Between inflation, rising interest rates, geopolitical tensions, and growing recession concerns, 2022 was a year of reckoning for both public and private markets. Since the beginning of 2022, the tech-heavy Nasdaq Composite has declined 23% (versus the S&P 500’s 14% decline) and global venture funding reached a thirteen-quarter low in Q1 ’23. Further dampening investor confidence, the failure of several long-standing institutions serving the startup ecosystem, such as Silicon Valley Bank, Signature Bank, and First Republic Bank, sent shockwaves through capital markets and the broader financial services industry. Today’s market represents a radically different fundraising climate—one not seen in nearly 15 years. Many founders find themselves in uncharted territory as concerns linger around the overall health of the fundraising environment, from venture capital to growth equity.

TABLE OF CONTENTS

TABLE OF CONTENTS

The View from 30,000 Feet: How is the Market Trending?

With seismic changes occurring across the broader capital markets and tech multiples at a multi-year low, we are seeing some key trends emerge in the venture landscape:

- The macro environment has impacted investor sentiment. Given the recent political and economic uncertainty, much of private market activity has been put on pause. Despite ample dry powder in the venture space, some investors are not willing to step up to price and set valuation terms, particularly in later-stage funding rounds.

- Early stage valuations have been more resilient. According to recent Pitchbook data, growth-stage companies have been more adversely impacted by the recent market correction and current macro environment than early stage companies. This is in part, due to the growth-stage’s proximity to public markets, whereby investors are confronted with a large gap between the valuation multiple that a growth-stage startup raised at in its most recent round versus where its public peers are trading at today.

- Up rounds are still happening, but taking longer. Despite challenges in the broader public equity markets, companies with proven traction, a path to profitability, and good unit economics are raising up rounds. However, with continued macro and market uncertainty, investors have become more discerning with longer and more rigorous due diligence, causing rounds to take longer to come together.

- Flight to structure. In the startup world, it is customary to raise capital through the issuance of preferred equity, and for founders and employees to hold common equity. As deals became more competitive in recent years, investors also purchased common equity in an effort to obtain the maximum amount of ownership in a given financing round. With today’s more volatile and uncertain markets, investors have returned their focus to preferred equity. Increasingly, they are also requiring terms that provide downside protection and minimum return thresholds, such as payment-in-kind (PIK) dividends, liquidation preferences higher than 1x, valuation ratchets, and participating rights. That said, while structure is becoming more commonplace, it is more prevalent in growth rounds than in early stage rounds. For more on this topic, please see this article written by our Growth investment team on the impact of different structures.

- In SAFE hands. A SAFE, or Simple Agreement for Future Equity, is a financing structure pioneered by Y Combinator. With a SAFE, a company is able to raise capital without formally assigning a value to the business in exchange for certain protections for the investor upon conversion (typically either a valuation cap, a discount to the next financing round, or both). Historically, SAFEs have been primarily used by companies that are pre-product or pre-launch. In the current climate, we have observed the SAFE structure being utilized by an increasing number of revenue-generating Series A and Series B companies, who need to raise an interim round to get to certain milestones ahead of a more formal priced round. Such companies usually have the internal support to defer an interim valuation event.

- Convertible notes have taken off. Convertible notes are a form of debt that can be converted into equity either at a valuation cap or at a discount (typically 20-30%) to a company’s next financing round just like a SAFE. However, unlike SAFEs, convertible notes offer downside protection given the asset class of debt, as well as potential minimum-guaranteed thresholds. They also incur interest (that can convert into equity in the next priced round) and have a predetermined maturity date which creates a ticking clock for the company to raise future financing and repay its debt. In this current climate, we are observing a number of companies raise convertible notes as well as the emergence of creative new structures such as pre-IPO convertible debt with a conversion price set at a premium to the company’s eventual IPO price.

