Everyone is talking about outcome-based pricing in AI apps. But almost no one is talking about what is actually happening behind closed doors: price wars.

Pricing wars are terrifying for companies of all sizes, but especially for startups. A great team, with the right product, at the right time, can still die from pricing their product incorrectly. And everyone knows that the hard part about pricing products is resisting the pressure to underprice, in order to win competitive deals.

Every AI company knows this struggle. New entrants flood the market weekly, burning investor capital to buy distribution at low cost due to falling (and subsidized) cost of tokens. Incumbents feel compelled to respond. “Match all competitors” has quietly become a standard entry in many AI sales playbooks. And once retaliation begins, price cuts cascade — great for buyers who are aware and taking advantage, but brutal for the businesses competing for them. As an AI app startup today, facing feature-similar and well-funded competitors, how do you not die by price war?

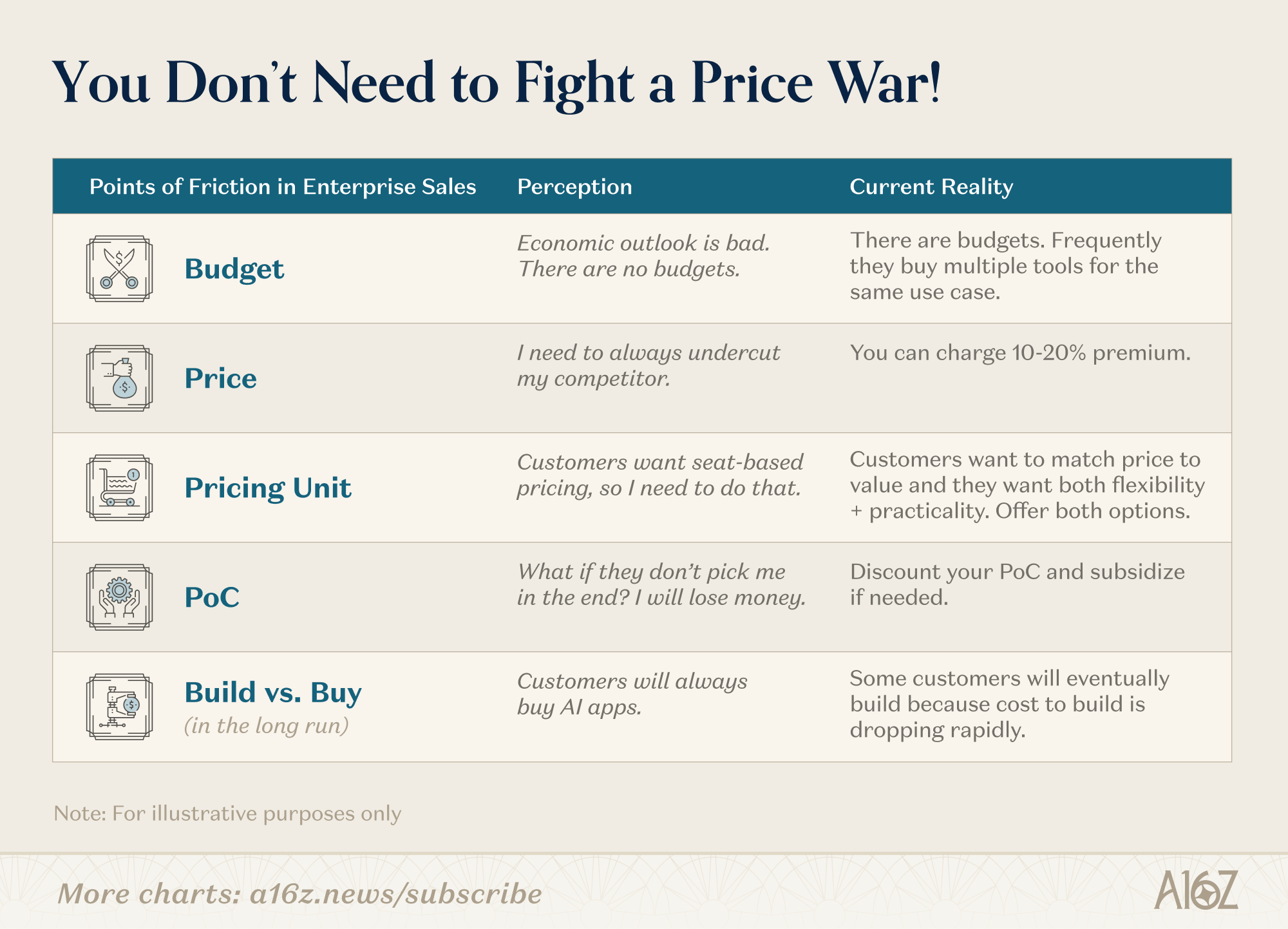

In speaking with many of the large buyers of these AI services (I can’t say who they are, but they’re big, obvious brands you know), it’s actually pretty clear that competing on price isn’t so necessary:

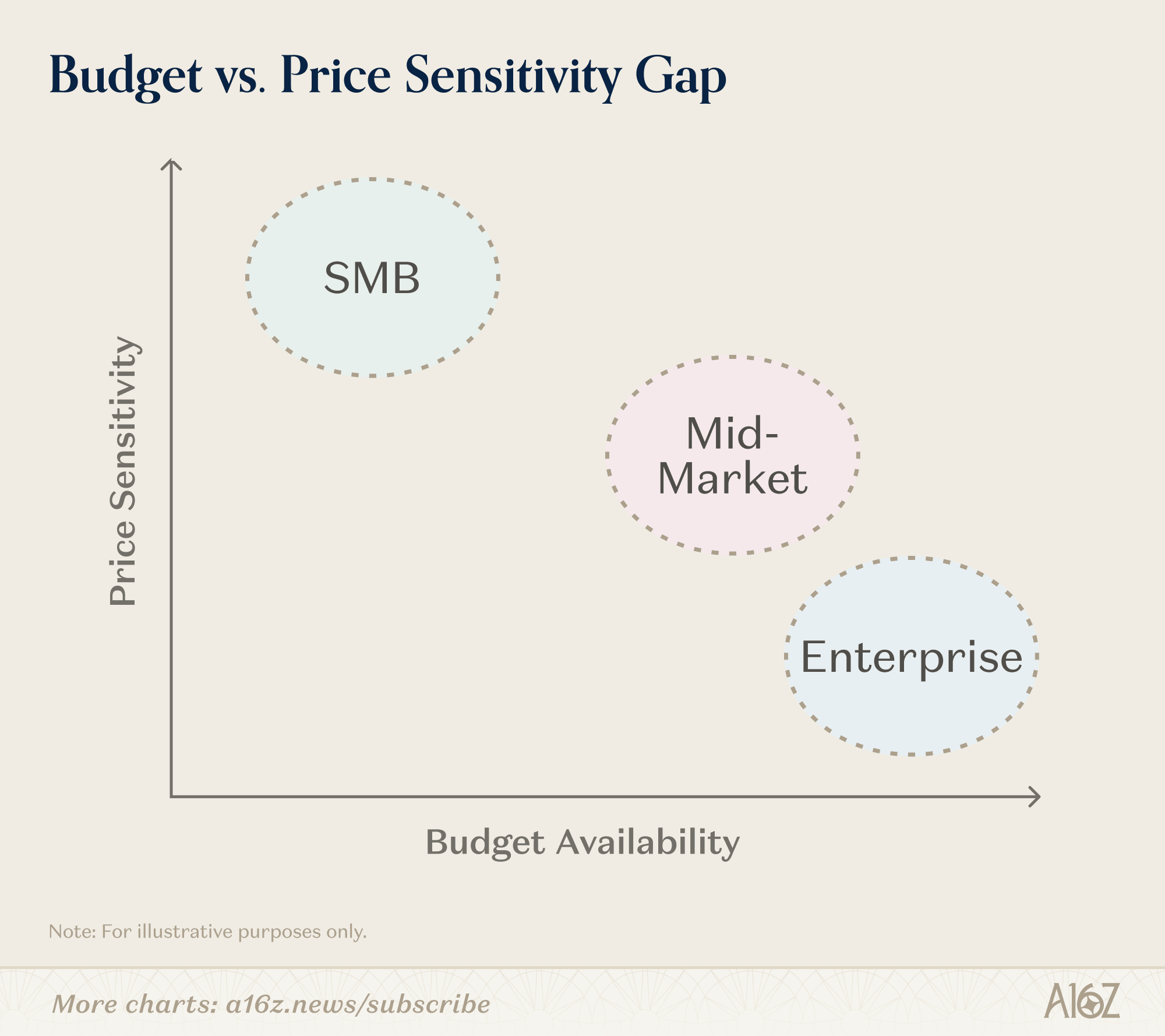

- These brands have huge budgets to spend, to the extent that they regularly hire multiple AI products for the same job.

