This first appeared in the monthly a16z fintech newsletter. Subscribe to stay on top of the latest fintech news.

IN THIS EDITION

- A contrarian take on recovery prospects

- The pandemic’s impact on real estate

- Big fintech seeks partners to go global

- WhatsApp Pay’s short-lived launch

- The big picture behind Hertz’s stock snafu

- The partner bank boom

Want more a16z?

Sign up to get our best articles, latest podcasts, and news on our investments emailed to you.

Thanks for signing up.

Why millions of missed credit payments don’t spell doom

Anish AcharyaNearly 15 million credit card accounts deferred payments due to financial hardship programs in April, according to TransUnion. The news prompted foreboding comparisons to 2008 and hand-wringing over an impending wave of defaults. The concern is justifiable — payment history is the most important driver of credit scores. Widespread missed payments would depress access to credit nationally, leading to lender pullback and a cascading series of economic damage.

However, there are a number of reasons to be hopeful this time around. First, the CARES Act takes great pains to protect consumers’ credit; lenders must report deferred payments as current, which means consumers are not penalized for skipping a payment. Given that 13 million people work in food service alone, it’s unclear how many workers are experiencing temporary hardship versus how many are insolvent. It’s obvious many are struggling; at this point, though, it’s unclear how many of those deferred payments will actually become delinquencies (30 to 180 days late) or, eventually, charge-offs (+180 days). TransUnion recently began selling data to lenders that indicates which consumers are in deferment and for how long.

Second, early reports indicate that two-thirds of workers who qualified for stimulus benefits received more take-home income than they otherwise would, due to unemployment and federal relief measures. That indicates a higher degree of likelihood that consumers will be able and willing to get back on track with their payments. (Here, policy will continue to play a major role, as supplemental unemployment benefits are currently set to expire in July.)

Finally, consumers are overall in better financial health than they were in 2008 — savings rates are elevated, consumers have nearly three times more equity in their homes, and banks are better capitalized than ever before.

Viewed as a whole, it’s reasonably likely that the credit markets will recover as the economy reopens and consumers get back to work. Though we may not return to an environment of “benign credit risk” for some time, I’m optimistic that this recovery will be quicker than 2008.

- The Most Human Technology Ever Made Anish Acharya

- What Happens to Design After AI? John Maeda, Paul Bakaus, and Anish Acharya

- What’s Next for Consumer AI? | Josh Elman Joins a16z Josh Elman and Anish Acharya

- Building AI Agents for Enterprise Operations Pablo Palafox, Luis Paarup, Anish Acharya, and Olivia Moore

- Investing in Ethos Anish Acharya, James da Costa, and Olivia Moore

The pandemic's impact on real estate

The economic crisis poses unique challenges for homeowners, prospective buyers, renters, and landlords — not to mention policymakers. Supplemental unemployment benefits are slated to expire next month, though millions remain out of work. “I worry about a cliff coming,” particularly when it comes to renters, says Richard Green, director of USC’s Lusk Center for Real Estate. “If Congress doesn’t come back and pass something, then I think we are going to face real problems toward the end of the summer.”

In this two-part series on the a16z Podcast, we examine the pandemic’s fallout from two perspectives: that of homeowners and buyers; and that of renters and landlords, particularly those in large cities like New York and San Francisco. How has the crisis affected home prices? Is the rumored exodus from densely populated cities real or overhyped? What’s the ripple effect of eviction freezes and a record number of homes in forbearance? And how can tech streamline the inefficient processes of renting, buying, and selling a home?

Listen now:

Real Estate in a Pandemic: Homeowners and Buyers (Part 1)

Real Estate in a Pandemic: Renters and Landlords (Part 2)

Big fintech players seek partners to go global

Seema AmbleWe’ve seen a number of U.S.-based fintech players announce international moves in the past month, many through partnerships. Square acquired Verse, the Spanish peer-to-peer money transfer application. WhatsApp Pay launched in Brazil (that is, until Brazil’s central bank promptly suspended it). Facebook and PayPal invested in Gojek, the Southeast Asian ride hailing, food delivery, and mobile payment company. Uber partnered with the payments gateway Flutterwave. Big fintech players clearly recognize the massive opportunity outside the U.S. — but why are they partnering with local players, rather than launching directly?

