This first appeared in the monthly a16z fintech newsletter. Subscribe to stay on top of the latest fintech news.

IN THIS EDITION

- A different path to self-driving money

- Online brokerages compete for new millennial investors

- The pandemic’s impact on the housing market

- COVID drives digital acceleration in finance

- The post-pandemic outlook for banks

Want more a16z?

Sign up to get our best articles, latest podcasts, and news on our investments emailed to you.

Thanks for signing up.

Decentralizing self-driving money

Anish AcharyaThere are two product experiments currently playing out in consumer fintech: the pursuit of “self-driving money” (first coined by Wealthfront)—software that automates and optimizes your finances, across categories—and a system that connects multiple point solutions (your credit, savings, student debt, mortgage, etc.) in such a way that the sum is greater than the parts. In the past, I’ve referred to this concept as having a “money button” on your phone. Many, myself included, assumed that self-driving money would ultimately be achieved by a single, dominant app. Now, due to new advances in fintech infrastructure and APIs, another path has emerged.

The idea behind the money button is that a single company will find product market fit with a specific wedge—such as managing credit debt or financing a home—and will then cross-sell into a constellation of other financial products, eventually achieving 100 percent of its customers’ wallet share. Conceptually, it’s similar to the iOS/Android divide in the mobile universe: There may be competing constellations of financial tools, but once you choose a core product, you’re incentivized to use the other products in that particular company’s ecosystem. This vision is strategic, exciting, and so far unrealized—no fintech product has achieved meaningful scale with a second line of business, much less many lines of business.

The decentralized alternative is decidedly less elegant: consumers choose solutions from many different providers to fit their various financial needs. In this model, your credit card, mortgage, savings account, and wealth management are all powered by different startups, and all of these app icons will (grudgingly) co-exist in a folder on your phone. Does this decentralized solution mean we’ll fall short in our ultimate quest for self-driving money? Not necessarily. But it does suggest that we’ll need new infrastructure to support this model.

That’s exactly the trend we’re currently seeing in the fintech infrastructure and API space. Platforms are becoming less prescriptive and more customizable to the user’s needs. Startups at the vanguard of this shift—Atomic, Astra, and Canopy among them—are powering connectivity across fintech apps in pursuit of self-driving money. By integrating with payroll providers, for example, Atomic automates the ability to easily switch your direct deposit to a newly opened bank account. Astra allows users to create rules that automate and optimize their money movement—say, sweeping excess cash into a higher-yield savings account.

With fintech products gaining increasing advantage over traditional banks, aided by a more open underlying infrastructure, the emergent model for financial automation may end up being decentralized—the money folder, rather than the money button.

- The Most Human Technology Ever Made Anish Acharya

- What Happens to Design After AI? John Maeda, Paul Bakaus, and Anish Acharya

- What’s Next for Consumer AI? | Josh Elman Joins a16z Josh Elman and Anish Acharya

- Building AI Agents for Enterprise Operations Pablo Palafox, Luis Paarup, Anish Acharya, and Olivia Moore