- Even if you and your competitor are similar, the solution you offer is very different from the customer’s status quo. Price according to the value you provide, and then make sure you’re the product they actually want.

- Everyone can sense that “category leaders” constantly change, so everyone worries about pricing as the premium option. But these brands have no problem paying a premium, if you give them the flexibility and the predictability in how they pay for it (in addition to the premium solution). Most startups underestimate this.

There is no silver bullet for pricing wars; there never has been. But, for AI application companies anyway (this piece isn’t for model providers; that’s a whole different story), if these enterprise buyers are any indicator, you don’t have to give it all away. Here’s what we learned:

1. The budgets are there. Stop acting like they aren’t.

The most dangerous assumption in a price war is that customers are fighting you on price because they don’t have the money. In enterprise AI right now, that is often simply not true. Leaders understand the magnitude of the opportunity. AI has the potential to reduce costs more dramatically than anything before it—and the risk of moving too slowly is existential. As a result, many large enterprises already have meaningful, pre-allocated AI budgets, and they are actively deploying them. The money is there: it’s just a matter of earning it.

In a recent conversation with the Head of AI at a top financial institution, one insight stood out: They intentionally deploy two or three AI tools for the same use case. Not because of indecision—but by design. Redundancy is policy. They do not want to rely on a single vendor for any critical workflows. AI apps are still maturing. Performance can fluctuate. Hallucinations happen. Outages are possible. So they hedge.

They also recognize that each vendor has distinct strengths. Instead of forcing a single solution across the organization, they match tools to different personas and use cases—for example, deploying multiple coding tools tailored to different teams.

Our conversations with mid-market and smaller enterprise companies reveal a different dynamic: they move faster. Teams run parallel demos, and once something shows promise, they quickly move into a proof of concept. One leader at a B2C hardware company described walking away from a low-cost contract with an incumbent technology giant in favor of a smaller, AI-native provider—simply because it delivered the most advanced agent. Across both segments, the pattern is consistent. The winning tool is rarely the cheapest. It is the one that proves indispensable. Which means the real question is not “can we afford this?”—it is “which of the tools we are piloting do we standardize on?”

The implication is significant: if you are discounting defensively against a cheaper competitor, you may be giving away margin you never needed to give. The buyer you’re worried about losing may have already preferred you because you are better or already have a budget for both of you.

What wins in that environment isn’t the lowest price — it’s becoming the tool they can’t imagine removing. Reliability, security posture, onboarding quality, and — more than anything else — whether you are visibly listening and building: these are the factors that determine which tool survives the consolidation phase.