- Recaps are due to make a comeback. When companies looking to raise capital find interest from investors who are not willing to sit behind the company’s existing investors, or preference stack, the standard solution is for the new investors to “reset” the ownership by proposing a financing not only at a different valuation (in order to achieve their ownership objectives) but also to put the new investment at the top of the preferred stack (most senior), and sometimes reduce the existing preference stack to make a return for the new investment more likely. This form of financing, through an ownership restructure, essentially force-converts existing preferred equity holders into not only a common equity position, but also often at a down-ratio whereby their ownership percentage is also significantly reduced. A variant of this deal structure, known as a “pay-to-play,” offers existing preferred investors the right to participate under the new financing terms and by doing so, are offered a conversion mechanism to preserve some or all of the preference of their original investment. While pay-to-play financing structures tend to be uncommon in strong markets, we have seen more of these situations arise in the current climate and expect to see this trend increase.

TABLE OF CONTENTS

TABLE OF CONTENTS

What it Means for Startups: The 16 Commandments of Raising Equity in a Challenging Market

Despite the current environment, we believe that great founders and great businesses will always have options when raising capital. Amidst this period of market uncertainty, we offer a series of recommendations and advice—our “commandments”—for founders looking to raise in this “new” normal.

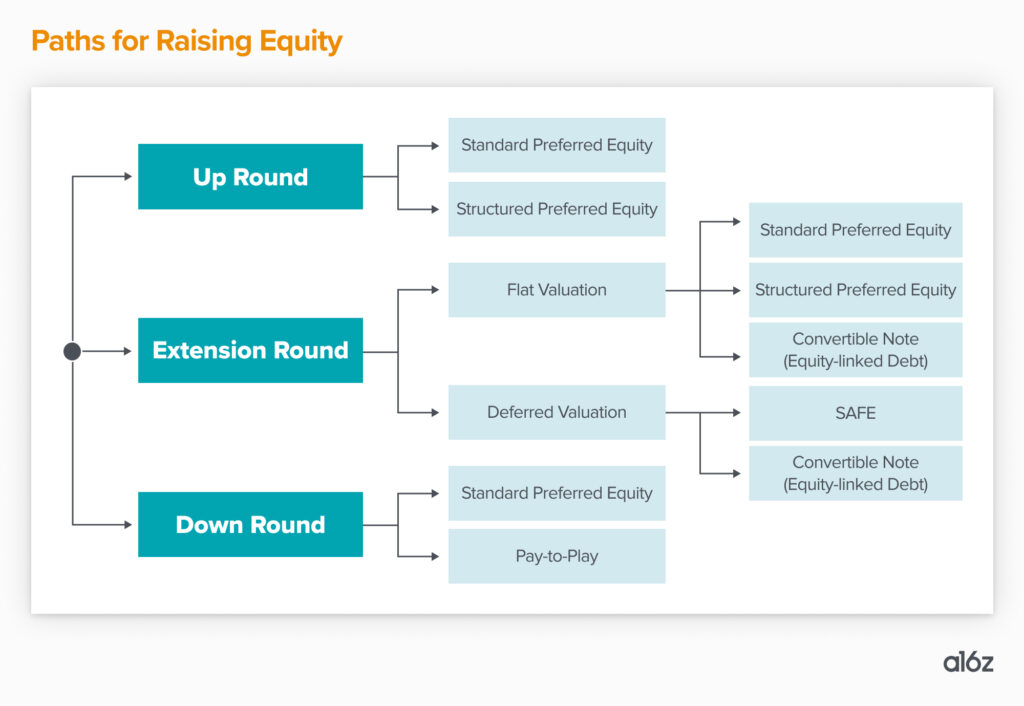

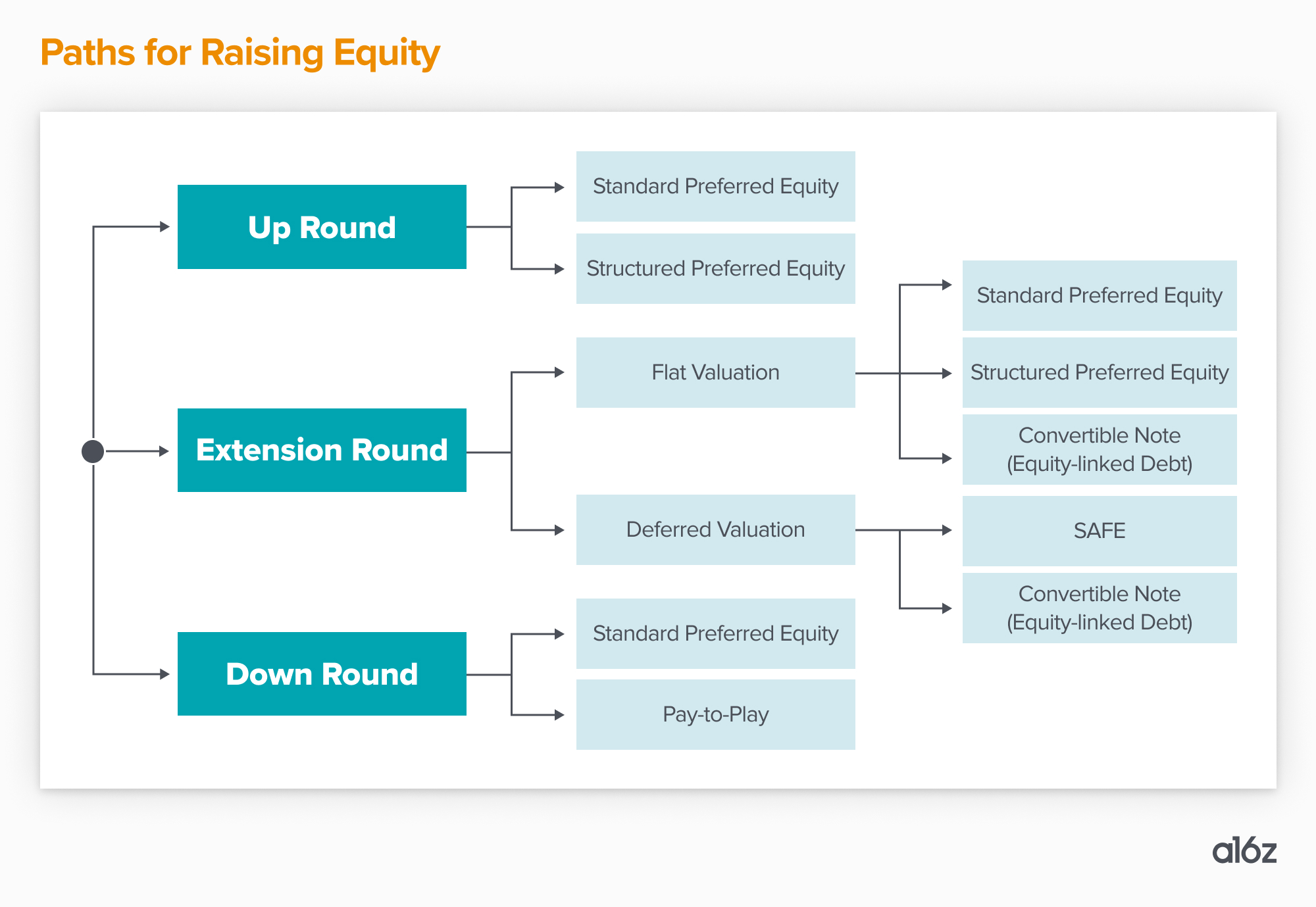

- Be flexible on structures and sources. Our Managing Partner Ben Horowitz puts it best: “If you are burning cash and running out of money, you are going to have to swallow your pride, face reality, and raise money even if it hurts.” For startups looking to raise in this current environment, it is imperative to internalize that there are a number of viable paths to raise equity (as depicted by the diagram below), including down rounds and flat rounds. There are also many alternative pools of investment capital to tap into beyond VCs, such as strategics, sovereign wealth funds, and family offices. Eliminate artificial boundaries and taboos from your vocabulary: “I want a valuation of at least $X,” “I won’t accept convertible debt,” “I don’t want strategics on my cap table.” Be open-minded when different opportunities arise. Having an inflexible attitude will greatly decrease your options and make it more challenging to raise capital.

- Don’t begin conversations with price expectations. Founders should avoid anchoring conversations around price expectations or last round’s valuation. You run the risk of not receiving any term sheets if you convey up front an expectation of a high price. Securing even a low-valuation term sheet early on will help build competitive tension, which you may be able to leverage towards additional term sheets and better terms. You just need one “yes” to get the ball rolling.

