Visa and Mastercard currently facilitate more than three-quarters of all credit card transactions in the United States, at a time when post-pandemic Americans are now using credit or debit cards for roughly 57% of all transactions (in 2016, it was only 45%). Given the two companies’ long-standing dominance in the payments-processing space, what would it take to disrupt this duopoly and start a new payments Goliath?

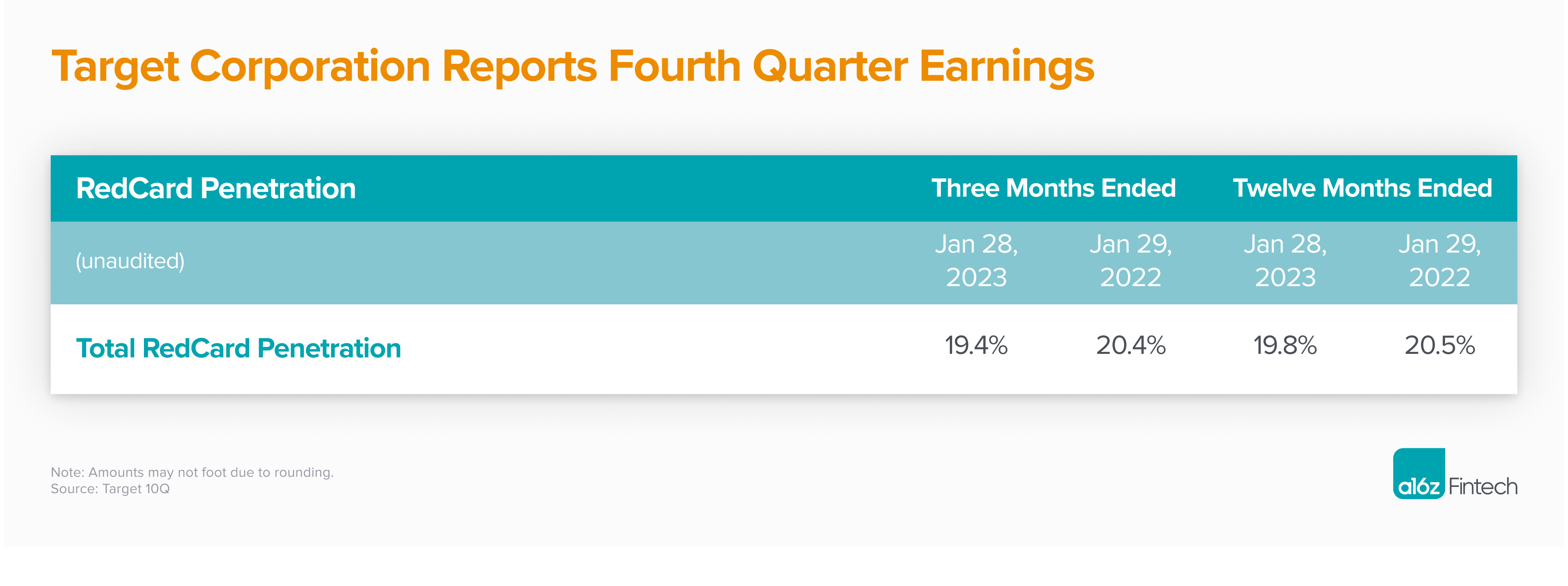

I’d like to direct your attention to the Target RedCard. The RedCard is Target’s umbrella name for its branded card products, which offer users a 5% discount on all purchases at Target stores and on Target.com. The RedCard is such an important KPI for Target that they break it out in every single earnings summary. To wit: Target did more than $100 billion in revenue in 2022, 20% of which happened on its own cards:

But what is extremely interesting and has compelled me to scan every Target 10Q for years, is specifically the Target RedCard debit card, on which more than 11% of Target’s revenue flows. After being connected, the card simply pulls money directly from your bank account, which allows Target to avoid paying the interchange, or swipe, fees that are the bane of all card-accepting merchants.

