“You don’t own your strategy until you are generating money.”

—Ben Horowitz, a16z founder“Finance is the scrum master for the company.”

—Caroline Moon, former partner at a16z, financial operations

While it can be easy for many CEOs to see the chief financial officer (CFO) as a glorified “scorekeeper,” reporting on revenue, expenses, profits, and losses, a good CFO doesn’t just keep score—they strategically and opportunistically grow your company and help put points on the board. When companies are rapidly scaling, they need an experienced finance executive to develop their business strategy in close collaboration with other leaders in the organization, and allocate capital based on their growth trajectory.

Finance typically has the most access to the company’s performance data. An ineffective CFO tells you what happened in the past without providing the guidance and leadership to chart a path for the future. A great CFO will use this data to help the company make decisions about where and how to invest in growth and ensure that the company has optionality going forward. The best CFOs are also excellent storytellers. They can clearly articulate your company’s vision to investors, which is why they’re excellent at raising capital—private rounds, IPOs, or otherwise.

TABLE OF CONTENTS

TABLE OF CONTENTS

Having the right strategic finance leader in place is critical to scaling successfully. While your company can benefit from a CFO in the early stages, the maturity and size of your company, as well as your time to IPO, will shape how the market perceives your company and who you can successfully recruit.

Typically, in the earlier stages of a company’s growth, a finance leader will develop a strategic plan for scaling, while building out your financial infrastructure and processes—which is particularly critical for your sales team. Experienced later-stage CFOs, on the other hand, typically haven’t personally built out core infrastructure in years, because they’ve relied on large teams and mature systems, and few have a desire to dive back into this hands-on work. We’ve often seen companies that have just found product-market fit and are beginning to scale try to hire a pre-IPO CFO and struggle to attract that level of talent.

Generally, a company should be well on its way to maturity before looking for an experienced pre-IPO CFO. Those CFOs are less likely to accept an offer from a company that is more than 12–24 months out from an IPO, and you’re more likely to benefit from the managerial expertise this type of CFO brings to the table.

Given this, companies typically bring on a pre-IPO CFO when:

- A liquidity event is on the near-term horizon

- Revenues and head count—especially internationally—have grown quickly and increased the complexity of daily business management

- Growth through M&A has emerged as a priority

Writing the MOC

We discuss writing a mission–outcomes–competencies (MOC) document in greater detail in The Hiring Process.

Any all-star CFO will:

- Move an organization away from bean-counting and toward more strategic financial planning

- Maintain frugality while investing in the areas necessary to grow the company, both strategically and opportunistically

- Define the business strategy and where and how to invest more capital or slow spending

- Share insight and analysis across the management team and down into the organization, so that decisions are made using sound financial data

- Secure capital from the right investors at the right price, given the company’s stage of development

- Improve returns from real estate, technology, and infrastructure investments

They’ll also own all of your financial operations. In this piece, a16z partner Jeff Jordan outlines the CFO’s responsibilities and key deliverables, which we’ve repurposed below:

- Control

- Ensure the company has accurate financial metrics (e.g., revenue, expenses, cash flow)

- Help the company stay informed about the performance of those metrics

- As the company matures, manage the audit process

- Financial planning and analysis (FP&A)

- Manage the budgeting and planning processes

- Build a model that projects performance into the future

- Track performance over time, and continually improve the model to be more robust and predictive

- Constantly look for opportunities to suggest improvements to performance

- Accounts payable and receivable

- Manage cash, both collections and disbursements

- Collect money quickly and disburse it slowly to optimize cash management

- Capital markets

- Help the company get the capital they need to survive and thrive

- Optimize the mix of capital between equity and debt where relevant

- Manage the company’s investor base

- Treasury

- Manage the cash in the company intelligently, balancing returns and risk

- Mitigate risks (e.g., illiquidity, currency) to the extent possible

- Tax

- Understand the company’s tax requirements

- Make sure the company is compliant with various tax authorities

- Optimize tax obligations within the bounds of compliance

- Risk

- Assess potential risks facing the company and proactively try to mitigate them

- As the company matures, manage internal audits

Specific to an IPO, the best CFOs will focus on 4 key aspects of the process:

- Getting the company public company-ready, which includes establishing an investor relations capability (in-house or outsourced) and implementing world-class internal controls and financial reporting systems. This gives your CFO good visibility into your current and future financial performance so they can manage your relationship with investors and have tight internal processes to close books and provide timely SEC filings.