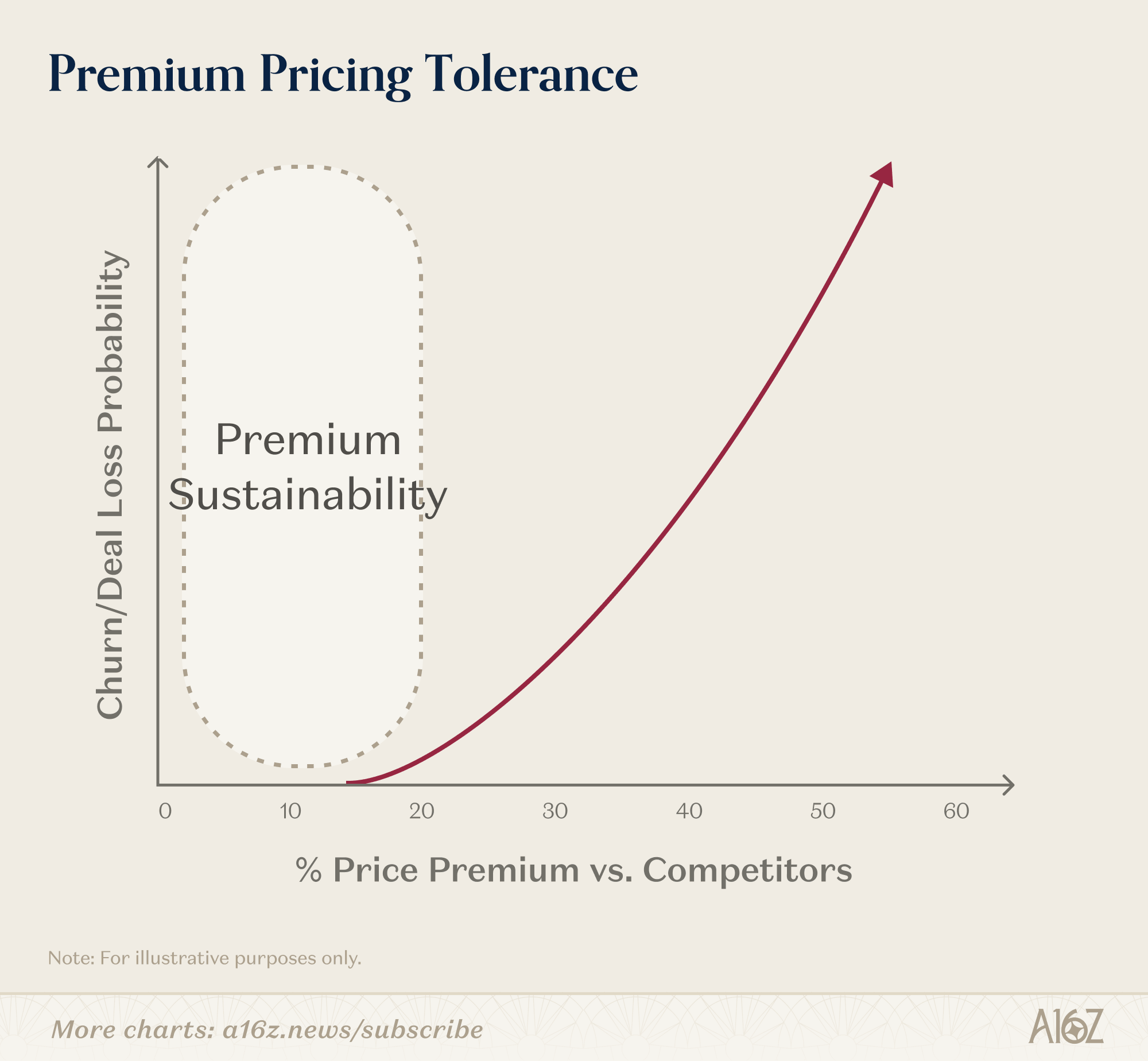

2. Premium perception is real — but it’s fragile.

Not every AI app company needs to match competitor prices. If your product is genuinely premium — or is perceived as such — you likely have more pricing room than you think. A useful rule of thumb: a strong premium perception can sustain prices 10 to 20 percent above direct competitors without materially increasing churn or creating friction in the purchasing process.

There is even a more surprising way enterprises tolerate price gaps. A VP at an on-demand logistics platform we spoke with found one agentic AI app to be clearly superior to another (to my surprise, the underperforming cheaper one is seen as the market leader) and the superior one is significantly more expensive, yet he still chose to deploy both, despite the price gap. His reasoning was simple: allocate intelligently. Use the premium tool where performance matters most, and rely on the lower-cost option for simpler tasks. The result is not necessarily higher spend, but a more efficient one—better outcomes without materially increasing the budget.

But that premium is not a fixed asset. In a market moving this fast, perception can erode quickly — a new entrant with a cleaner UI, a better benchmark, or a louder content presence can shift buyer expectations within a quarter. The companies that hold premium positioning do so actively, not passively. They monitor the signals: sales cycle length, win/loss rates on competitive deals, the language prospects use when they push back on price. When those signals shift, your window to respond is short.

That being said, the fact that “market leadership” is so fleeting for AI companies is something everyone already knows, and for that matter, probably overestimates. The proof is in the price wars! The key to avoiding price wars entirely (and protecting your business) is finding another way for your customers to recognize and pay for value. This is where creativity matters, far more than most startups realize.