- Investing in Ethos Anish Acharya, James da Costa, and Olivia Moore

Online brokerages compete for new millennial investors

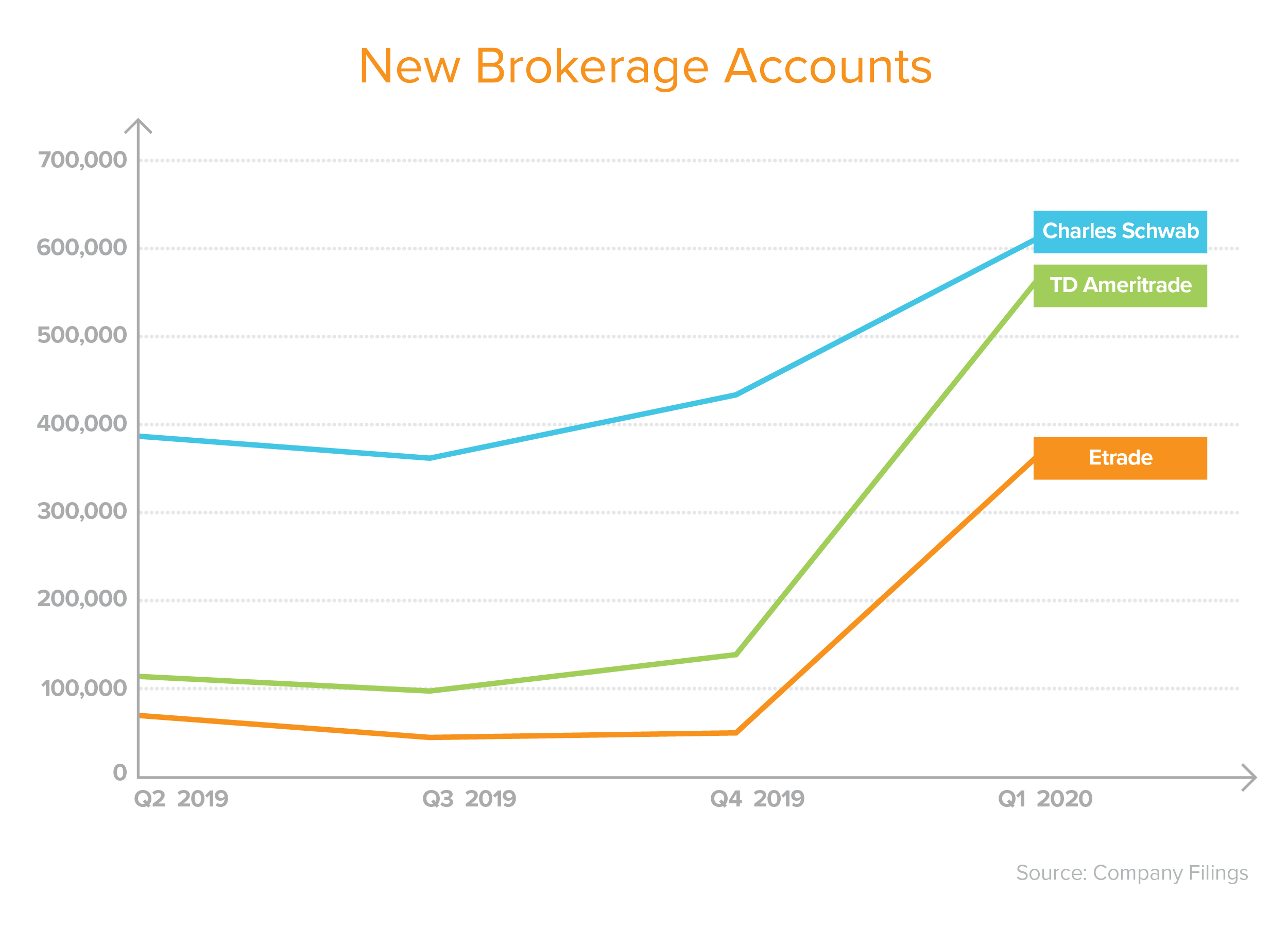

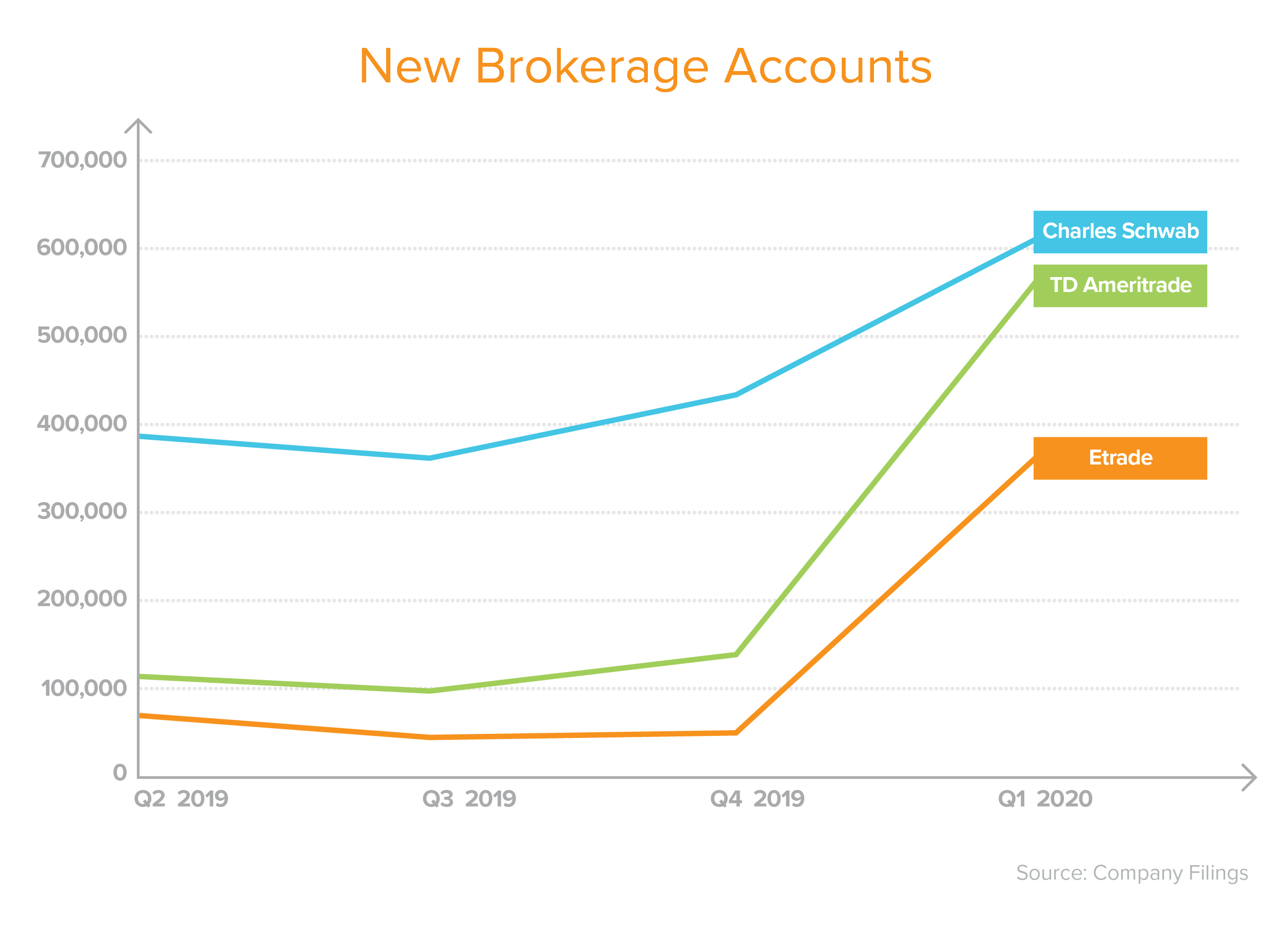

Seema AmbleOver the past few months, the major brokerage platforms have seen significant growth in both trading volume and new account creation. What’s causing this spike? And is it cabin-fever trading or a long-lasting trend?

Charts provided herein are for informational purposes only and should not be relied upon when making any investment decision.

Charts provided herein are for informational purposes only and should not be relied upon when making any investment decision.

It’s true that market uncertainty typically leads to sell-offs in the public markets, as well as a rise in trading volume—but that doesn’t explain the explosion in new accounts. There are a couple of factors at play here: first, in Q4 last year, the major trading platforms launched commission-free trades, which boosted new account growth. And now, as people shelter in place, the coronavirus seems to have prompted another spike in investment accounts. Of Charles Schwab’s 609,000 new accounts in Q1 2020, more than 280,000 of those were added in March alone.

This new account growth highlights the ongoing battle to win over millennial and Gen Z investors. Brokerage firms report that many of these new accounts are young and first-time traders. That’s surprising, given that millennials reportedly trust financial institutions less, invest less, and have far less saved for retirement than previous generations. Of course, a number of new trading platforms have also cropped up over the past 5 to 10 years—including Robinhood, Stash, and others—that appeal to millennials and Gen-Zers with commission-free, mobile-first, easy to use products. Robinhood has added 3 million funded accounts this year alone. Older brokerages are feeling the threat and want to compete for these customers.