Fintech is default local, not default global. Unlike software or a social network that can be “turned on” in any geography, fintech products must receive local regulatory approval, offer local payment methods, and work with local bank partners — all of which takes time, talent, and money, oftentimes a significant, dedicated team. Additionally, over the last 10 years, local fintech players have emerged around the world, posing formidable competition for foreign entrants.

Broadly, the strategy behind international partnerships is typically directed by some combination of the business needs listed below:

- Partner to drive adoption. In countries with strong local payment methods, partnering can help build trust and reduce friction in signing up new users. Uber’s partnership with Flutterwave is a good example: Flutterwave gives Uber users the ability to top-up their Uber Wallet using local money transfer services like M-Pesa in Kenya, EFT in South Africa, or the Verve payment card in Nigeria.

- Partner for influence. A strong local player can provide bargaining power, particularly where regulatory approval is more difficult to attain. One example is Facebook’s investment in Reliance Jio in India. WhatsApp Pay has been stuck in private beta in India since 2018 as it awaits approval from the government. An investment in Reliance Jio could help overcome some of those regulatory hurdles.

- Invest to learn. Investing can be a good way to learn more about a market, especially where a local competitor already exists and a license is hard to achieve. An investment may even be a path to acquisition. Paypal has pursued this investment strategy in a number of markets: Toss in South Korea, Mercado Libre in Latin America, and, this month, Gojek. Stripe has also gone this route by investing in PayMongo in the Philippines.

- Acquire to expand. Outright acquisition is primarily a tactic to build new core markets. Square’s acquisition of Verse is one example. Square’s Cash App is currently only in the U.S. and the U.K., while Verse is live in 12 countries and licensed in over 30. The acquisition allows Square to enter Europe fairly quickly, reportedly for just 30 to 50 million euros. Acquiring an existing consumer brand can be tricky — it requires a similar demographic and marketing message. Verse aligns well with Cash App’s young target demographic. And similar to Cash App’s $Cashtag, Verse customers use the $VerseTag to identify themselves when sending and receiving payments.

Although there are companies that have gone global directly — PayPal, for example, is now in 200+ countries and derives 47 percent of revenue from outside the U.S. — that network took years to build. Even after PayPal set up a European office in 2007 and became a Luxembourg-based bank, much of its non-U.S. payments was concentrated in the U.K., Germany, and China (according to its 2015 10-K). In 2015, PayPal acquired the international remittance company Xoom to bolster its international business, followed by a number of other partnerships and acquisitions. Moreover, PayPal’s business model is predicated on money transfers, much of which happens across borders. In contrast, many European neobanks have struggled to gain users outside their home launch markets, particularly when lacking an international money transfer use case.

In the coming months, we’re likely to see similar acquisitions, investments, and partnerships by big fintech — rather than attempting to go it alone — as these companies look to go global.

- Is Software Losing Its Head? Seema Amble, Elena Burger, and Steven Sinofsky

- Investing in Probook Alex Rampell, David Haber, Olivia Moore, and Seema Amble

- Is Software Losing Its Head? Seema Amble

- Investing in Tessera Labs Seema Amble, Eric Zhou, and Joe Schmidt

- Why the World Still Runs on SAP Eric Zhou and Seema Amble

WhatsApp Pay's short-lived launch

WhatsApp, the largest messaging app in the world, launched WhatsApp payments in Brazil last week, allowing users to make payments and send money to one another for free. WhatsApp used Cielo as its payment processor and was accepting cards from Banco do Brasil, Nubank, and Sicredi. For anyone who has been following WhatsApp’s drawn-out foray into payments, the news was long overdue. Though the company originally planned to introduce payments in India in 2018, it has yet to receive regulatory approval and integrate with UPI, the Indian central bank’s real-time payment system.

Thus, Brazil was the first country to roll-out WhatsApp payments nationwide — until Brazil’s central bank suspended the service one week later, pending further review. In fact, the central bank even requested that Visa and Mastercard stop enabling WhatsApp transfers, threatening potential sanctions should they refuse to comply. This unexpected reversal seems to be driven by the central bank’s continued push for a competitive environment in the payments space. Cielo’s deep penetration and WhatsApp’s large user base in Brazil has effectively raised red flags as to how future entrants and incumbents will be able to compete.

