Capital allocation is a core part of any CEO’s job, and it’s particularly critical for growth-stage CEOs. After all, once your company goes public, you’ll be expected to justify every dollar you spend.

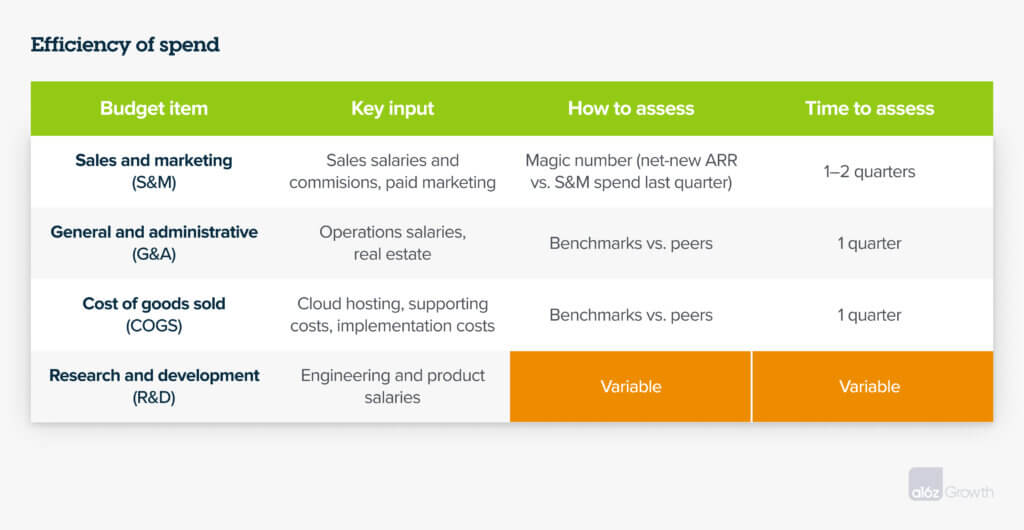

Most growth-stage CEOs I work with know how to tell if they’re efficiently allocating capital in every part of their budget with one glaring exception: research and development (R&D).

In board meetings, we scrutinize the efficiency of sales and marketing (S&M) spend, costs of goods sold (COGS), and general and administrative costs (G&A). But when it comes to R&D, I consistently see CEOs allocate huge amounts of capital with very little rationale to justify or explain it.

R&D spend is the lifeblood of technology companies—all the more so as companies race to build and incorporate AI into their products to remain competitive. Without a product that provides unique value to customers, nothing else matters. Every function of the organization is in service of getting the products in the hands of customers in exchange for money.

If R&D is so critical to a company’s success, why then do R&D budgets lack the same discipline of other spend categories? Because assessing the ROI of R&D spend is far less straightforward. The return on R&D is variable and often happens over a longer time horizon compared to other budget line items. Measuring the efficiency of S&M spend is usually a matter of quantifying LTV:CAC, and most tech companies can identify inefficiencies within 2 quarters. To improve the efficiency of spend on cost of goods sold (COGS), most growth-stage leaders can optimize seat-based spend or renegotiate consumption-based contracts in a quarter or 2. And finding inefficiencies in overhead (e.g., G&A), especially in tougher market conditions, is often a matter of assessing office space, worker productivity, legal costs, etc.

Ultimately, while R&D is perhaps the most important capital to allocate, it’s also the hardest capital to efficiently allocate.

So, when you’re at the beginning of your budget planning process, how do you figure out if you should spend $30M, $50M, or $100M on R&D? And then how do you figure out where, exactly, those dollars go within R&D? And, especially when you’re considering integrating a new technology platform into your business—like AI today, or cloud a decade ago—how do you invest in innovation without losing control of your runway and budget?

Here’s how I wish more growth-stage teams approached their R&D spend:

- Use benchmarks to initially ballpark your overall spend (but remember there are good reasons to vary from benchmarks).

- Map your spend to your product roadmap, then attach an expected ROI and timeline for the expected return.

- Focus on performance management of your product and engineering teams as early indicators for what R&D investments are working, and which aren’t.

1. Start with benchmarks

Benchmarks are helpful to reference when you’re allocating capital across all budget items, and your board and investors can help with identifying the most relevant benchmarks for your company. Benchmarks don’t represent what you should spend, but are rather good starting points to help you articulate why you’re spending more or less than comparable companies, how long you plan to continue spending that way, and what you expect to get out of that incremental spend. Many companies have good reasons not to conform to R&D benchmarks, especially if they’re creating new categories or building at the forefront of a new technology like generative AI. That said, if you’re spending a bunch more on a given product than your competitors are, you should charge more for that product because it offers more value to customers, or that extra spend isn’t worth it.

We pulled benchmarks for R&D spend from private and public companies in application, infrastructure and security, and consumer internet.

![]()

2. Map spend to your product roadmap

As the CEO, you likely have no shortage of compelling ideas for what to build coming from your employees, customers, and investors. While benchmarks can provide some guidance on appropriate overall spend, really effective R&D capital allocation involves mapping your spend to clear product roadmap priorities.