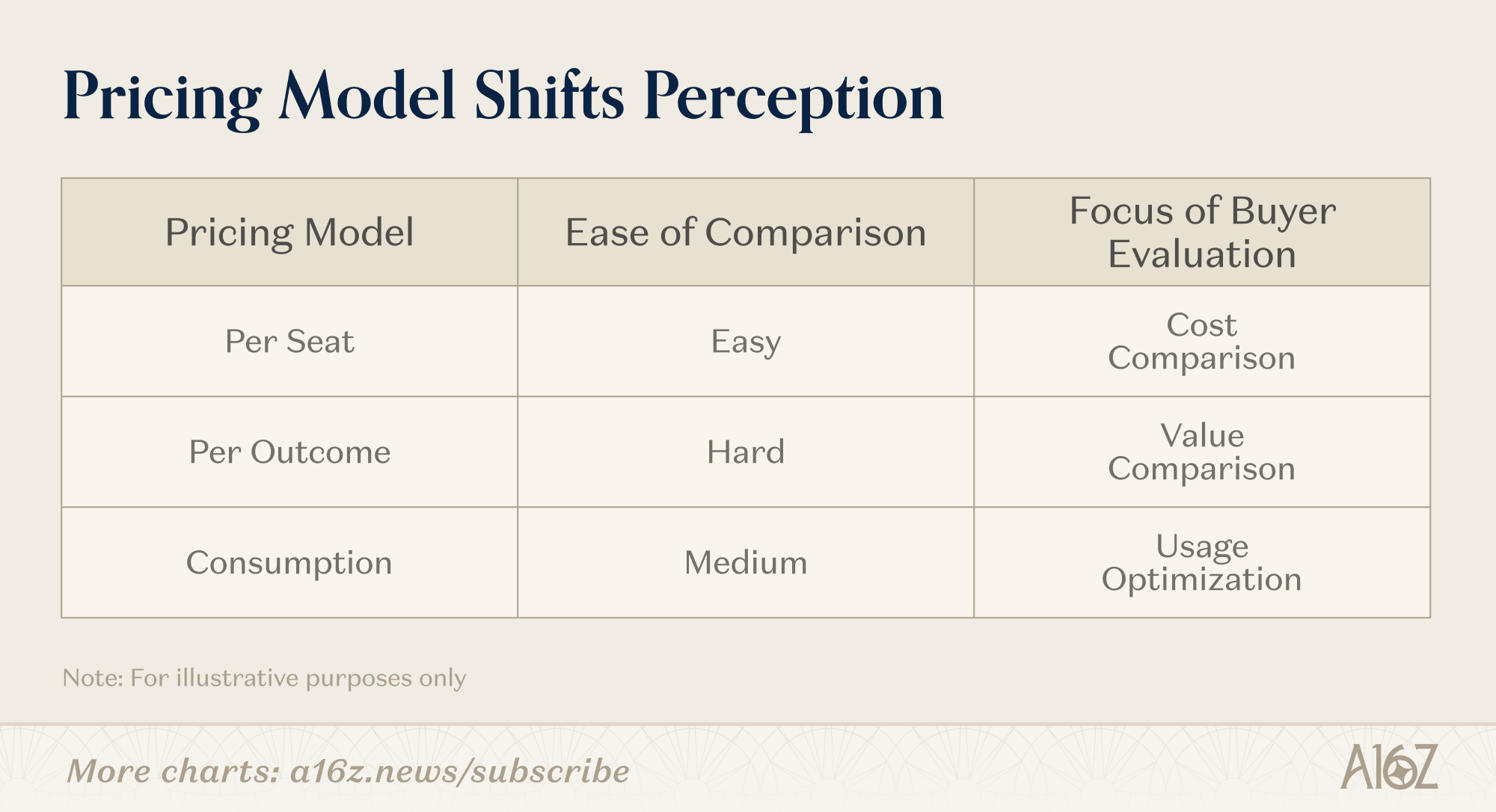

3. Pricing units and structures are more important than you think.

The most underused lever in AI apps pricing isn’t the number — it’s the unit. How you charge is as much a competitive lever as what you charge. AI app companies are experimenting with per-seat, per-outcome, per-workflow, and consumption-based models. Each unit frames value differently. A per-outcome model, for example, makes price comparisons much harder. You’re no longer being compared on cost per seat but on cost per result. That shift changes the conversation.