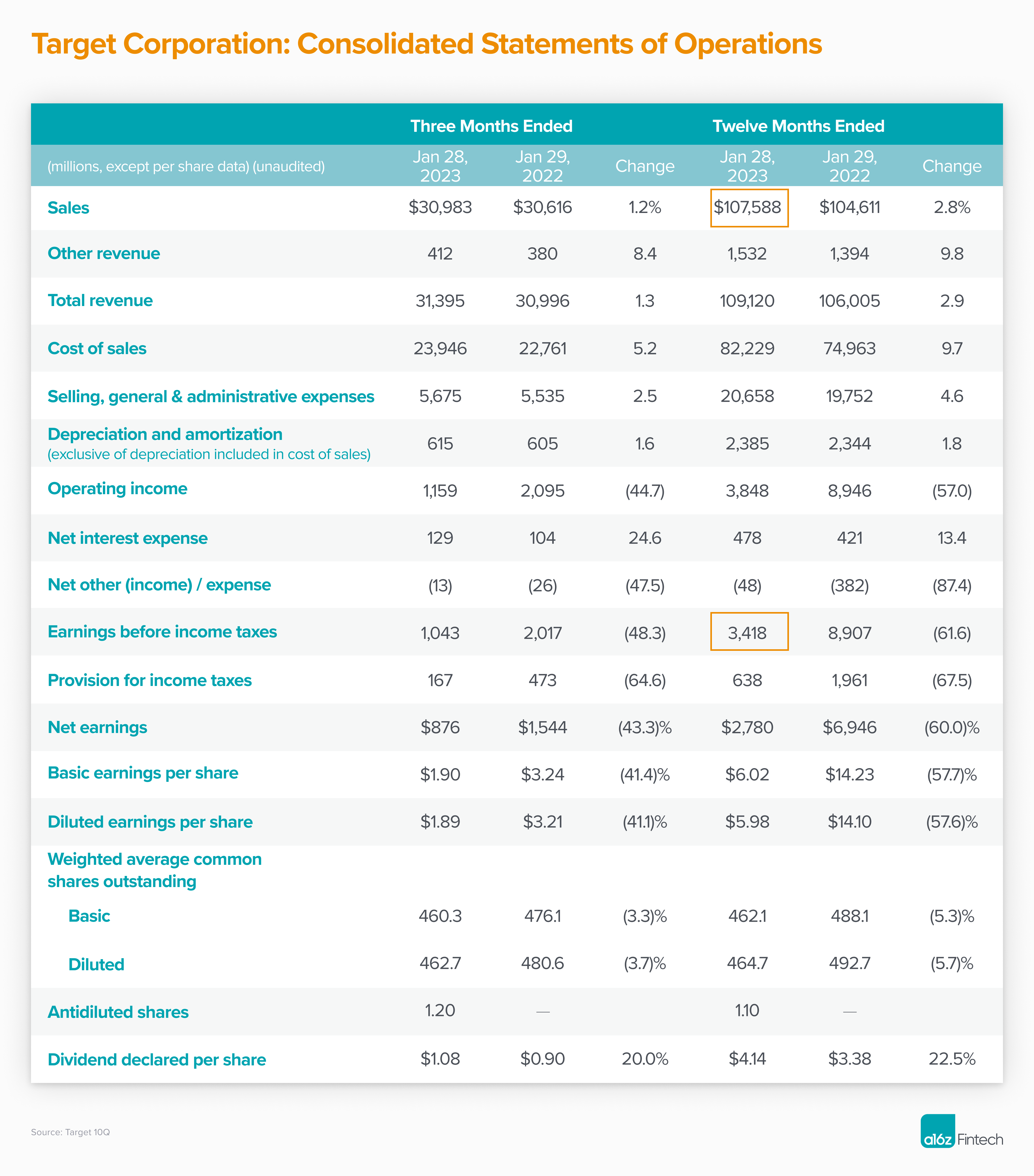

It should be self-evident why this is important. Look at Target’s full-year revenue for 2022: they made $107.6 billion in sales and $3.4 billion in pre-tax income. Now imagine if every transaction at a Target store or at target.com were made with a credit card—which is currently not the case—at an average fee of 2%. This would result in $2.2 billion in incremental income if all payments shifted to ACH, which would be 65% more profit!