Assuming WhatsApp does eventually receive approval, Brazil is an excellent location to introduce payment functionality, given the 120 million WhatsApp users there. (The country has the second-largest user base behind India.) Sixty percent of Brazilians own smartphones, and WhatsApp is installed on more than 90 percent of them. WhatsApp is not only Brazilians’ main means of texting, it’s also used by millions of small businesses to showcase their storefronts and inventory. In a country where COVID-19 has increased ecommerce sales by approximately 99 percent month-over-month — an all time high — WhatsApp Pay could further bolster digital transactions and allow merchants to seamlessly accept payments.

The big picture behind Hertz's stock snafu

Bored retail traders equipped with smartphones and zero-cost trades did something that never could have happened a few years ago — they nearly bailed out a bankrupt company. Over 150,000 Robinhood users established positions in the bankrupt car rental company Hertz, outgunning hedge funds and institutional investors. Arguably, Hertz should be worth negative $1.8 billion (according to analysis done by Matt Levine); instead, due to the retail demand, it’s trading at $200 million market cap. As a result, Hertz contemplated a $500 million equity issuance, instead of the Debtor-in-Possession (DIP) financing that typically accompanies Chapter 11. (The offering was suspended, following pushback from the SEC.) The brief saga was a bit absurd, but that absurdity is illustrative of a broader and more meaningful trend: technology in finance is reducing friction and driving marginal costs towards zero. This has surprising and unexpected implications for financial services writ large.

One effect is that power in financial markets is shifting away from large established institutions, like big banks and hedge funds, and back to consumers. That retail traders were able to successfully outgun hedge funds is just one example; others are more profound. By unlocking lower marginal costs, software is shifting business models — and upending entire industries in the process. As Robinhood scaled this year, we watched other big players also start offering free trades, effectively ending the use of daily-active-revenue trades (DART) as a key metric for brokerages.

Beyond trading, fintech is spurring new business models that disrupt the status quo. Companies are now offering free or low-cost services that allow them to take on big banks and corporates. Tally automates the payment of credit card debt. Services like Albert and TrueBill help consumers negotiate lower bills from all manner of companies, especially banks, telcos, and internet providers. DoNotPay goes a step further, enabling customers to go so far as sue companies for violation of consumer rights.

Financial services used to be about fee extraction; now fintechs are returning those fees to consumers. That’s not only changing existing industries, it’s fueling the creation of entirely new categories of financial services.