- Optimize for size, not dilution. For founders who have raised capital during the last few years, the standard approach has been to optimize for dilution given the easy accessibility to capital. However, in today’s environment, founders should instead consider optimizing for round size. If a round has come together and you are being offered more capital than you had intended to raise, taking the incremental dilution now for the additional capital can be a prudent move. This will not only offer a runway extension, but also help avoid a potential situation down the road where you are forced to raise again following a short interval.

- Start early to account for the unexpected. During a period of market uncertainty, it is critical to prepare and build in sufficient buffer time to account for unanticipated obstacles, such as partner-level meetings taking longer to schedule, extended confirmatory diligence, or other unforeseen funding delays. By starting your fundraising journey early, you can ensure that you have a time-cushion to fall back on when the unexpected happens.

- Prepare well to run an efficient process. Take time up front to thoroughly rehearse your pitch, sharpen your delivery, improve your deck, and prepare a data room. Diligent preparation and deliberate planning will help reduce your chances of making an error, which can be costly and time-consuming to fix later on. Completing a fundraising process expeditiously is imperative in this environment. You do not want your company to become a “stale listing,” which in real estate, refers to properties that have spent too many days on the market. Stale listings are often caught in a vicious cycle: the perception is that something is wrong with it, which keeps other would-be buyers from purchasing it. Similarly, in the venture capital world, startups may also be viewed as “stale” or unattractive to investors. The key to avoiding this stigma is to run an organized and efficient process aimed at creating competition.

- Engage your insiders. Proactively engage with your existing investors (insiders) about your upcoming fundraising plans. Having an insider commit to participating in or leading your round may serve as a strong endorsement and vote of confidence that can encourage other market participants to also invest in the round. However, insiders may be at different stages of their fund lifecycle and may have limited reserves so it is important to have honest and open conversations with them on whether and how much they are able to commit.

- Nurture ecosystem relationships.As our team has discussed in the past, we believe it’s never too early to begin building relationships within your ecosystem, from both a commercial and strategic partnership perspective. Relationships take time to nurture, so this is time well-invested and will pay dividends in the future. These developed relationships can be incredibly useful in helping to catalyze a potential financing, whether it be a bridge round alongside existing investors, a strong signal for new investors to co-invest as part of a larger financing round, or a stage-setter for a potential strategic transaction in the near to long term.

- Ask yourself the difficult questions. Even before you meet with investors, think about where investors may push back. Why are newer cohorts showing lower retention? Why is CAC rising? Why have organic acquisitions stagnated? This enables you to anticipate key investor concerns and proactively address them by preparing materials and answers in advance. Investors want to engage with founders who are thinking critically about what they’re doing right, what they’re doing wrong, and what they intend to do differently.

- Pressure-test your burn multiple. Stress-test your burn multiple, which we define as cash burned divided by net ARR added. In other words, how much cash are you burning to generate each incremental dollar of revenue? Evaluate how your burn multiple is changing across months and quarters and explore what you can do to improve this metric. Moreover, identify areas that are your largest sources of burn, which areas represent “burn-sinks” vs. burn-investments and have a rationale for why spending is justified. Investors are looking to invest in companies that are able to balance growth and cash burn, as well as those who know how to do more with less.

- Don’t pursue growth at the expense of profitability. The Rule of 40 (Ro40), defined as the sum of a company’s revenue growth and profitability margin, is a metric used by investors to gauge a growth-stage startup’s performance. It succinctly captures the trade-off between growth and profitability. Companies with identical Ro40 scores aren’t necessarily treated the same, since the pendulum between growth and profitability swings over time. During the strong market environment of recent years, the scale tipped in favor of growth, with investors rewarding startups that were able to demonstrate rapid growth even at the cost of poor unit economics and profitability. Since then, the goalposts have moved drastically—the “growth at all costs” mantra has come to an end. Today, investors are putting more weight on profitability. If your unit economics are in the red, consider prioritizing efforts to improve your company’s profitability even if it means achieving lower growth in the present. Growth efforts can always be ramped up later in the company’s journey, but the quest for good unit economics can feel like a Sisyphean task when already operating at scale.

