Revolut’s platform “feature complete,” except that Revolut keeps delivering new features, so that could be selling them short.

It’s also not just the number of new features and products that Revolut offers. It’s the quality of the execution. Customers love it. The company reported in 2024 that 65% of new customers came either organically or via a referral from an existing customer. And our survey research highlights Revolut customer NPS is more than double the industry average.1

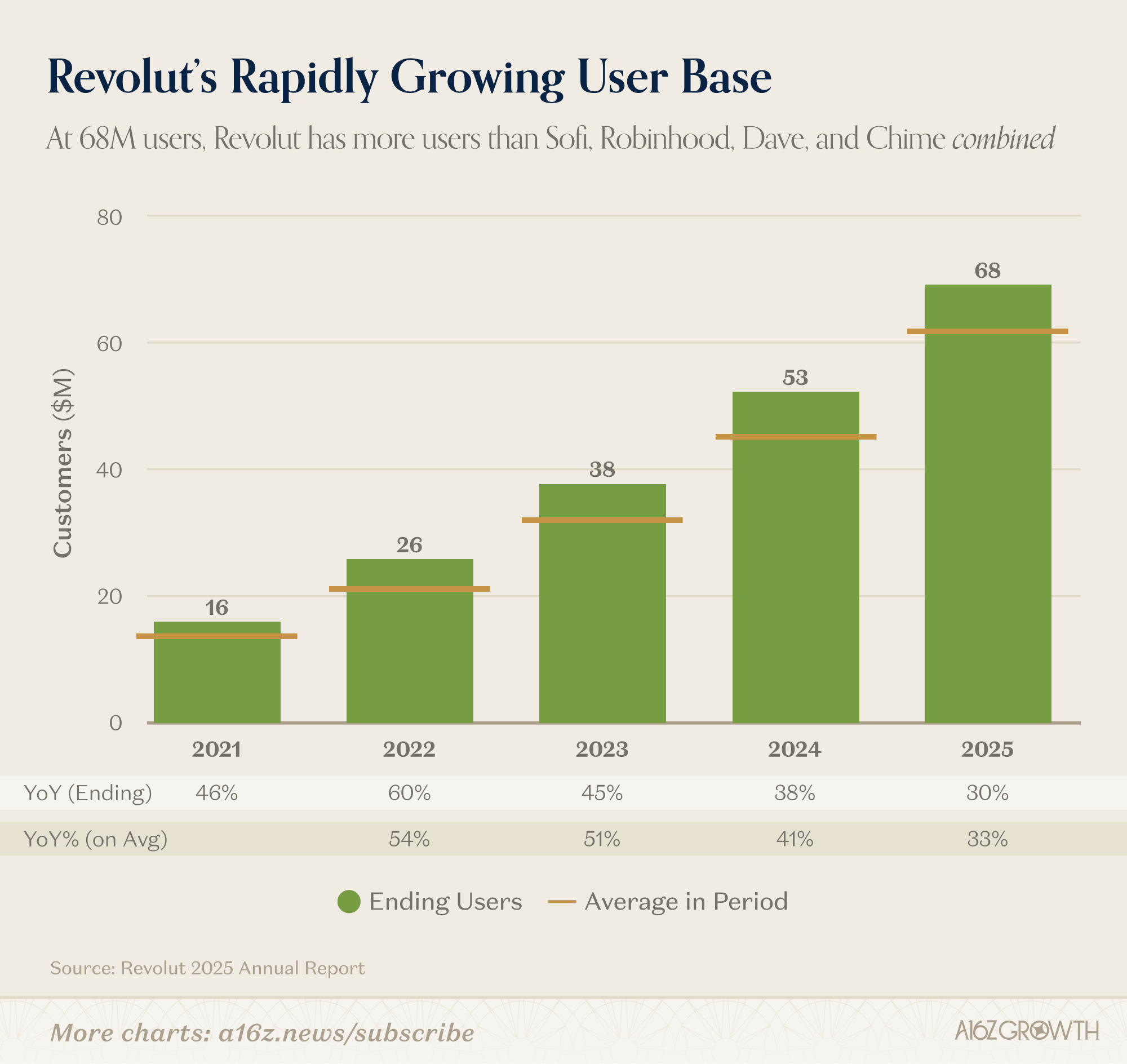

Put it all together, and the net result is that users continued to compound at 30%, reaching 68M at the end of 2025.

Source: Revolut annual report.

To put that 68M users in perspective, JPM—the world’s largest bank outside of China—has ~85M consumer customers (~70M+ considered “digitally active”).