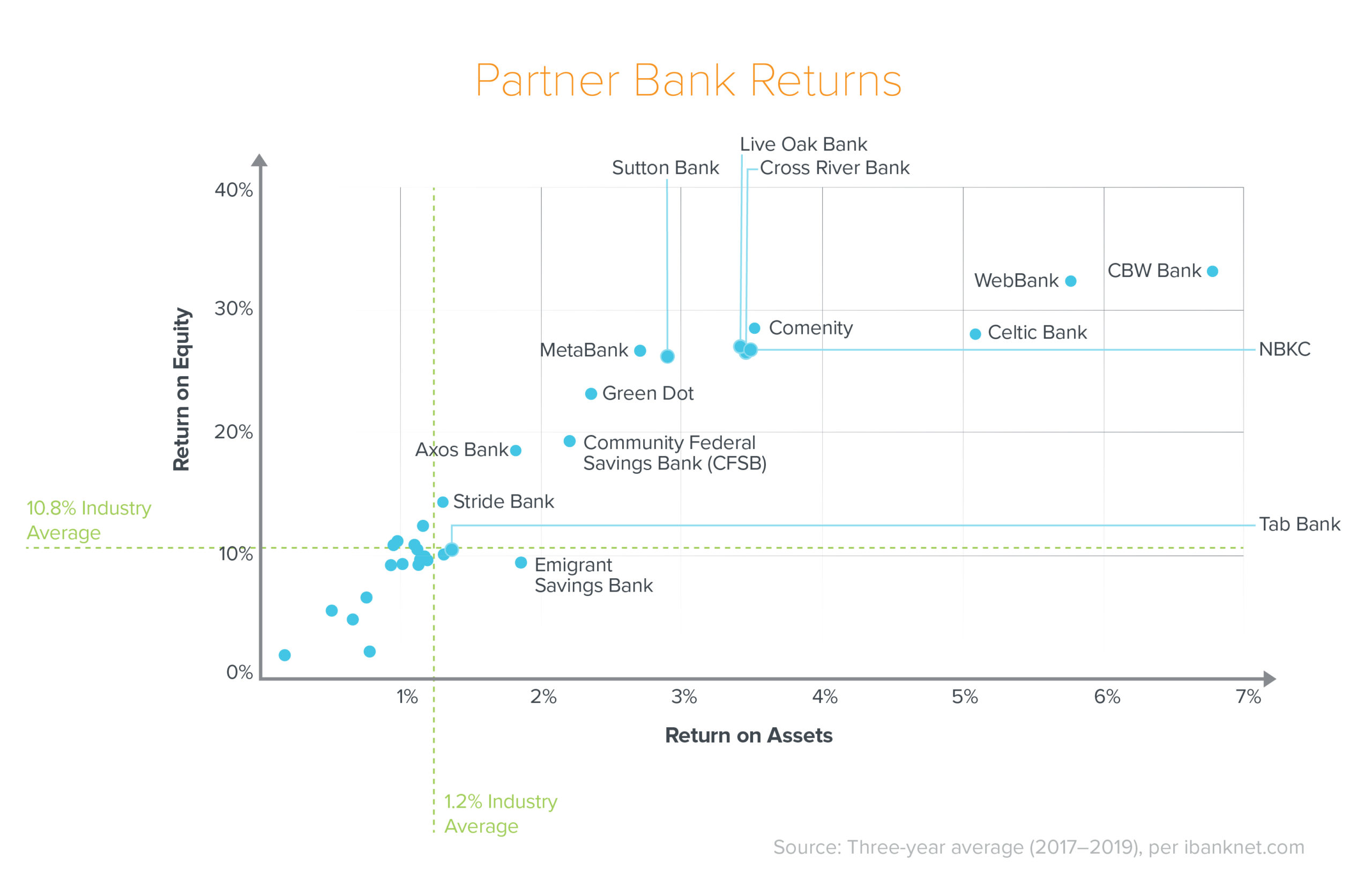

The partner bank boom

Anish AcharyaPartner banks have exploded in recent years — by our count, their ranks have grown more than five times over the past decade. Today, there are more than 30 partner banks representing hundreds of fintech relationships and financial services.

The rapid rise of this trend begs the question: Why has the number of partner banks increased so suddenly? For one, the relationship is mutually beneficial. Fintech companies are able to offer banking products without the regulatory overhead of becoming a bank, while banks harness these partnerships to improve their returns by gathering low-cost deposits or growing asset-light fee streams.

Charts provided herein are for informational purposes only and should not be relied upon when making any investment decision.

In addition, it has become increasingly easy to form these partnerships. Eliciting a partner bank used to require a herculean effort, due to both compliance concerns and technical hurdles. Now, thanks to the rise of companies that provide banking infrastructure as a service, fintech companies can launch products in a matter of months, not years.

In an effort to provide greater visibility into this interconnected and expanding ecosystem, we’ve mapped out the banks, the fintech companies, and the many services these partnerships afford. To view and download the extended list of more than 30 partner banks and fintech partners, including the products they offer, subscribe to our fintech newsletter.

- The Most Human Technology Ever Made Anish Acharya

- What Happens to Design After AI? John Maeda, Paul Bakaus, and Anish Acharya

- What’s Next for Consumer AI? | Josh Elman Joins a16z Josh Elman and Anish Acharya

- Building AI Agents for Enterprise Operations Pablo Palafox, Luis Paarup, Anish Acharya, and Olivia Moore

- Investing in Ethos Anish Acharya, James da Costa, and Olivia Moore

More from the a16z fintech team

Cabin-Fever Trading; Housing Projections; COVID Drives Digitization, and More

Online brokerages compete for new millennial investors, financial services go digital, and the post-pandemic outlook for banks.

By the a16z fintech team

35 Fintech Companies Aiding in Coronavirus Relief

From Propel’s part in Project 100 to Square’s role as a stimulus lender, here’s how U.S. fintech companies are stepping up to help those feeling the impact of COVID-19.

By Seema Amble and the a16z fintech team

The CFO in Crisis Mode: Modern Times Call for New Tools

Many businesses are reassessing their 2020 projections as the pandemic unfolds. Yet despite an influx of data on which to base decisions, the tools at the CFO’s disposal have not kept pace.

By Seema Amble and Angela Strange

Small Businesses Depend on the Stimulus Package. The Stimulus Will Depend on Fintech.

The government is unprepared to identify, adjudicate, and disburse $350 billion of aid to small businesses without a sea of fraud. Tech is the answer.

By Alex Rampell

Sign up here to receive this monthly update from the a16z fintech team in your inbox.