- Be deliberate and precise on use of proceeds. Investors want to partner with founders who efficiently overcome roadblocks. It is not enough to show how much and where you plan to allocate future capital; you must also demonstrate that the juice is going to be worth the squeeze. Which acquisition channels are not saturated and thus will provide the best returns on marketing spend? Which customer segments will you deprioritize because their unit economics will not work even at scale? Which features are you pushing to drive better retention? Demonstrate to investors that you know your business inside-out and present a realistic plan on how you will mobilize funding to target the highest ROI levers and achieve specific milestones.

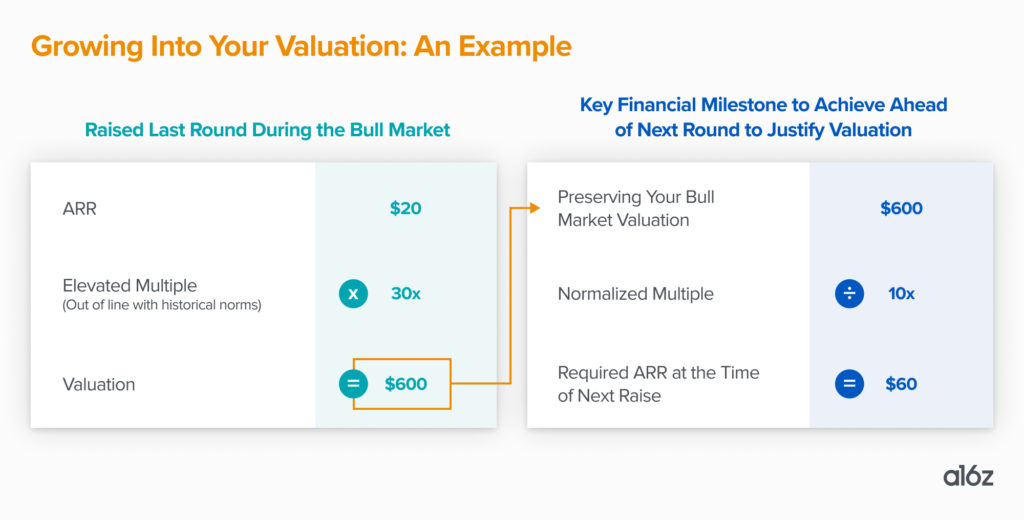