- Accounting and tax compliance, including an audit of financial statements, comfort letters, tax planning, and possible use of a second advisory accountant

- Board matters, including appointing independent board members and creating an audit committee

- External issues, including banker selection, exchange qualification and selection, S-1 preparation, and SEC filings

When you’re pulling together criteria for your search, be clear about the outcomes that are most important to you. Some additional considerations include:

- Is it important for the CFO to have worked with similar products or technologies in your space?

- Are there any peculiarities in your business model around licensing, cost accounting, original equipment manufacturer agreements, value-added reseller agreements, etc., that require the CFO to have specific experience?

- Who are the direct reports to this position? Are there any current plans to replace or add staff over the next 12 months?

- Should the CFO have international experience outside North America?

Archetypes and backgrounds

Once you have a clear idea of your specific needs, you’ll want to focus on hiring a CFO with the background and skill set to best address those needs. Below, we break down 4 broad types of CFOs that we see in the market: the career finance executive, the broad-based operator, the M&A and capital markets expert, and the career accountant. Remember, these archetypes are helpful ways to pattern-match your needs with a candidate’s skill set. They’re not hard-and-fast rules, however, and it’s highly unlikely that you’ll find a candidate with just one of these backgrounds.

The career finance executive

The career finance executive is the most traditional type of CFO. They typically have some experience in investment banking or private equity earlier in their career and have most likely been working at private companies. They have deep experience in strategic financial planning and leading key finance groups, including treasury, audit, and business unit finance. They’ll also have a classic set of FP&A experiences, including developing complex business models, operating plans, sales plans, and forecasting processes, managing budgets, and reporting financials to the executive team and board of directors. They’re often at a point in their career where management of key functions is more important than their fluency in technical details.

The majority of CFO searches that we see for growth-stage companies are for this type of executive.

The broad-based operator

This type of CFO is a strong operator who tends to come out of capital-intensive companies or private equity firms and has spent a significant part of their career outside of the finance team, typically as a general manager or leader in business strategy or business operations. As a result, they have a much broader view of both the industry and the ways in which companies operate, and are better positioned to be a strategic adviser to the management team and board of directors.

If you’re hiring this type of CFO, you’ll likely also need to hire a strong controller or chief accounting officer to handle some of the day-to-day financial analysis and decisions.

The M&A and capital markets expert

This CFO is defined by extensive experience in mergers and acquisitions (M&A) and capital markets. They have a strong track record of successfully raising capital from debt markets, private equity, venture capital, and public markets. They have completed M&A deals as a buyer, seller, or adviser. Often, they have spent a significant portion of their career in strategy consulting, investment banking, or private equity before taking on a CFO role, and they are a strong strategist with great networks in the banking community.

This type of CFO often lacks internal operating experience, so you’ll likely also need to hire a strong controller or chief accounting officer.

The career accountant

The career accountant will have a strong technical background as a CPA, coupled with great business acumen. They’ll have experience diving deep into regulatory issues, like establishing and maintaining the practices outlined in the Sarbanes-Oxley Act, and overall risk management. They will also have experience in international accounting and have led audit processes. Most often, these CFOs come out of the semiconductor space and join hardware-focused companies that have more complicated accounting processes.

You’ll likely also need to hire a strong FP&A and operations team to complement their skill set.