Across all of our conversations, one theme came up consistently: pricing has to match value. Even very large enterprises are pushing for outcome-based models—gainshare, success-based pricing, or other structures that tie spend directly to results. There is a clear desire to move away from traditional usage-based or seat-based models, which many feel are misaligned with how AI actually delivers impact.

At the same time, there is an apparent tension. While buyers want vendors to have meaningful skin in the game, they also need predictability. Budgets still matter. Planning cycles still exist. Fully variable pricing, in practice, can be difficult to operationalize.

A VP of AI adoption at a large real estate company put it most directly: vendors should offer dual models, allowing customers to decide between predictability and performance-based upside. In other words, give buyers the ability to trade off flexibility for certainty depending on their internal constraints. In a market where everyone is competing on price, letting buyers choose their own model may be the edge that has nothing to do with price at all.

4. Don’t discount the product. Discount the proof of concept.

One of the most utilized moves in AI competitive selling is also one of the simplest: lower the cost and friction of entry, not the cost of the product itself.

Enterprise buyers in AI are often in long, cautious evaluation cycles. Procurement timelines are slow. Security reviews take months. One enterprise buyer at a large bank said that their POC of an AI app took almost a year. The decision to standardize on a tool is significant — and risky. What stops deals from progressing is often not price objection on the full contract; it’s the cost and commitment of getting started.

The move is to make the proof of concept (POC) more accessible. Faster to initiate. Cheaper to run. Lower in upfront scoping. Then convert at a fair pricing once you have won the evaluation. A B2C company that purchased an AI app after POC said that they had a flat price for unlimited usage (albeit limited workflows) during their POC. Once the purchase was made, they started paying for exactly what they used. A VP at a large bank said that their AI app provider gave them credits during POC at a discounted rate, but once they started running into performance issues, the strings of the credit pool loosened as both parties wanted the agents to work.

This is already pretty common. Companies are offering significantly expanded free tiers or over-delivering during POCs — sometimes by an order of magnitude — to get customers onboarded and deeply engaged. In some cases, this can look like 10–25x more value than what is ultimately included in the paid plan.

The goal is not to win on price but to win on adoption: get customers hooked early, before the market consolidates. Elena Verna, Head of Growth at Lovable, puts it plainly: “[The freemium plan] costs us an arm and a leg, but we view it as a marketing expense, not as a cost center.”