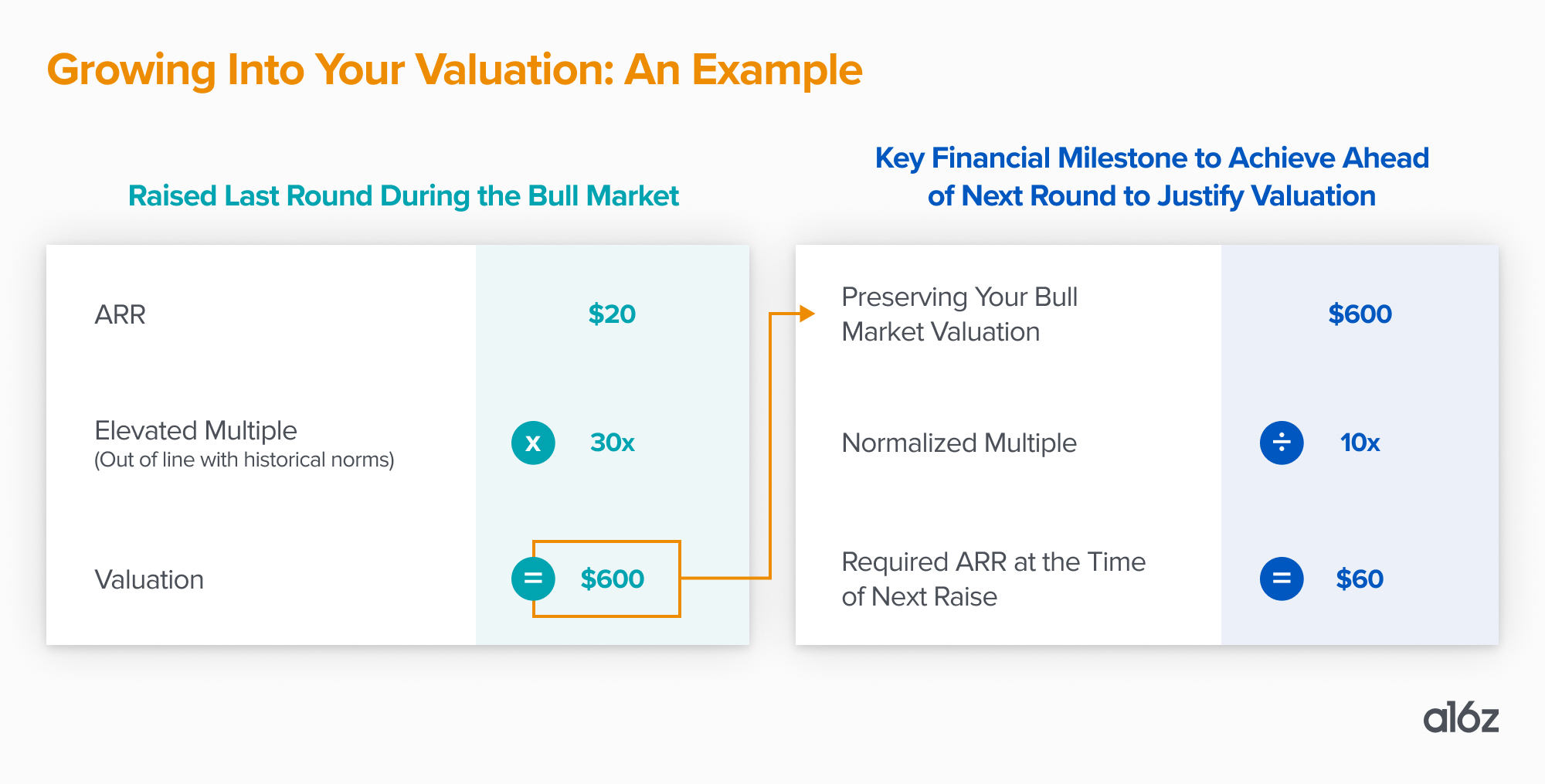

- Grow into your valuation at normalized multiples. If you’re a company that raised capital over the past few years, you likely did so at a strong valuation. Given the recent market correction, your focus today should be setting near-term financial targets that enable you to grow into that valuation at normalized multiples. Balancing offense and defense is key—recalibrate your business plan and adopt operational discipline by evaluating how you’re going to use the capital you’ve raised in the most efficient manner possible to hit the required financial milestones ahead of your next raise. Please see this article written by our Growth investment team on how to think about navigating down markets and scenario planning.