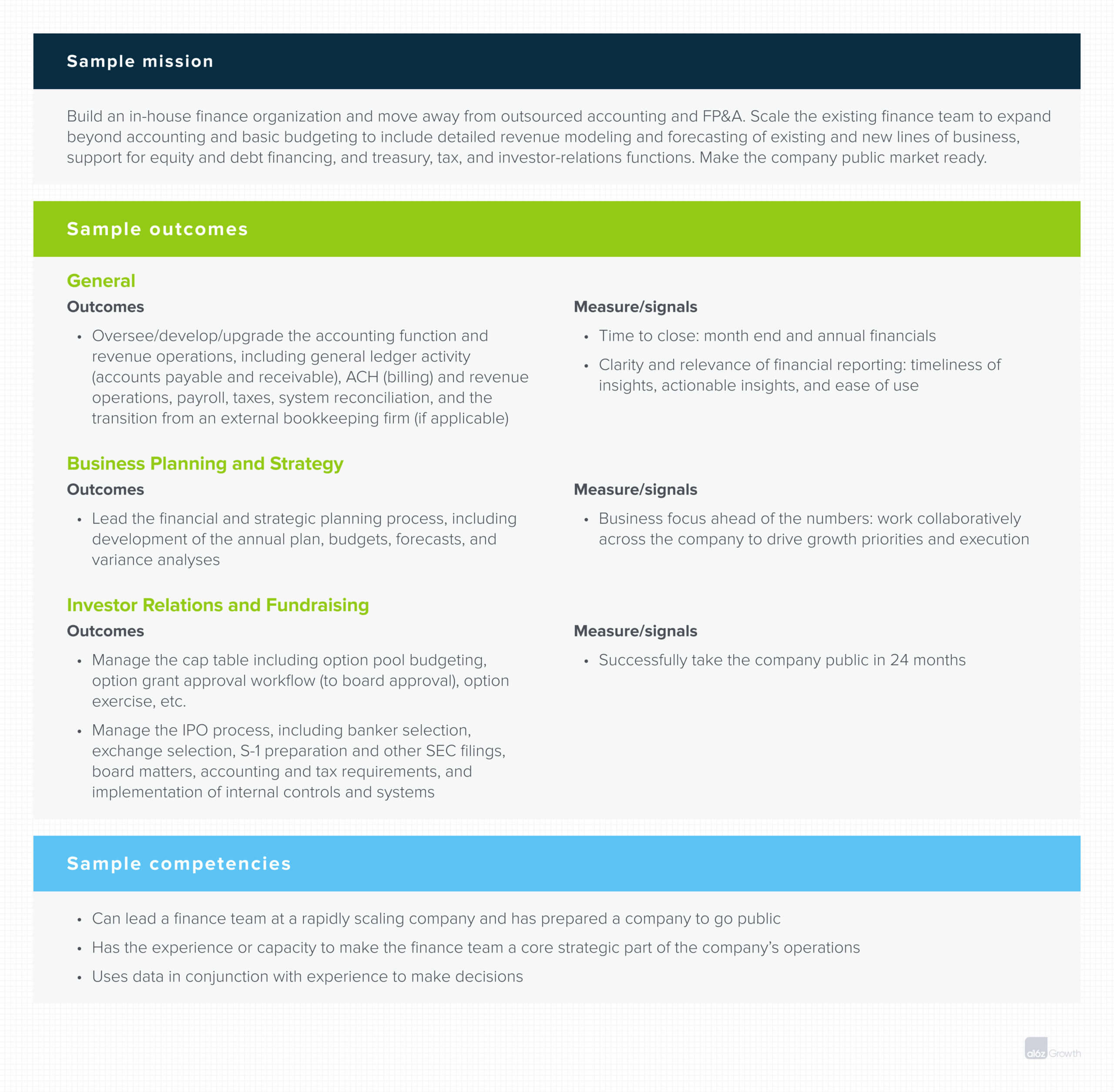

Sample MOC

Setting up your CFO for success

It’s pretty straightforward to figure out whether a CFO has the business experience and financial domain expertise to do the job. It’s equally important, and usually far more difficult, to assess if a candidate will understand how to work with you, the rest of your executive team, and the board of directors to balance the opportunity and risk.