To be clear, JPM’s total AUM makes it orders of magnitude larger than Revolut, but from a sheer reach perspective, Revolut is no longer just a “challenger,”—it’s the real thing. Revolut has more users than Sofi, Robinhood, Dave, and Chime combined.

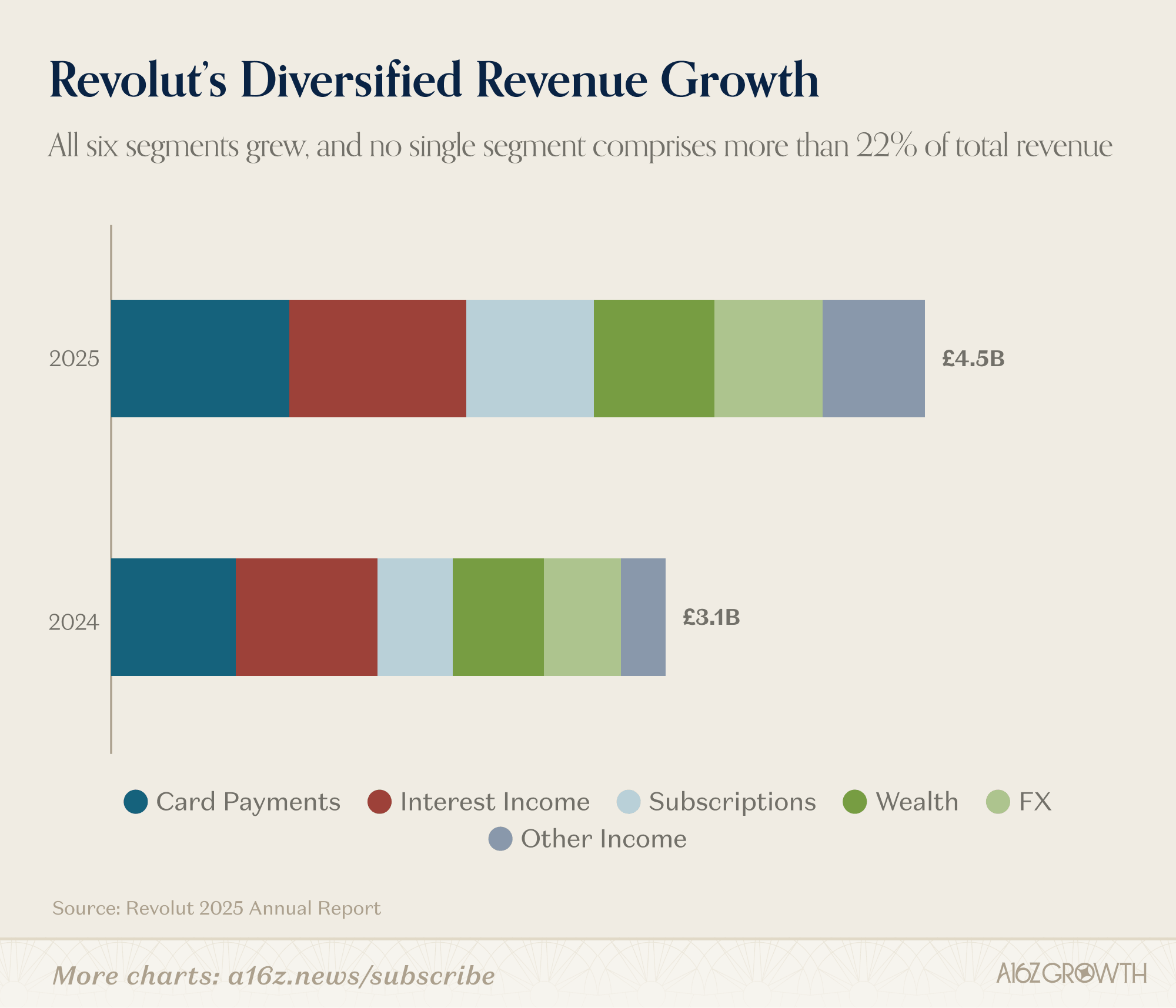

A full product suite has not only continued to attract more customers, but has created an increasingly diversified revenue profile:

Source: Revolut annual report

The company publicly reports 6 main revenue streams:

- interest income;

- card payments;

- wealth;

- FX;

- subscriptions; and

- other income.

All six segments grew YoY, and no single segment comprises more than 22% of revenue.

