Over the past half century, Wall Street was completely revolutionized by computers.

Not so long ago, human brokers on the stock exchange floor haggled to buy and sell every stock, writing their agreements on pieces of paper.

But in 1971, the NASDAQ, the world’s first electronic stock exchange, was introduced. Electronic trading platforms followed in the 1980s, and the rise of the internet in the 1990s brought online brokerages like E*TRADE.

In the 2000s, technology radically changed not just how stocks were traded, but the decision behind which stocks to trade. Firms like Citadel, DE Shaw, and Two Sigma started to employ High Frequency Trading, computer algorithms capable of executing thousands of trades per second.

Quants, the algorithm writers, overtook master traders, who manually studied companies. Algorithms overtook hunches. The quant funds who led the pack raked in hundreds of billions of dollars.

100% of stock trades used to be made by humans. Today, 80% are made by computer algorithms.

AI is about to bring a similar revolution to healthcare.

Over the next few decades, at least half of the $4.3 trillion dollar American healthcare industry will be AI-driven.

AI will drive drug discovery, proposing medicines not yet dreamed up by man. AI will play a key role in diagnosis, helping humans know what’s wrong sooner so they can get access to life-saving treatments. AI will change how care is delivered, as every human will have a world-class AI doctor in their pocket. And AI will eliminate a lot of the infuriating back office minutia in healthcare.

The markets are significantly undervaluing this opportunity.

This is partially because the market only knows non-AI healthcare companies today. In the digital health public markets, there are (1) tech-enabled service companies that have excelled in speedy go-to-markets, but have been low margin due to human labor, and (2) healthcare SaaS companies that are high-margin, but have struggled in go-to-market because of the difficulties of selling SaaS to human-loving healthcare entities.

AI health companies will not have these limitations. Margins will be way better than human services. Go-to-market will be far easier because AI companies can sell “AI humans,” as opposed to fighting the uphill battle of selling software on which healthcare companies must train their overworked employees. Just like the internet completely transformed go-to-market for software companies, AI will transform go-to-market for healthtech companies.

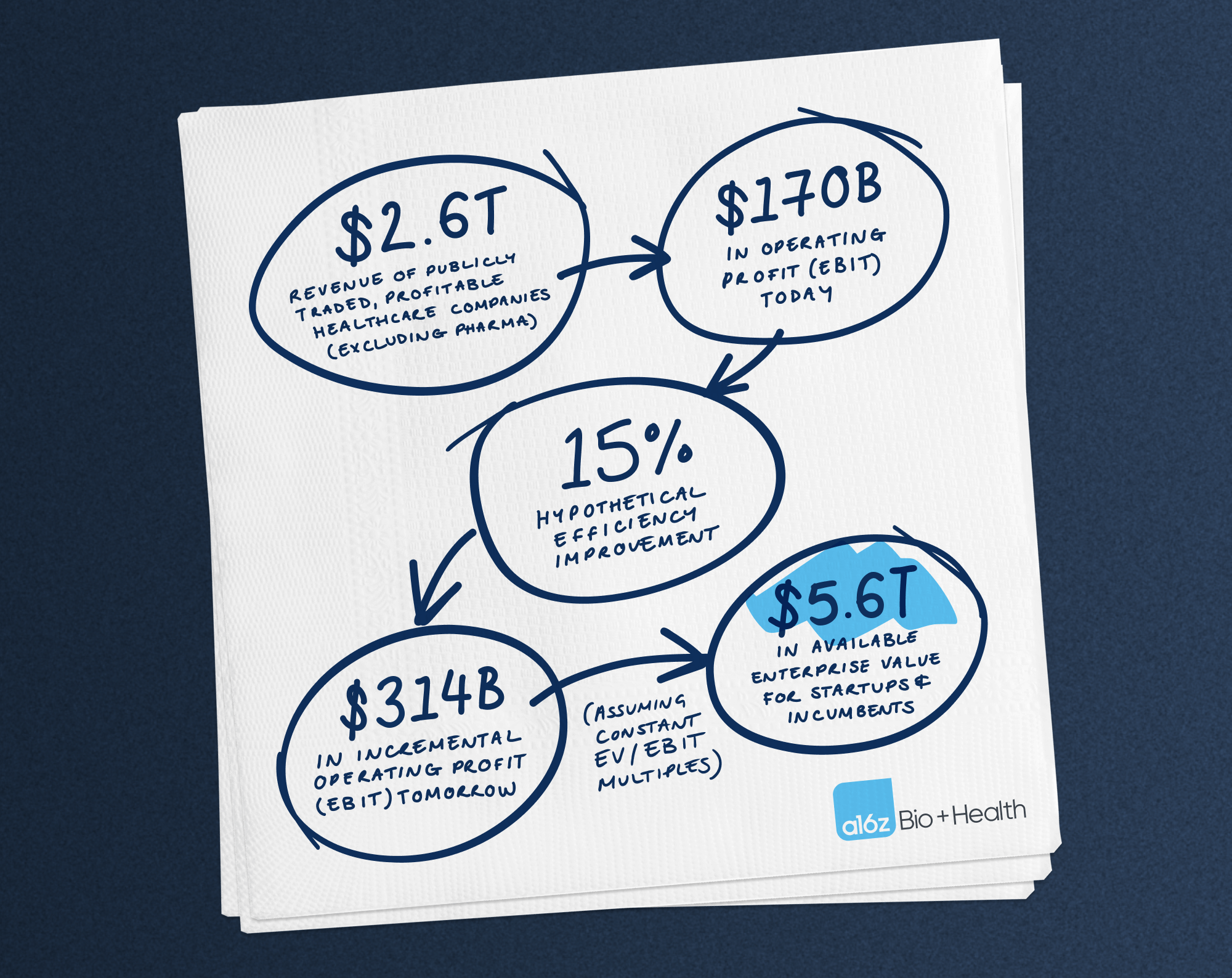

To demonstrate the scale of the AI opportunity in healthcare, consider that publicly traded, profitable healthcare companies today (excluding pharma) generate $2.6 trillion in revenue and yet turn only $170 billion (~6.5%) of that revenue into profit. Imagine if these were able to achieve even a 15% increase in efficiency1 for having infinite access to low-cost AI “workers.” That alone would drive $314 billion more in operating profit and ultimately $5.6 trillion in incremental enterprise value, even assuming no improvement in valuation multiples or growth in topline revenue. That would nearly triple the enterprise value of profitable public healthcare companies, and we believe that number is conservative!

Source: CapIQ as of 11/30/2023; Andreessen Horowitz analysis

So will this happen? What kinds of companies will capture this AI opportunity?

We can look to the introduction of the internet in the 1990s to see what happened in the last technological revolution. Pre-internet—in 1990—the biggest companies at the time were largely in non-tech industries like oil and gas (Exxon Mobil), pharma (Merck), CPG (Coca-Cola), auto (GM), and telecom (AT&T). While some small public companies in the 1990s like Apple and Microsoft embraced the internet and 500x-ed to become the biggest companies in the world, the vast majority of value accrued to startups founded as the internet was taking off. Today these startups—Alphabet, Meta, Amazon—have knocked all of the aforementioned biggest companies of 1990 off the top 10 list.

The same will likely happen with AI in healthcare. While some public healthcare companies will transform their strategies with AI and excel because of it, the vast majority of the value will accrue to AI health companies being started now.

Today resembles the early days of the internet. Will there be an AI bubble that bursts just like the dot com one did? Probably. But the best companies will rise from the ashes and transform human health.

***

1“15% efficiency improvement” denotes a 15% reduction in COGS and 15% reduction in OpEx