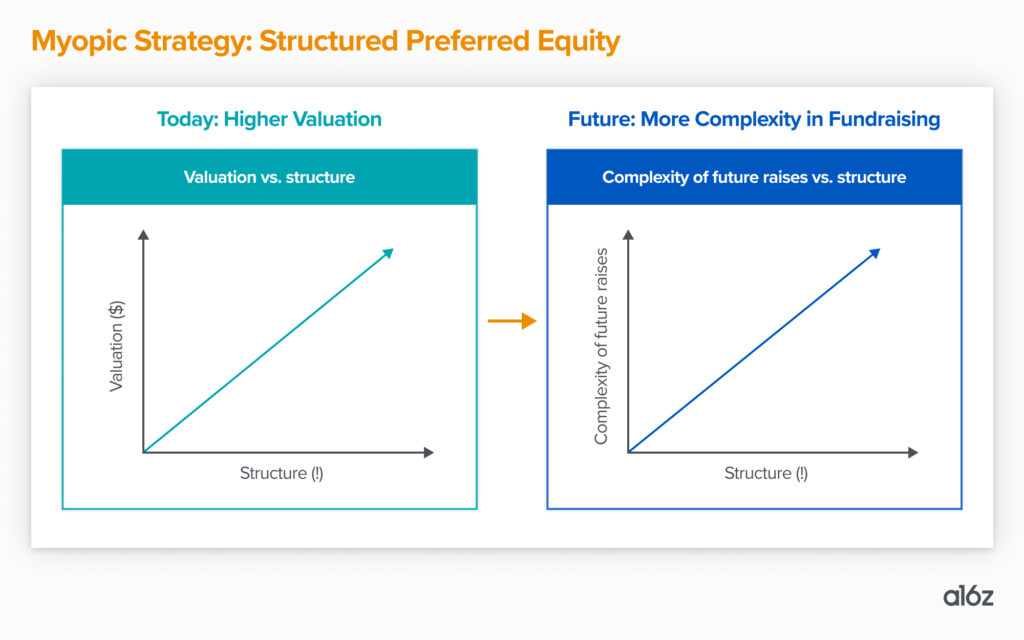

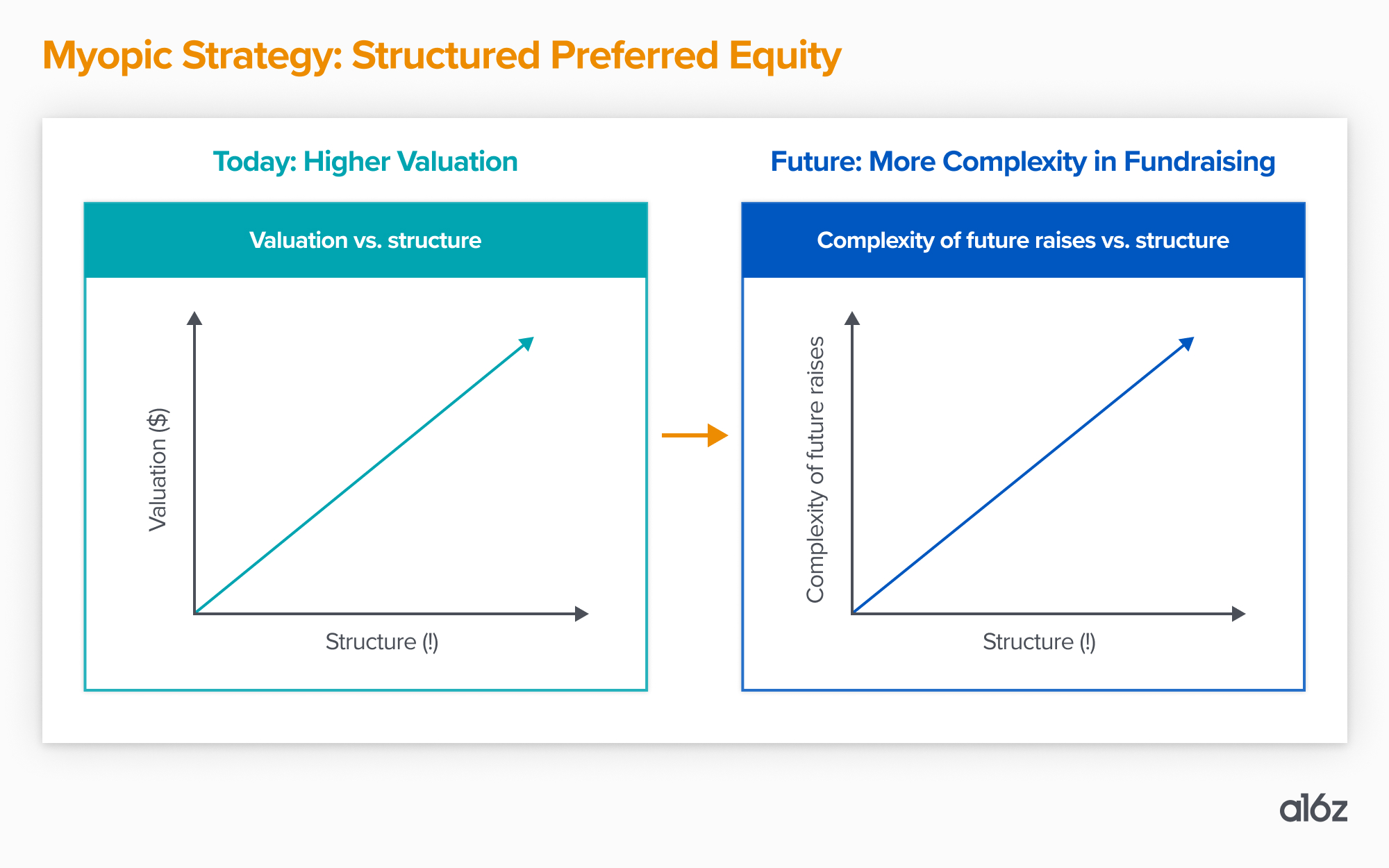

- Don’t myopically view a structured up round. In today’s climate, there are some who believe that securing an up round, even in the form of structured equity, can be a Fountain of Youth that will help maintain both the actual and perceived health of the company. However, founders should be aware that an up round is not a solution for all of the company’s issues. Implementing structure into the company’s capitalization solely for the sake of preserving your last round’s valuation is not an act that is easily reversible and will have downstream effects on future financings. For example, future investors may expect that in subsequent rounds they too will receive the same rights, thereby further diminishing returns to common equity holders, including founders and employees. As such, startups that are several years or rounds away from a liquidity event, may be better off raising a “clean” flat round or down round than an up round that comes with structure such as higher liquidation preference, participation parameters, ratchets, and other atypical governance rights.

- Treat deferred valuation as a Band-Aid, not a cure. To address the potential valuation gap between a wide bid and ask spread, some companies are electing to raise capital via SAFE or convertible note structures that defer the topic of pricing. The rationale behind this approach is that it gives the company more runway and resources to achieve key milestones ahead of an eventual formal priced round. The notion of deferred valuation as a magic bullet solution is alluring, but may ultimately present challenges and could derail the eventual priced round. Founders should exercise caution and consider this approach carefully before committing. If you have immediate liquidity needs or anticipate reaching near-term milestones, then this solution between financing rounds may be suitable for you. However, depending on your specific circumstance and the terms of the instrument, it may also lead to misaligned incentives between existing and deferred round investors, as well as present long-term issues with your capital structure if milestones are not met.

- Communicate with candor. There may be a tendency to not discuss or communicate a fundraising outcome that on the surface seems sub-optimal. One misconception is that it might spook employees, partners, and vendors by raising concerns that the company’s prospects are limited or challenged. On the contrary, it is imperative in such instances to be transparent with employees about where things stand and to listen to their concerns. Candor and honesty in such moments will help build loyalty and enable you to lead more effectively.