The business is even more diversified than this would suggest, as every revenue stream may have multiple sub-products underneath (e.g. wealth encompasses both public equities and crypto). 11 different product lines exceeded £100 million revenue in 2025.

Importantly, 76% of the revenue comes from fees, up more than 4 percentage points vs 2024, while interest income accounted for just under 22%. That is the inverse of established banks that make 70%+ of their revenue from interest, and also one of the reasons why Revolut can earn premium ROEs (more on that below).2

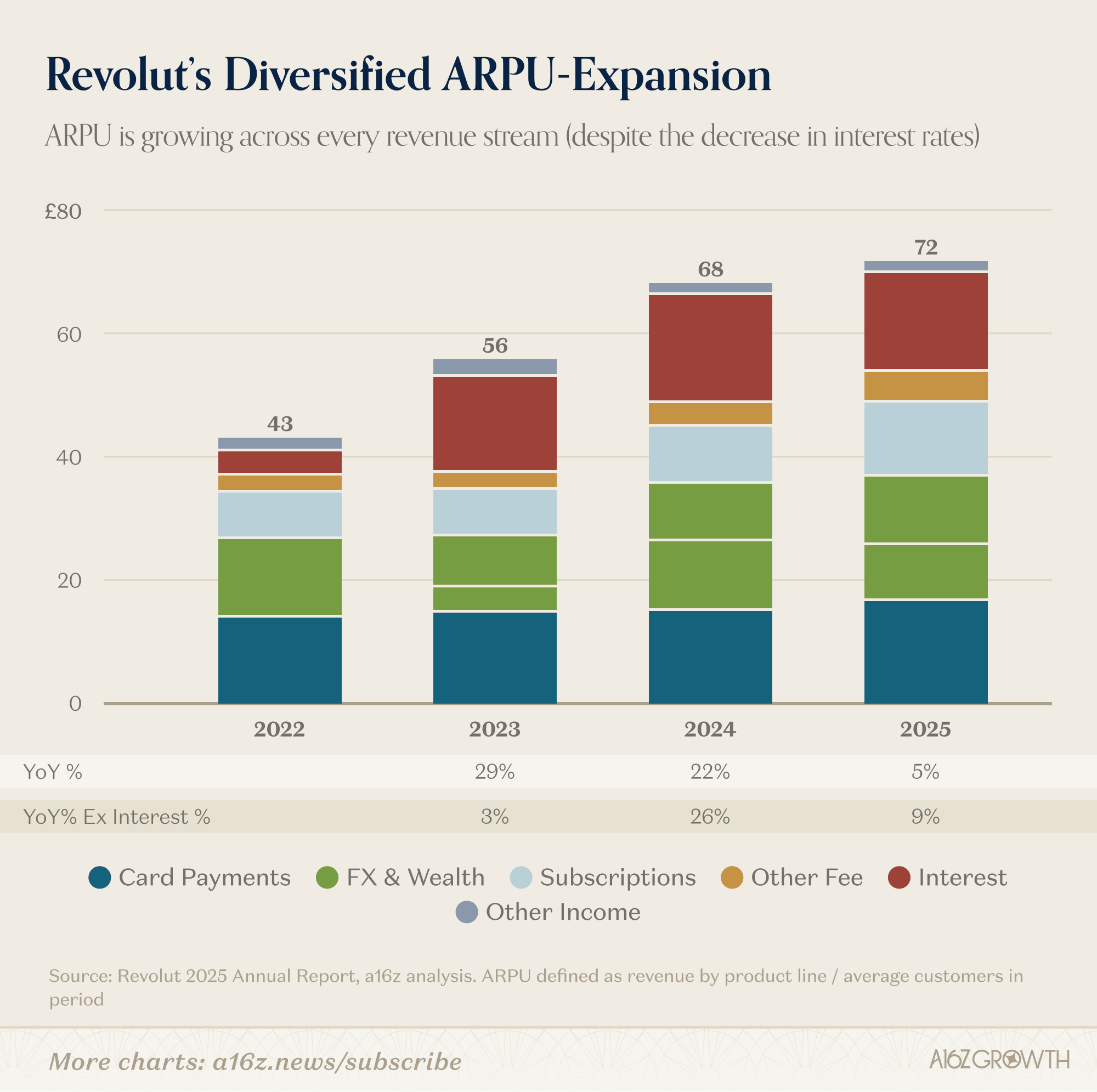

Unsurprisingly, a diversified revenue base has translated into diversified ARPU growth, as well.

Source: Revolut annual report, a16z analysis. ARPU defined as revenue by product line / average customers in period.

