Every meeting a busy founder takes is time away from building the company. So it’s understandable why engaging corporate development groups is believed to be a waste of time, unless you’re selling your company.

But there are actually several benefits to engaging with corporate development — it just depends on your goals, and on the particular mandate of the group you’re engaging. The composition and focus of most corporate development groups is simply too varied to narrowly define the whole function, and the expertise and responsibilities of groups varies widely from company to company. Furthermore, the scope of corporate development activities actually extends beyond just M&A, to include strategic partnerships and even go-to-market opportunities.

Understanding these differences is critical to deciding whether corporate development is useful for your startup or not…

Engaging corporate development for M&A transactions

Generally, corporate development is focused on “inorganic” activity for a company: partnerships with, investments in, acquisitions of, or divestitures to other companies. But the expertise and scope of groups varies as follows, and each of these models have different implications for how and who to engage on the corporate development team.

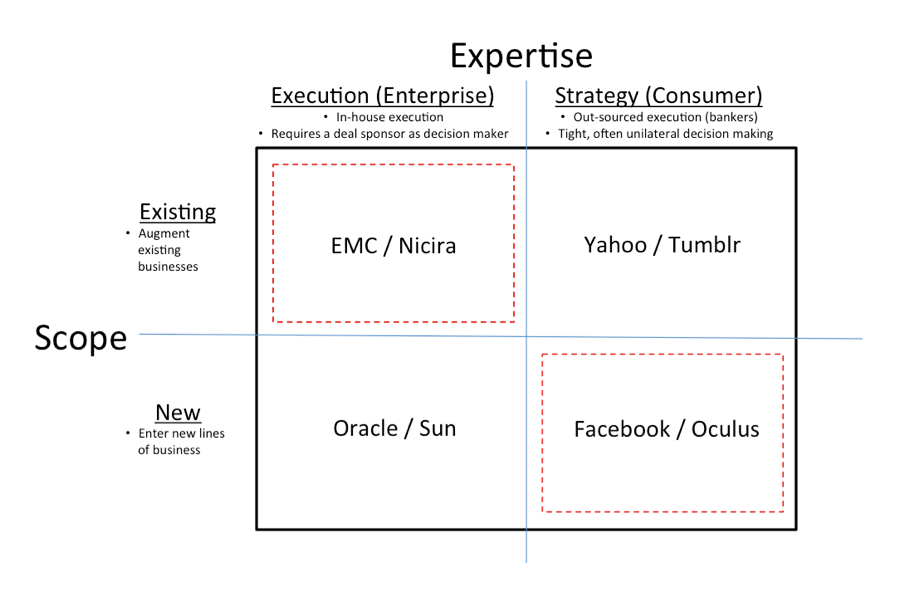

Execution Focused

In large, established organizations with discrete business units and strategy teams, corporate development groups are often purely execution-focused — the business unit GMs decide the “who and the why”, and the corporate development teams execute on the “what and the how”.

Enterprise companies tend to be organized this way. So companies like Cisco and EMC are far more likely to acquire companies that augment their existing business units vs. establishing an entirely new business line. (And if they did the latter, it would likely be of a business at scale — think of the difference between VMware’s acquisition of Nicira vs. Oracle acquiring Sun Microsystems).

Implication for startups: Build relationships with the business unit GMs — i.e., potential deal sponsors — early, and focus less on corporate development engagement.

Strategy Focused

On the flip side, other corporate development groups specialize in implementing strategic imperatives, so are focused on pursuing lines of business that could create entirely new growth trajectories. Decision-making, and the idea-generation that leads to these decisions, also tends to be more centralized in these organizations.

Consumer businesses generally fit this mold. In this scenario, though, it is far harder to predict the type of businesses — let alone the specific company! — that acquirers would pursue, since the complementary businesses are not tightly integrated with the core business. Take Facebook’s acquisition of Oculus for example.