To that end, Charles Schwab announced fractional share ownership earlier this month, which allows users to own a percentage of share, rather than buying the entire share. This makes investing more affordable and accessible. Likewise, Fidelity announced real-time fractional trades in stocks and ETFs in January, on the heels of similar product announcements by Robinhood and Cash App. Meanwhile, platforms like Betterment and Stash have offered fractional shares for years.

While incumbents have followed the trend to offer free trades and fractional shares, they’ve innovated less on product and marketing than newer fintech companies. As an example, Stash has been hosting “Stock Parties”: open, social media-driven parties that give people the chance to earn stock in their Stash investment accounts at 4pm every weekday. Stash also pioneered a “stock back reward,” which awards users fractional shares for their spending.

It remains to be seen how much this new trading activity will persist, post-COVID. In the meantime, the crisis continues to drive competition between incumbents and fintech companies—and in the short-term, at least, that has allowed more consumers to access the public markets.

- Is Software Losing Its Head? Seema Amble, Elena Burger, and Steven Sinofsky

- Investing in Probook Alex Rampell, David Haber, Olivia Moore, and Seema Amble

- Is Software Losing Its Head? Seema Amble

- Investing in Tessera Labs Seema Amble, Eric Zhou, and Joe Schmidt

- Why the World Still Runs on SAP Eric Zhou and Seema Amble

The pandemic's impact on the housing market

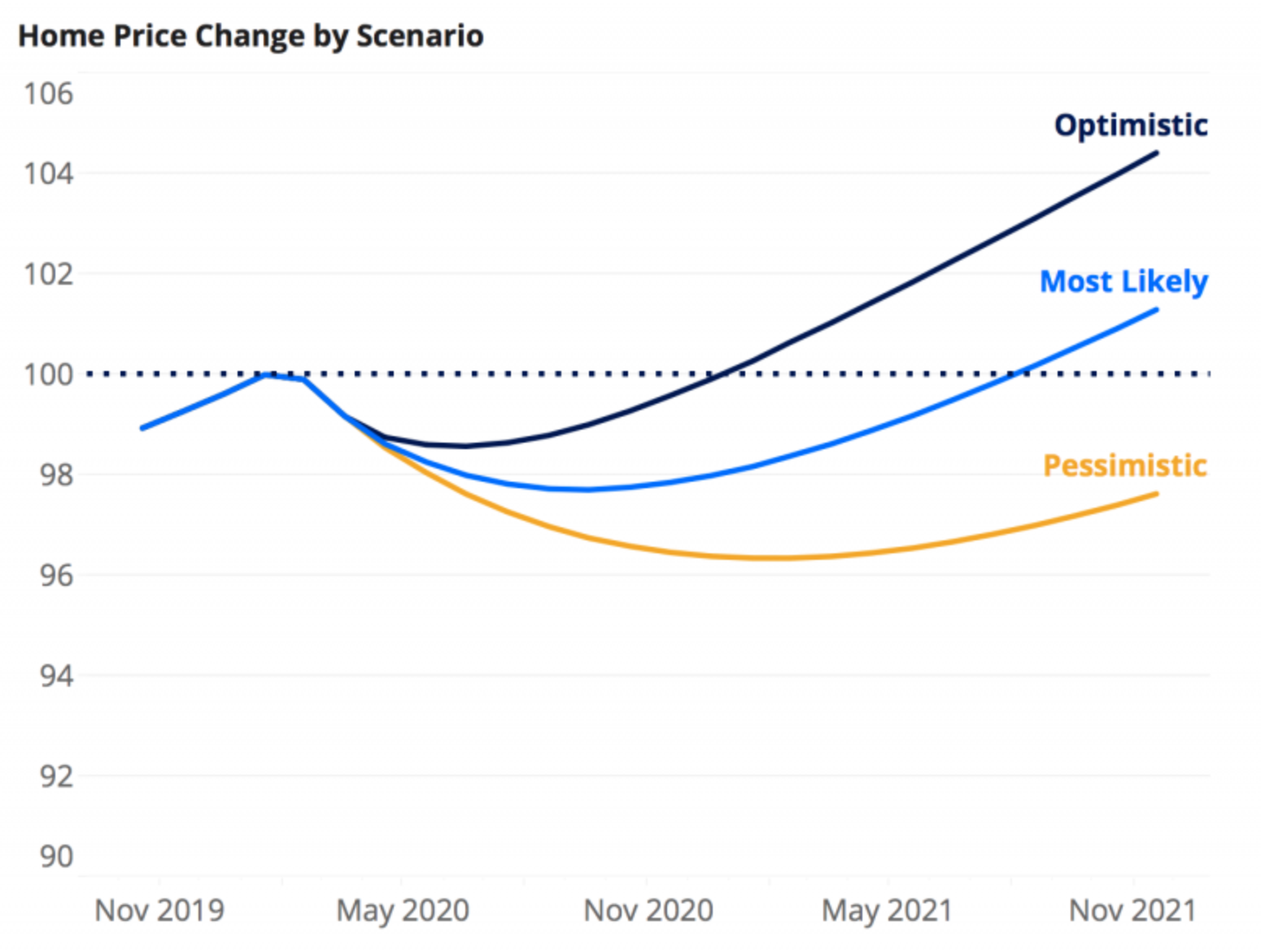

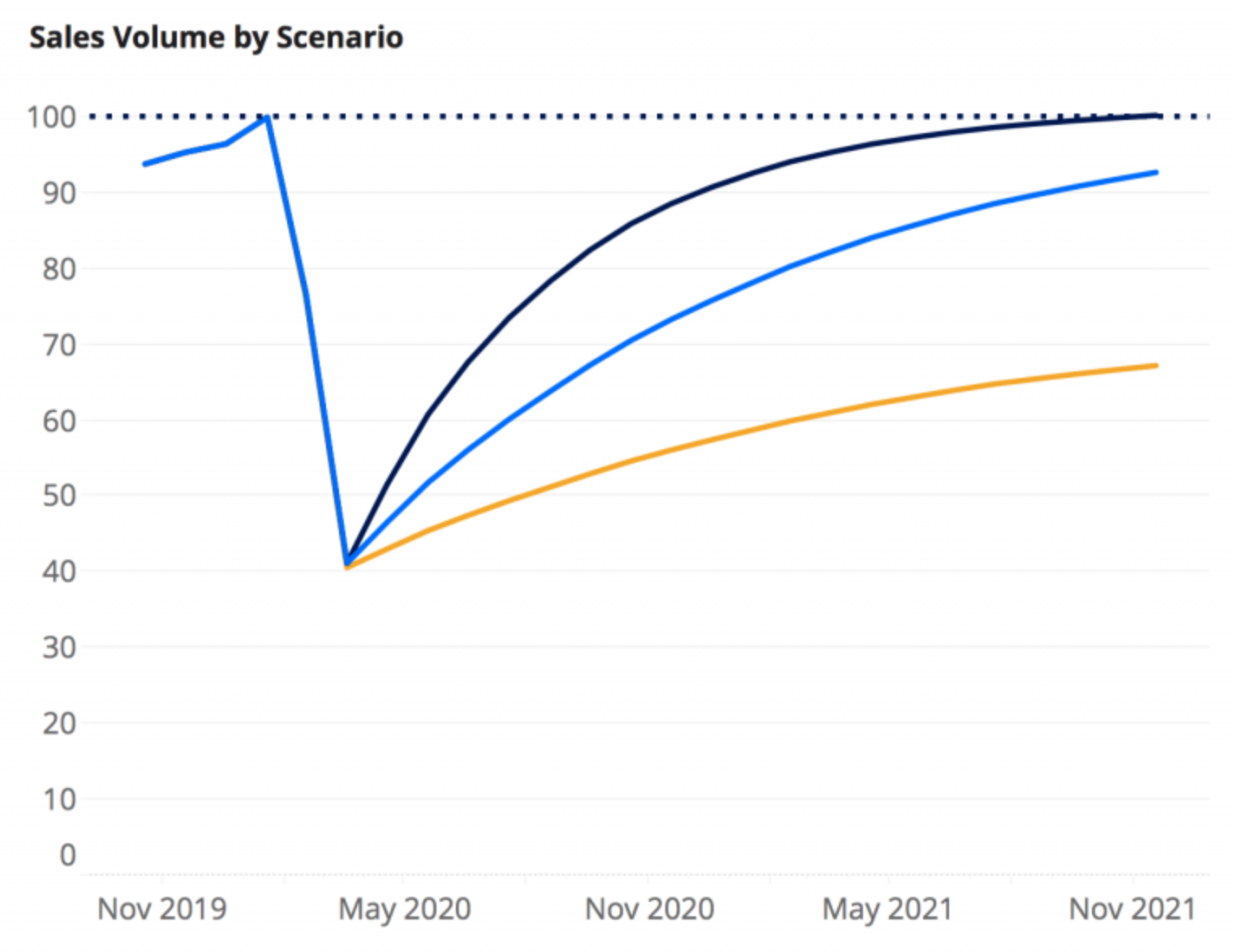