Since 2022, every reported revenue stream has grown and aggregate ARPU has grown ~65%, or a 18% CAGR.

The diversification point is important because it supports continued compounding and builds resiliency. In any given year there could be product lines that explode and ones that face headwinds (e.g. a decline in interest rates, as per last year). But, the net of it all can still drive strong ARPU growth, driven by attachment of new products and continued share of wallet gains in the core.

III. Top Tier Efficiency

Revolut has demonstrated rapid user growth, extreme product velocity, and diversified revenue, but we promised efficiency, as well.

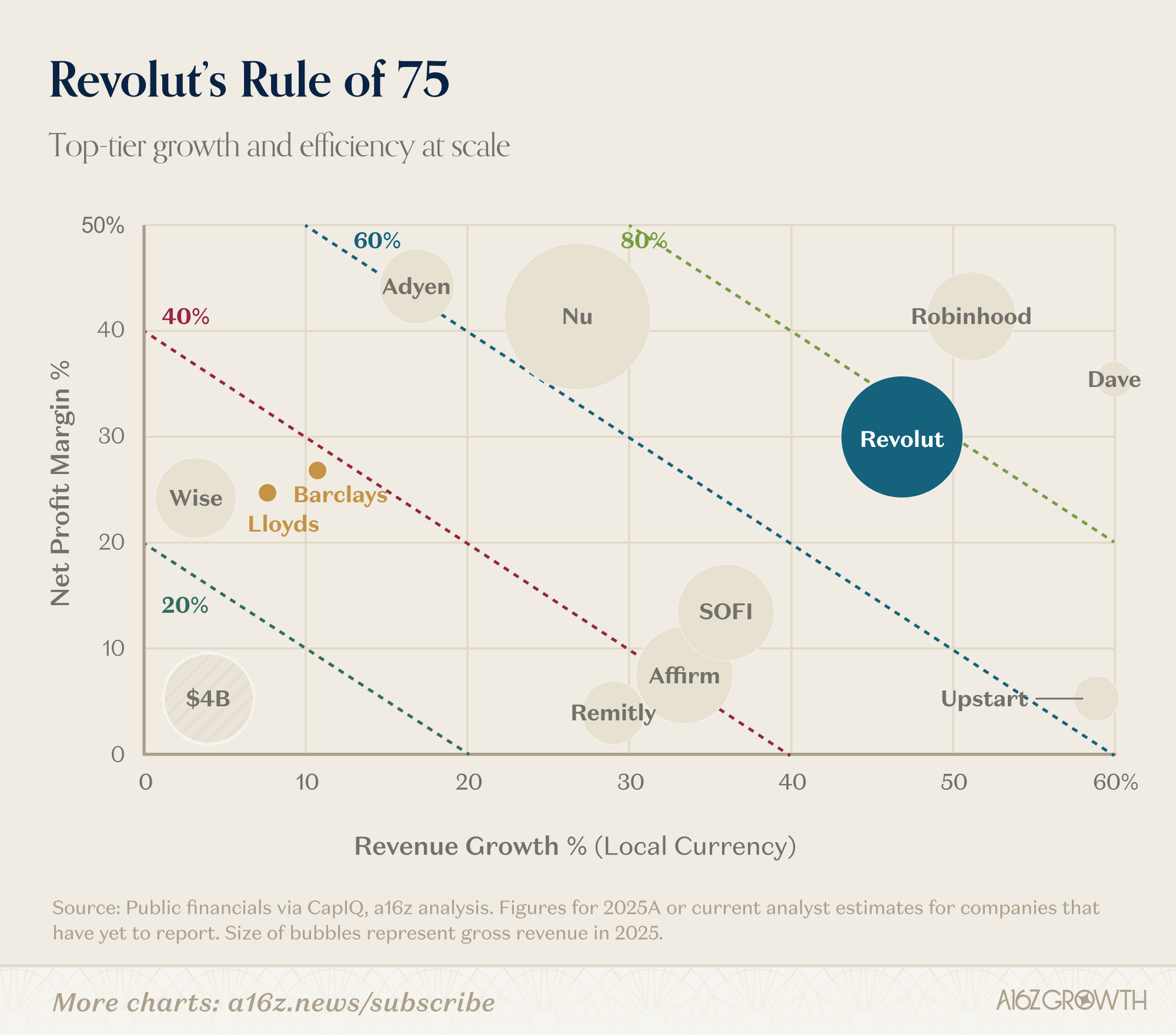

In 2025, Revolut realized revenue growth of 46% and a net profit margin of 29%, resulting in a rule of X (growth + margin) of 75%. So much for Rule of 40!