We cover best practices in The Hiring Process, but we’ve included some role-specific considerations below for you to keep in mind when making this hire and integrating them into your org.

Your chemistry is key

The CFO reports directly to the CEO, and the chemistry between the 2 is the single most important element to evaluate during a CFO search process. A true CFO will add credibility and quality to your company’s strategy, and help you articulate the company’s vision. The vision, story, and theme for what’s next must come from the CEO and CFO, and these are especially critical once you become a public company.

The best CFO candidates should be naturally curious and eager to learn more about how your company works. They come to the search process like owners. During periods of uncertainty, you’ll rely on the CFO more than any other executive on the team, and it’s critical that you can trust each other. Think: who will you believe when someone tells you that you’re headed in the wrong direction?

Never have your general counsel report to your CFO

You want to make sure your general counsel and CFO are able to provide checks and balances to keep your company on sound footing legally and financially. We strongly advise against having your general counsel report to your CFO. If you organize your reporting structure this way, your general counsel won’t have the authority or direct line of communication with the CEO to flag existential threats to the company. In worst-case scenarios, we have seen CEOs take bad advice from a CFO and, as a result, face legal action from external regulators.

Look for strong relationships with external financial partners

Along with the CEO, the CFO will be the public face of the company during any capital raises, whether through private or public markets. These responsibilities are at the heart of any CFO role. Therefore, CFOs should have very strong communication skills and work effectively with external players like banks, audit partners, and investors. Backdoor references from your investors are a great way to assess a CFO candidate. In some instances, bankers or investors might even recommend a candidate for the position.

Bring the board into the interview process

Because the CFO works very closely with the board of directors, you should ensure that 1 or 2 of your most involved investors meet one-on-one with the candidate for 45-minutes to 1-hour. They should use that time to both assess the candidate and sell them on your company—emphasizing the career benefits that the role can provide, like connections with high-powered investors or operators.

Thanks to Scott Kupor and Caroline Moon for contributing their hard-earned wisdom and expertise to this guide.

Further reading

We’ve drawn insights from some of our previously published content and other sources, listed below. In some instances, we’ve repurposed the most compelling or useful advice from a16z posts directly into this guide.

Hire a CFO, Jeff Jordan

A great CFO is more than a bean counter. This article highlights the CFO’s strategic value and responsibilities, and offers advice on when you should build out your financial functions and hire a CFO.

Like the CEO, CFOs have a company-wide view on the business. They operate in the middle of all the data flows in and around the business. A good CFO uses this vantage point to make a good company great, leading a high quality finance organization that manages critical responsibilities for the company.

The CFO in Crisis Mode: Modern Times Call for New Tools, Seema Amble and Angela Strange

In the face of economic uncertainty, your CFO is tasked with making both difficult and critical decisions. Amble and Strange discuss the CFO’s current tech stack, as well as new tools and opportunities for CFOs to embrace the strategic side of their roles and address things like headcount planning, cash flow, resource allocation, and sales.

Cash, Growth, and CEO ❤️ CFO, a16z podcast with Ben Horowitz, Scott Kupor, and Caroline Moon

Are you missing the signs that you’re running out of cash? By creating a productive partnership with your CFO, you can move beyond the typical math and spreadsheets to identify leading indicators while balancing growth, strategy changes, and more.

Navigating the Numbers, a16z podcast with Jeff Jordan, David George, Caroline Moon, and Das Rush

Your income statement, balance sheet, and cash flow statement not only show you how your company is doing, they’re some of the best tools you have to run it. Learn about common mistakes, how to determine if you’re running a healthy company, and how you can use your numbers to navigate crises.