- Preserve optionality. As you embark on your fundraising process, there is a chance that you may not be able to secure the funding you need. As such, it is important to be prepared for the possibility of a sale, soft landing, acquihire, or wind-down. Make sure to set aside sufficient cash and time to explore these alternative paths and potentially dual-track alongside the fundraising process.

TABLE OF CONTENTS

TABLE OF CONTENTS

Conclusion

While the strong market environment over most of the past decade has yielded many positive fundraising outcomes, it is important to take a step back and treat fundraising for what it is—a milestone versus a destination. A flat or down round should not be viewed as a death knell for a startup. Many successful, category-leading companies such as Airbnb, Doordash, Block, and Meta raised flat or down rounds along their startup journey. The current environment represents a great time to build, without the distraction of hype cycles, speculative valuation chasing, and unbridled market exuberance. While the capital markets environment has undoubtedly changed following an extended market run, the future most certainly holds great opportunity for founders and investors alike.

The views expressed here are those of the individual AH Capital Management, L.L.C. (“a16z”) personnel quoted and are not the views of a16z or its affiliates. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by a16z. While taken from sources believed to be reliable, a16z has not independently verified such information and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. In addition, this content may include third-party advertisements; a16z has not reviewed such advertisements and does not endorse any advertising content contained therein.

This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by a16z. (An offering to invest in an a16z fund will be made only by the private placement memorandum, subscription agreement, and other relevant documentation of any such fund and should be read in their entirety.) Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Andreessen Horowitz (excluding investments for which the issuer has not provided permission for a16z to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://a16z.com/investments/.

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Please see https://a16z.com/disclosures for additional important information.