Source: Public financials via CapIQ, a16z analysis. Figures for 2025A or current analyst estimates for companies that have yet to report. Size of bubbles represent gross revenue in 2025.

The company’s combination of growth and efficiency puts it in rarified air—only a handful of companies have ever achieved Rule of 75% at $1B+ of revenue.

In fact, considering that Robinhood and Dave are expected to grow <30% next year per consensus estimates, Revolut may soon be standing alone at the top of the podium.

Efficiency is rooted in Revolut’s DNA. The combination of prioritizing self-developing its banking infrastructure, driving highly organic growth, and tightly managing costs, has resulted in realizing a net profit margin of 29%. Combined with its limited physical footprint, Revolut now has a meaningful cost advantage over incumbent banks that should compound as the company continues to scale.

To put a bow on it, the company is also demonstrating AI can drive even further operating leverage. Take customer service, for example:

In 2024, Revolut’s Assistant chatbot reduced resolution times by 80%. In 2025, those improvements continued with resolution times decreasing another 40%+ for retail and 50%+ for businesses—all while user NPS increased nearly 12 percentage points year over year. Revolut’s Assistant now resolves over 75% of customer queries.

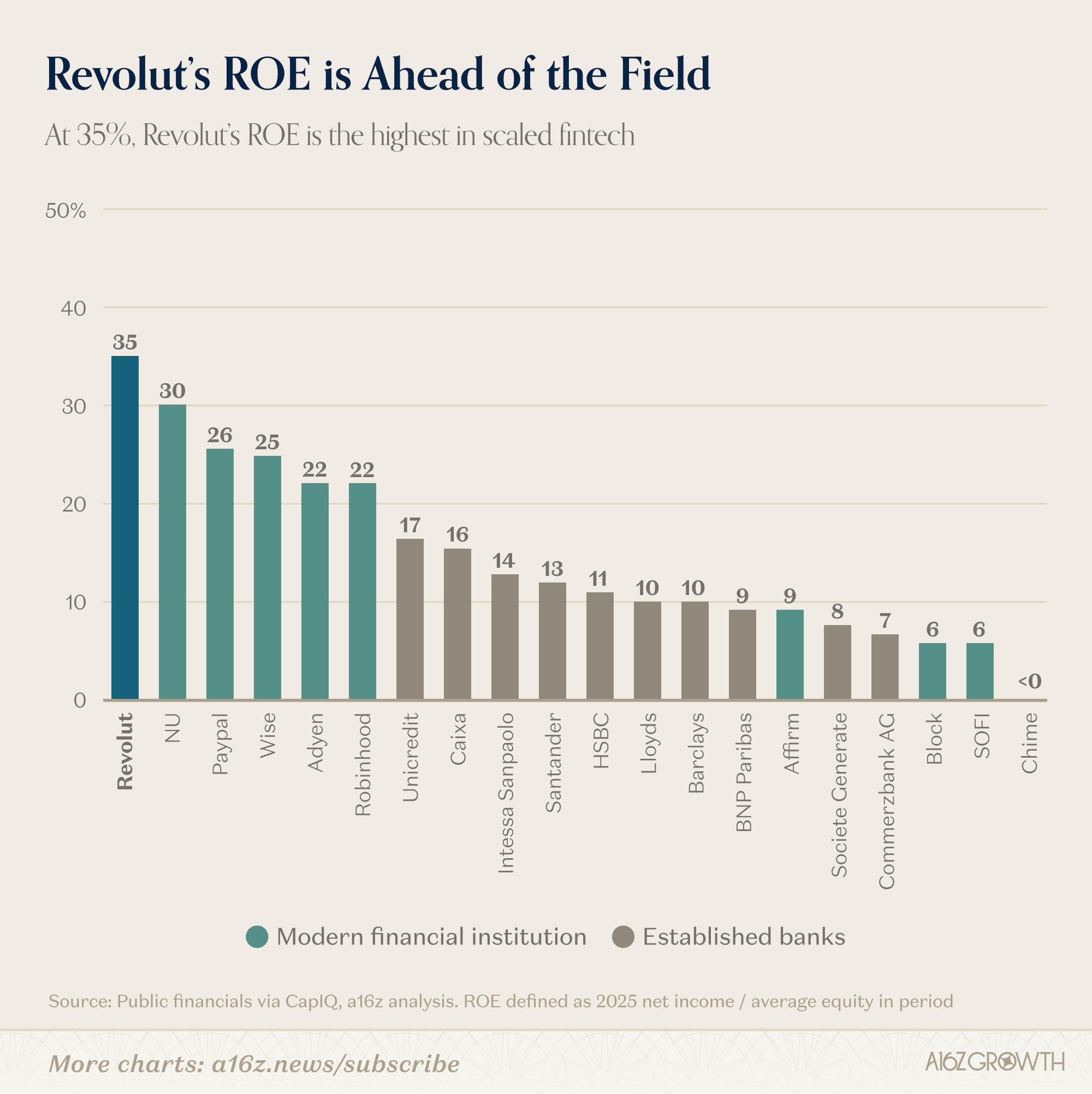