5. The real long-term price war isn’t with your competitors. It’s with your customer’s engineering team.

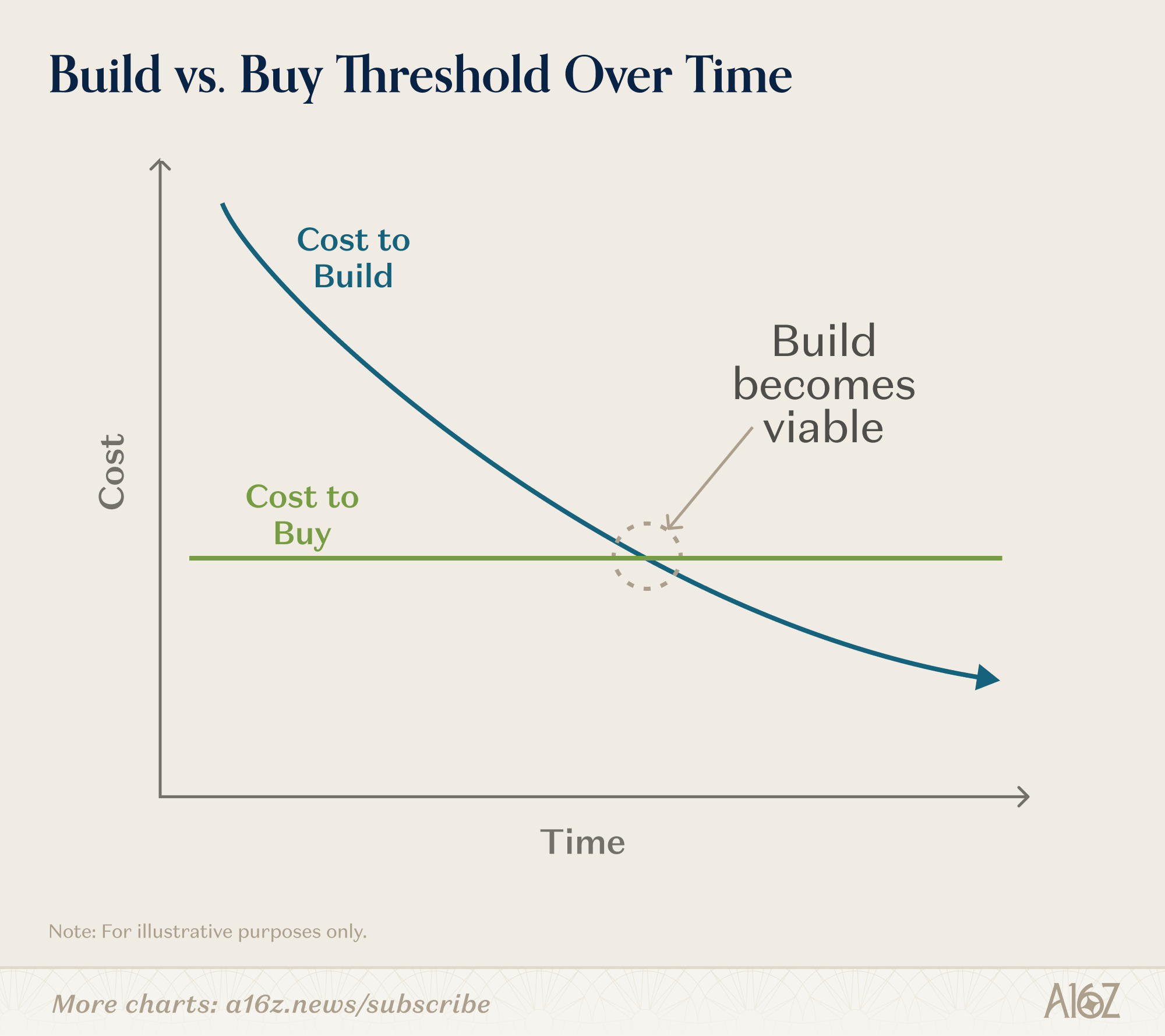

There is a threat to AI app companies that gets far less attention than it deserves: as foundation model costs continue to fall, the build-vs-buy calculus shifts. Companies are a lot more sophisticated than expected on this.

When models are expensive and complex to deploy, the case for buying a purpose-built AI app is straightforward. But as inference costs drop and model APIs become easier to integrate, the internal cost of building a custom solution approaches — and in some cases falls below — the cost of a third-party subscription.

At that point, the conversation changes. Engineering teams start asking whether they can just build it themselves. And in many cases, they can.

Companies we talked to had mixed perspectives on the build vs. buy question. There is, of course, some selection bias—everyone we spoke to had already adopted AI applications in some form. But even within that group, the long-term strategies varied meaningfully.

One B2C logistics company expects to move away from third-party tools over time. Their view is that current costs are unlikely to scale efficiently, and that building in-house will ultimately be more economical.

In contrast, a smaller B2C hardware company reached the opposite conclusion. For them, building is simply not viable. They do not have the engineering capacity to support it, and even a small team would cost more than their current vendor contracts.

Others are taking a more segmented approach. A VP at a financial institution described a clear boundary: anything non-core will be purchased, while anything tied directly to their core product—mortgages and other financial services—will be built in-house, both in the short and long term. VPs and Directors from other industries agreed with this approach.

Taken together, these perspectives highlight that the decision is not binary. It is shaped by economics, internal capabilities, and, most importantly, how close the use case is to the company’s core value proposition.