Target has impressively shifted 20% of their entire sales to their own cards. The only “illogical” part of this is that to save ~2%, the company is… giving up 5%, albeit to the user in the form of direct savings at Target, which is the primary benefit of the RedCard.

Target isn’t an outlier here. Most “frequent interaction” or high-frequency billing companies do the same. Verizon and AT&T, as additional examples, give you substantial monthly savings for moving your bill-pay off of credit cards and to ACH (or sometimes debit cards, given the lower average fee).

When you sign up for a RedCard debit card, you link your existing bank account to the card and let Target pull funds from it. It’s just a “router” to your existing bank account. So effectively, the debit RedCard is an abstraction layer around payments, mapping a point-of-sale (POS) transaction at a Target store to a subsequent low-cost ACH debit from an existing checking account.

This is harder than it seems. For anyone in credit/debit payments, you might recognize the “verbs” of payments—authorize, capture, settle, void, and credit—not to mention things like chargebacks. ACH has fundamentally different “verbs,” and the RedCard is a Rosetta Stone of sorts.

So why is this model potentially the future of payments? For one, tools like Plaid have made the connection extraordinarily easy. You don’t have to remember your bank account number or routing code to send a payment. All you have to do is log-in to your bank account once and you’re done; it’s a behavior consumers are increasingly used to.

In fact, every high-frequency biller—Albertson’s, Netflix, Walmart, Costco, Safeway, Microsoft, Disney, etc.—should be doing this, in addition to experimenting with pricing and benefits. It’s likely that trillions of dollars of “frequent merchant-consumer interaction payments” could shift in the process. Additionally, if companies have a link to a customer’s checking account and a dominant or frequent relationship with them, the additional “fintech” cross-sells that are available to them are endless.

That said, while I think Target has been smart to roll this out, paying 5% to save 2% (and justifying it by showing increased engagement, which likely reverses cause and effect and shows sampling bias!) is not smart. A better alternative, in my opinion, would be to provide customers with a one-time benefit to make the switch. As an example, imagine if Netflix started offering such a benefit and started offering customers, upon log-in, a $2 one-time discount if they clicked and switched their payment method to direct debit. This would provide Netflix with long-term savings of more than $100 million a year in North America alone, based on their rough interchange costs.

The “hard” part of this, not surprisingly, is software. What we need is a “RedCard as a Service” for retailers—“frequent interaction” retailers in particular. This would likely sit alongside the existing payments stack, or maybe above it, because ideally the one team (at the merchant) that handles dispute resolutions and chargebacks, or refunds, or store credits… doesn’t care about the tender type. All of that is just abstracted away into whatever tools they already use.