All this efficiency results in Revolut delivering the highest ROE we have seen at scale in fintech (and it’s still continuing to improve). We’ve written in the past about the importance of ROE to bank valuations, and Revolut is a shining example of efficiency at scale.

Source: Public financials via CapIQ, a16z analysis. ROE defined as 2025 net income / average equity in period

Revolut’s 35% ROE is well-above other leading consumer fintechs, and ~3-4x higher than mature banks. Keep in mind that Revolut is ‘over-capitalized’ (i.e. its reported equity is higher than what would be needed under banking capitalization requirements), which means that its ‘true’ ROE may be even higher.

Growth doesn’t get much more capital efficient than that.

IV. Ample Room to Run: ARPU x Users

While Revolut’s results in 2025 are remarkable, we think there is still tremendous runway ahead. Referring back to the company’s core revenue growth algorithm (users x ARPU), both levers have a lot of remaining pull.

Many more users to acquire

Consider that the company reported having 68M users at the end of 2025. As noted above, that’s a lot, but it’s also <15% of the ~450-500M adult population in Europe (excluding Russia). That also excludes the growth opportunities in Australia + Singapore (existing markets), Mexico + Brazil (recent entries), the US (recently applied for bank charter), and more geographies to come.

The point is that Revolut has a lot more potential users to capture.