Implication for startups: Build relationships with the corporate development group, and also identify — and nurture — unilateral decision makers.

Engaging corporate development for strategic investment

Another function that resides in corporate development is when large corporations want to invest in startups. How such a strategic investor works with its portfolio companies — and what motivates them — is important for startups to understand before deciding to work with one.

In our experience, strategic investors (“strategics”) are motivated by one of four things:

1. They have negotiated or have line-of-sight to a commercial deal, and would like to make an investment to fully realize the benefit of that deal.

2. They want the startup to work on their platform or in their ecosystem.

3. The technology or space is highly relevant to them, so they would like to use strategic investment as a path to acquisition.

4. They are after purely financial returns.

Implications for startups:

We typically advise our founders to avoid scenarios #3 and #4, because it can complicate M&A processes. Or, it can lead to an uncomfortable situation if your investor decides instead to compete with you!

Startups should be fine with reasons #1 and #2, however, because a partner with “skin in the game” as an investor is more motivated and has aligned interests. (A strategic investor that appears on your cap table, but nowhere in your business, is harder to explain — and it’s something you will be asked by subsequent investors, whether financial or strategic.)

But why should startups even bother with these corporate investor partnerships in the first place? The reason is because strategics can accelerate your business — through everything from distribution to revenue to credibility in new markets around the world. Some examples of this include:

…ecosystem partners — such as Cisco, Salesforce (ItsOn, Box)

…technology partners — such as Qualcomm, Microsoft (21, Foursquare)

…distribution partners — such as Telefonica, Docomo (Cyanogen, Coinbase)

…product partners — such as GE (Quirky)

…customer partners — such as Citi, NYSE and 7-Eleven (Pindrop, Coinbase, Belly)

…geographic partners — such as Alibaba, Rakuten (Lyft, Pinterest)

How to engage corporate development in the first place

For companies still at the very early stages, the typical advice is to do nothing, especially for the M&A scenario. One reason for this is that corporate development professionals have worked on dozens of completed strategic transactions (and untold numbers of failed ones) in their careers, while founders have worked on maybe one such deal (if any). This disparity of experience is at the root of many of the missteps we’ve seen over the years and can be mitigated by proper preparation.

While every partner, transaction, and situation is different (and we tailor our advice to individual situations), here are some basic answers to a few frequently asked questions:

Q. Should we send the corporate development group confidential information?

A. At first, you should share only the information that you would be comfortable sharing broadly anyway.Q. Should we sign an NDA?

A. Yes — and one with a non-solicitation of employees agreement!Q. How should we decide whether to take that second or third meeting?

A. Only if, given the scenarios above, you see a clear benefit to you that justifies making that time.Q. Should we let the corporate development group meet the whole startup team?

A. We typically advise our companies to reserve this until very late in the process, post-term sheet even.Q. What if we have multiple strategics after us? Which one do we pick?

A. Actually, this is what you want! Competition drives both timing and terms — including price.Q. Will working with one strategic (outside of M&A) preclude us from working with others?

A. It depends — companies often work with multiple strategics, but usually not direct competitors.Q. Are there any red flags we should look for in the term sheets?

A. Lots. For this, it’s best to enlist your board, investors, and legal counsel. They’ve seen enough examples given their vantage points to be able to quickly spot any potential pitfalls.

* * *

Aside from M&A or strategic investment transactions, corporate development relationships can be valuable “sherpas” to help guide startups through a large organization. Sometimes, they can lead to unexpected opportunities.

Overall, think about your engagements with corporate development as investing in and building long-term relationships, where the (time-efficient) ideal is that the right relationship is in the right place at the right time when you need it. Regardless of how you go about it, though, one truism remains: Generating competitive tension is critical to creating good outcomes. So, if you decide to talk to one corporate development group, make sure you are talking to more than one… and at the right cadence to grow the relationship over time.

Thanks to Tyson Clark and James Loftus for their inputs on this piece.