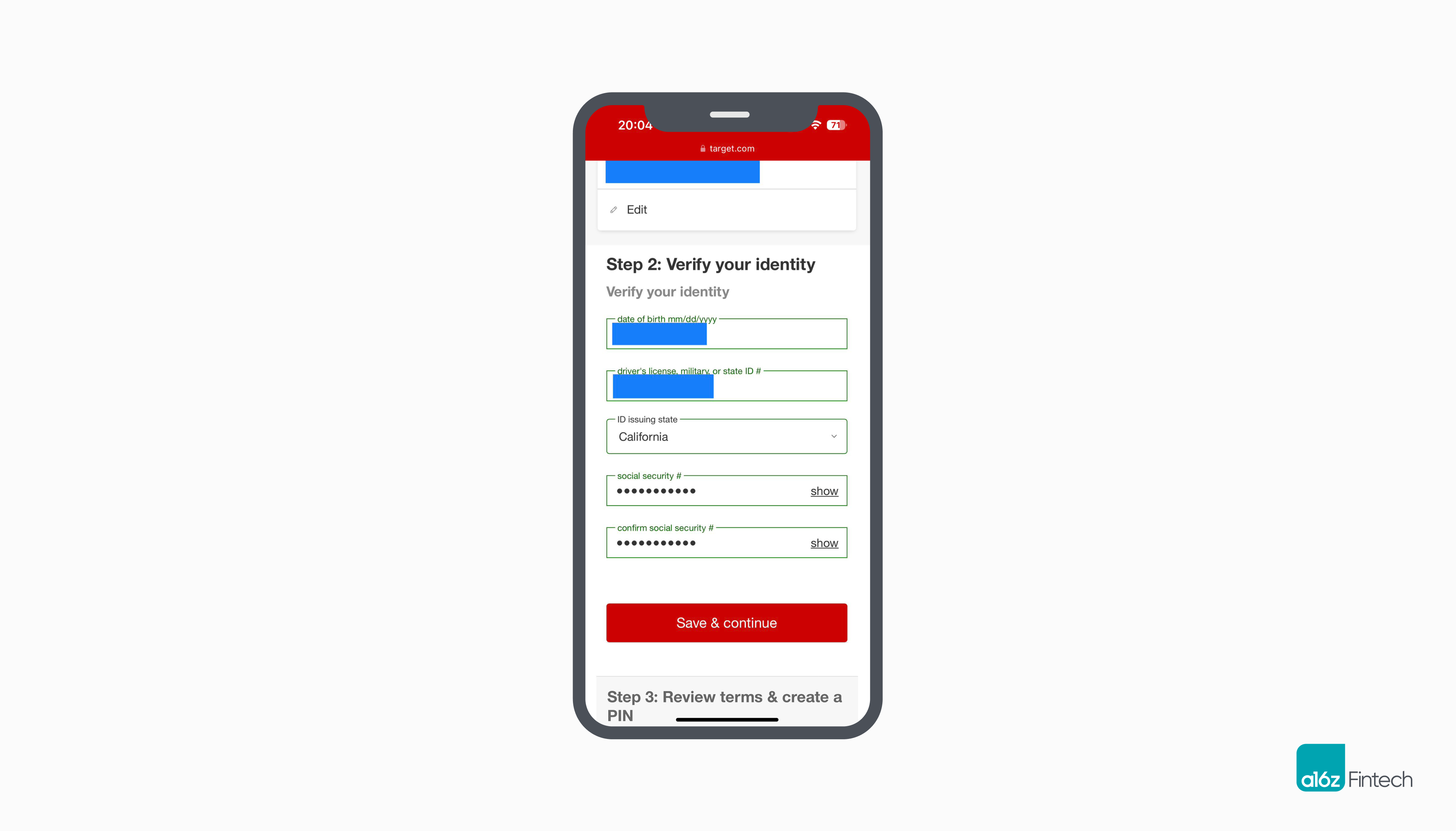

The other thing that’s needed is a much better onboarding experience. Frankly, it’s shocking that Target does 20% of its revenue on its own RedCards given how complex they make the onboarding process and how much information they gather from the consumer (see below). Better software/CX/UX would make the offering much more compelling.

Luckily, inertia, one of the twin moats that protects so much of banking, is now decreasing thanks to improved technology, and consumers are more willing to switch up their payments methods. (Rewards, the process by which merchant fees fund customer benefits, with banks in the middle, remains a stubborn reason why “RedCard as a Service” hasn’t previously taken off.)

A truly magical experience would be what I would call the “Customer IQ Test,” whereby online customers are asked, “Do you want to save $5 right now by switching your Visa Card ending in 2655 to your Bank of America account ending in 7688? Click Yes to confirm and you’re done” while an automatic mapping of their credit/debit card to their existing checking account is done in the background. The various credit bureaus and other players with access to large depositories of bank credentials and PANs (primary account numbers, i.e., credit and debit cards) already have this ability. Another version of this test might offer customers the opportunity to prepay $1,000 of spend at a particular company, say Safeway, for only $950. This deal would ensure the customer buys all of their groceries at Safeway—so loyalty and fee minimization in one package. A quasi-subscription—where, for example, you are automatically billed $100 a month by Safeway to get $105 of store credit—could be another option.

Stepping back, there are still good questions around how many frequent billers the average customer may have, what merchants this might make sense for, and more. But in general, the tools to create a RedCard as a Service are either coming or already exist to make this offering easy, fast, and low-friction… and the economic incentive for merchants is MASSIVE.