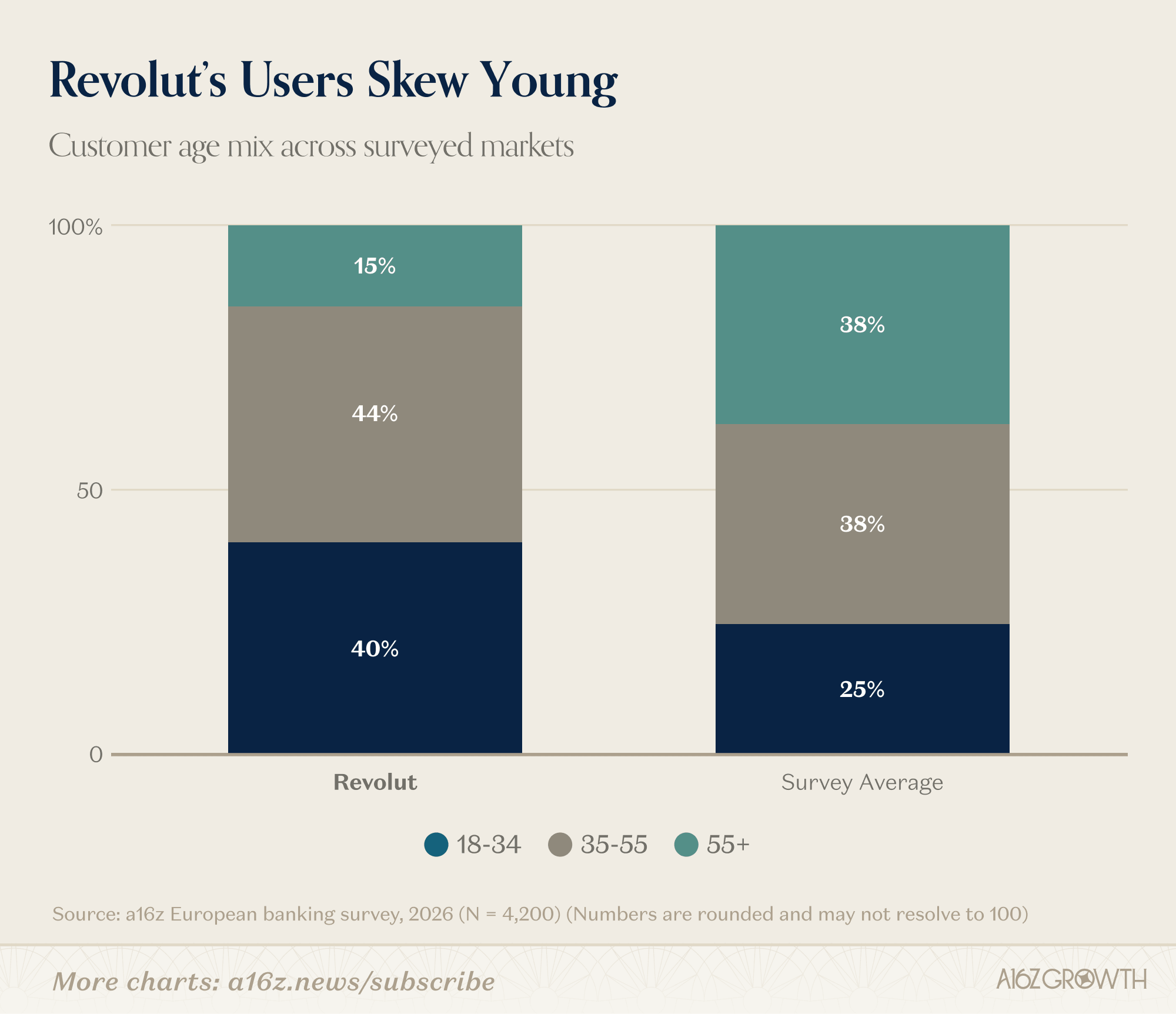

Plus, the current user-mix already demonstrates that the future is unlikely to look like the present. Unsurprisingly, Revolut skews young(er) and digitally savvy—we think these customers are representative of what the majority of the population will seek eventually.

Source: a16z European banking survey, February 2026 (N = 4,200). Surveyed markets were UK, Ireland, France, Spain, Italy, Germany, and Poland.

As Revolut continues to capture a high share of first-time banking customers (and convince older demographics that banking can indeed be a pleasant user experience), their market share should continue to grow.

Importantly, ~25% of Revolut’s users under 35 treat Revolut as their primary account per our survey. We’ll get into that more in a moment, but leaving everything else aside, simply the maturation of that cohort ought to have a profound effect on the future of banking market share in Europe.

ARPU has a lot more potential expansion

The other vector of growth, ARPU, has even more room to run.

Share of wallet in financial services typically shifts over decades, not years. Revolut continues to earn the trust of its customers, as primary account users (per the company’s reporting) grew 45%, outpacing the overall user growth of 30%.

The steep growth of primary account users matters, because when it comes to ARPU, “primary” users are the big prize:

- Our research points to incumbent banking institutions (with seasoned customer relationships) can push their “primary account” share to 60%+.

- Likewise, Revolut primary account users self reported spending and saving ~2x as much money with their primary account as they do with any other open account—and spending tends to increase as customers age;

Simply put, more (and maturing) primary users can translate into higher ARPU, and if incumbent banks are any guide, the ceiling for Revolut’s growing “primary share” is quite high.

Another aspect of the growing “primary” relationship is the still mostly-untapped lending revenue opportunity for Revolut:

- As noted above, currently Revolut derives 76% of its revenue from fees, in contrast to the ~30% typical of mature banking institutions;

- At the end of 2025, Revolut’s Loan-to-Deposit ratio (LDR) stood at just ~6%, compared to ~70-90%+ for established banks (or ~4% if calculated using total customer balances). Lending balances grew ~2x in 2025 and can continue compounding for many years to come.

To be sure, disciplined lending growth takes time. But if the incumbent ceiling is a guide, Revolut will have ample opportunity to expand ARPU much further, by leveraging its balance sheet and providing better loan products to its customers. By way of comparison, simple napkin math for Barclay’s UK consumer and business banking line, implies an ARPU of ~£435 or ~6x what Revolut generates today.