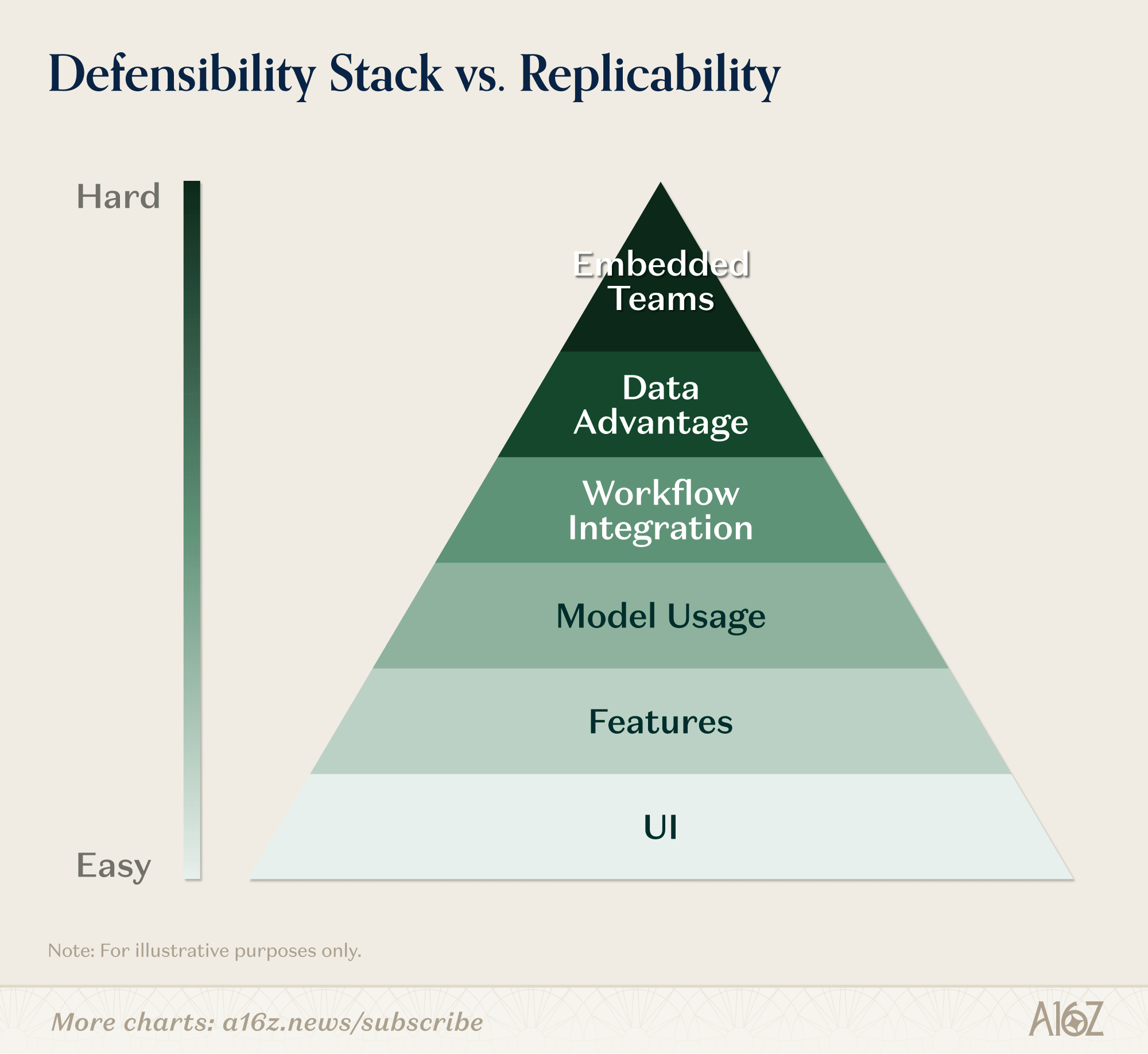

This is the price war that matters most in the long run — and the one that can’t be won by discounting. The defense is differentiation that is genuinely expensive to replicate internally: deep workflow integration, continuous model improvement, domain-specific training data, dedicated customer success, and forward-deployed engineers embedded in the customer’s operations. Scale buys time. That depth is what earns loyalty.

The thread connecting all five

Across every conversation we had — financial institutions, logistics platforms, hardware companies, real-estate, travel platforms, and others — the pattern was the same. Nobody said they chose a tool because it was cheapest. They chose the one that proved indispensable, that listened, that made the evaluation easy and the contract fair.

The price war is real. But it’s mostly being fought on the wrong battlefield. You don’t get to choose when it starts. You do get to choose whether it’s the fight that defines you.

Post script: There is sparse, but some literature on pricing wars which do not provide any silver bullets. If you want, ChatGPT can give you all the advice that has been given. Here’s the prompt:

“Act as my strategic thought partner and advisor. I want to fully understand the landscape of expert advice on price wars — what strategies, frameworks, and counter-moves have been recommended by the best business thinkers, economists, and practitioners. Cover the full range of current thinking.”