The real estate marketplace Zillow released a new forecast for the housing market this month. Unsurprisingly, perhaps, the report predicts a 2 to 3 percent reduction in home prices this year and a 45 percent drop in the volume of home sales. Interestingly, however, the company also estimates that home prices will rebound to pre-COVID rates by late 2021 and that the sales volume will spring back by 2022.

Source: Zillow

Source: Zillow

In a historical context, a one to two year recovery seems optimistic. During the 2008 crisis, by comparison, home prices dropped by more than 20 percent and didn’t fully recover until 2016. Of course, the ‘08 crisis was largely tied to the housing bubble, as well as a sharp increase in the supply of homes in the preceding years. Still, unlike 2008, our current crisis has left more than 30 million people unemployed and halted economic activity. So what’s behind Zillow’s comparatively positive prediction?

The company’s view may be partially tied to the role that technology plays in the real estate process today. It’s now possible to view homes virtually and complete much of the closing process online (more on that below). Zillow, for example, created 525 percent more 3D home tours in April than in February; the company expects virtual tours to continue to increase in popularity even after the pandemic subsides. In addition, the recent rise in iBuyers—companies that use tech and AI to make instant cash offers on homes, such as Opendoor, Zillow Offers, and RedfinNow—has accelerated the influx of technology into real estate and the relative ease with which we’re able to buy and sell homes. Whereas housing was subject to destructive market forces in 2008, tech advances in the ensuing years may help curb the slump in sales and prices this time around.