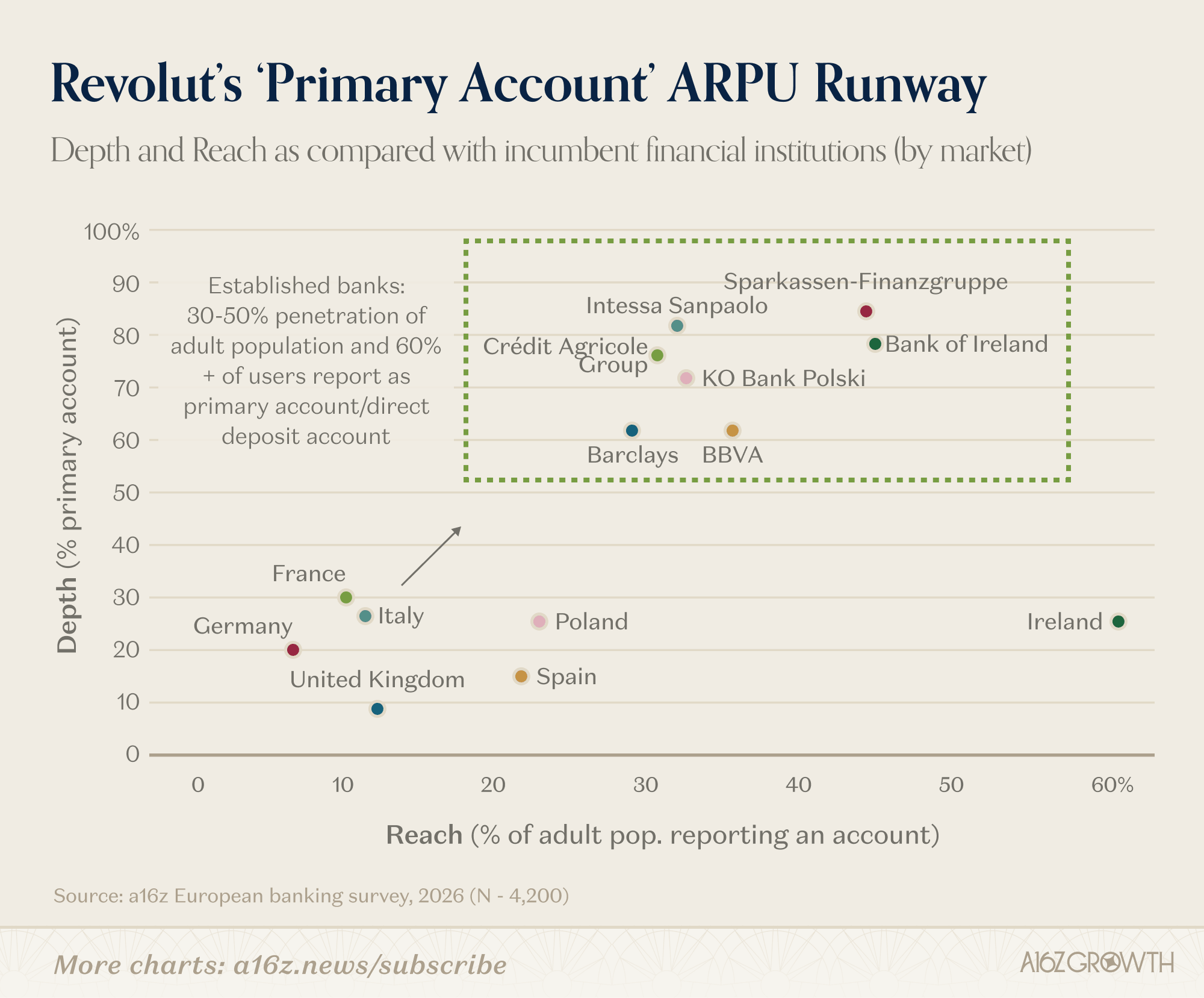

Just to illustrate the point, take a look at where Revolut currently stands, by reach (i.e. penetration) and depth (i.e. primary bank share):

Source: a16z European banking survey, February 2026 (N = 4,200)

Revolut has plenty of runway to keep pushing up-and-to-the-right (or, in Ireland’s case, mostly up), both by expanding its user base and deepening those relationships to “primary.” The latter of which should continue to occur organically, as the younger cohorts mature.

V. Closing Thoughts: Not Just A Challenger Anymore

Revolut’s 2025 numbers matter not only because they are impressive, but because they paint a cohesive picture of a financial institution, and not just a “challenger” bank.

Customer growth remains exceptional, monetization is broadening, primary account adoption is rising, and profitability is strengthening even as the company continues to invest and rapidly scale. That combination is rare in financial services (and in any industry).

There is still execution ahead—particularly in lending, regulation, and expansion into new markets—but reading this annual report, we believe the question feels less like ‘whether Revolut can become a scaled banking platform,’ and more like ‘how large can that platform become?’

The company’s stated long-term goal is “100 million daily active customers in 100 countries.” The march is well-underway.

- a16z 2026 Banking Survey. NPS is defined as the % of respondents that are promoters (-) % detractors, when asked how likely they were to recommend their financial institution to a friend on a scale of 1-10. Promoters = 9 or 10 and detractors = 6 or less.

- CapIQ, 2025