COVID-19 drives digital acceleration in finance

Businesses of all kinds are experiencing two years’ worth of digitization compressed into months. That’s evident in healthcare, education, and, yes, financial services. All of these industries have historically been slow to adopt new technology, due to the complexity of the systems involved and regulatory oversight. Now the forcing function of social distancing is overcoming that inertia. We’re already beginning to see meaningful ways in which that is taking place.

Banking moves online

At Square, direct deposit volumes grew by three times from March to April, up to $1.3 billion; Chime saw record signups. And traditional banks and credit unions witnessed a 50 percent increase in mobile banking engagement since the beginning of the year. Meanwhile, Visa noted an 18 percent rise in US digital commerce. And PayPal had its largest single day of transactions on May 1, besting previous Black Friday and Cyber Monday records.

In China, Ant Financial has seen demand increase 400 percent on its online banking platform from lenders looking to develop online offerings. That’s forecasted to generate 65 percent of Ant’s revenue by 2021.

Notarization goes remote

Likewise, remote online notarization (RON) is on the rise: 47 states have permanent or temporary online notarization measures in place, up from 24 states with permanent measures preceding the epidemic. These nuances are complex; specific requirements vary by state, sometimes even by county. In response to the increased demand, Notorize.com announced it is hiring 1,000 notaries.

Bank branches close, online accounts open

Twelve percent of bank branches closed between 2010 and 2019 in the US. That number is likely to rise over the coming year as social distancing persists. Meanwhile, online account opening is way up—for most, it’s the only reasonable means available to open an account. Though the permanent closure of bank branches has not yet been announced in the US, 800 branches have shuttered in China.

Home buying and selling go digital

Most mortgage brokers are understaffed for the recent surge in refinance volumes. As a result, digitally native mortgage operations have picked up some of the slack. (Better.com, one example, is hiring 1,000 new employees). A sticking point in the mortgage process—especially with social distancing in place—is the appraisal. Appraisal waivers increased from 10 percent of loans to an estimated 30 percent since the coronavirus hit the US, mostly for loans with a loan-to-value ratio below 70 percent. Wells Fargo has stopped ordering interior appraisals for everything except new construction.

Even governments are getting on the bandwagon: Twenty percent of municipalities have introduced virtual tour technology for property inspections for their permitting offices, up from 4 percent pre-pandemic.

Remittances move to digital rails

New active users for the electronic money transfer service Xoom quintupled since January. In April, 28 percent of all of MoneyGram’s transfers were digital, compared to 18 percent for the months prior. Remittances account for 10 percent of GDP globally and 30 percent in some of the poorest countries.

In the long run, digital delivery brings the promise of better, more convenient service at lower cost.

The post-pandemic outlook for banks

Kristine LipscombClearly, we’re currently in a period of tremendous change—what does the digital acceleration of financial services mean for the future of banks? The age-old question of “build vs. buy” may be a thing of the past. In the current climate, it’s becoming increasingly apparent that in order to adapt quickly, institutions will be compelled to prioritize fintech partnerships.

At present, most banks are reacting to pressure to be virtual and digital—simultaneously shifting more than 90 percent of their employees to work virtually while operating on legacy, on-prem core banking systems that have not yet migrated into the cloud. JP Morgan Chase is currently assessing how many of its 180,000 employees who are currently working from home will return to a physical workplace. As bank services become increasingly digital, the viability of the traditional bank branch model will be called into question.

Compounding the pressure on banks, fintech companies were already challenging existing business models and acquiring new users well before the pandemic hit. Now a focus on automation, machine learning, and analytics will be more important than ever. This data-driven, customer-centric shift will define the future of financial services.

The 2008 financial crisis cemented the notion that brand and reputation are critically important to maintain existing customers and acquire new ones. It’s not enough to be reactive; the current moment will challenge banks to be proactive by investing in customer-first products and services. The most effective way to do so—and to best manage this rapid digital transformation—may be to partner with fintech.

More from the a16z fintech team

Investing in Deel

Remote work is becoming increasingly common, but the tools that enable employers to pay a global workforce have not kept up. That’s why we’re partnering with Deel as they build a payroll solution for remote workers.

By Anish Acharya

How to distribute cash to 200M Americans; the calculus behind pandemic insurance; and more

The a16z fintech team on direct cash transfers, the finance apps seeing an uptick, and the challenges of extending insurance coverage for coronavirus.

By the a16z fintech team

35 Fintech Companies Aiding in Coronavirus Relief

From Propel’s part in Project 100 to Square’s role as a stimulus lender, here’s how US fintech companies are stepping up to help those feeling the impact of COVID-19.

By Seema Amble and the a16z fintech team

The CFO in Crisis Mode: Modern Times Call for New Tools

Many businesses are reassessing their 2020 projections as the pandemic unfolds. Yet despite an influx of data on which to base decisions, the tools at the CFO’s disposal have not kept pace.

By Seema Amble and Angela Strange

Small Businesses Depend on the Stimulus Package. The Stimulus Will Depend on Fintech.

The government is unprepared to identify, adjudicate, and disburse $350 billion of aid to small businesses without a sea of fraud. Tech is the answer.

By Alex Rampell

Sign up here to receive this monthly update from the a16z fintech team in your inbox.