The challenge, of course, is that product roadmaps operate on multiple time horizons, and the ROI of different R&D spends typically maps to those different horizons. Some investments will generate returns within a few months, while others may take years to produce results.

The 70–20–10 rule for allocating R&D—sometimes it works, sometimes it doesn’t

How, then, do you prioritize? The best known framework for R&D spend for companies that have found product-market fit is the 70–20–10 rule, where 70% of spend goes toward investment in the core product, 20% toward new product feature development or smaller products in their nascency, and 10% toward more speculative new products (sometimes called moonshots).

The problem with the 70–20–10 rule is that product is so multifaceted that it defies a generalizable rule or framework. Different companies operate in different markets and competitive dynamics, and your priorities and spend will depend on competitive intensity, market size and runway for your existing product, and how likely you are to win the market with an additional product.

In typical market conditions, new customers may be clamoring for new features. Building those features will increase adoption and expand usage, so it makes sense to allocate ~20% of R&D to building them. But during major platform shifts, like the current shift to AI, many companies have to rapidly shift product direction. In the most extreme cases, a 10% moonshot can suddenly become the company’s core focus and 80% of R&D spend. Unsurprisingly, many great product bets have come from veering from the 70–20–10 rule.

Imagine if, in 2007, Netflix decided to follow the 70–20–10 rule. They would have focused primarily on building a better DVD rental business and likely gone the way of Blockbuster Video. They succeeded, where Blockbuster failed, because they understood that a huge entertainment platform shift and change in consumer behavior was beginning. They wisely allocated the majority of R&D to pivot to a new streaming product and reinvented themselves for a new platform era.

For many growth-stage companies, AI is a similar existential shift, likely to dominate workflows they previously owned. For these companies, innovation is a matter of life or death, and the best way to survive is to nail the product for a new platform—and that means nailing R&D spend.

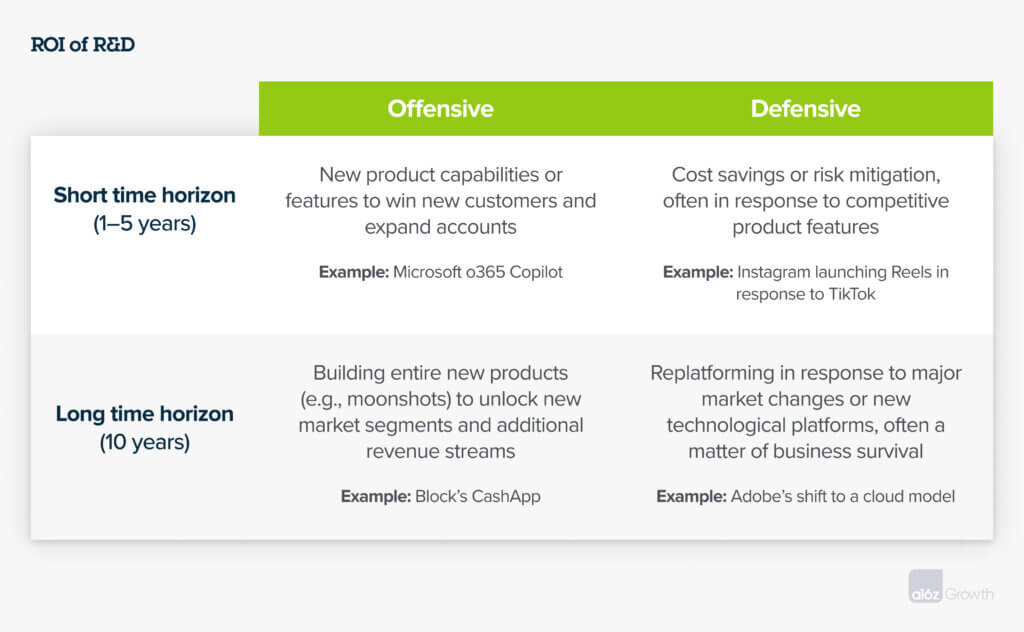

My 2×2 framework for the ROI of R&D

The important product conversation to have with your board and your teams is the expected timelines and returns on your R&D investments. Generally, I think of the ROI on R&D investments as a 2×2 grid, in which bets are offensive or defensive with a short- or long-term time horizon.

Offensive bets typically deliver paybacks as business growth, product features, and developments that unlock new markets or consumer spend. Short-term offensive bets have shorter development cycles and more predictable returns. Microsoft’s launch of the o365 Copilot earlier this year, for example, took less than 12 months to develop after the launch of ChatGPT with the potential to generate additional revenue as soon as it launched. Long-term offensive bets are usually multi-year, complex product developments that are higher risk and higher reward. Most moonshots fall into this category. For example, Meta made a long-term, offensive R&D bet on a platform-size shift with Reality Labs. Time will tell if the metaverse is the right bet, but Mark Zuckerberg has made the bet clear: a multi-billion dollar R&D investment and corporate rebrand for the metaverse with a 10+ year payback period.

Defensive bets, on the other hand, avoid risk and minimize losses, often by saving costs or building a product feature to prevent a competitor from winning customers. For instance, a short-term defensive bet might add a feature a competitor launched that is luring away customers, such as when Instagram launched Reels in response to TikTok’s growing market share. A long-term defensive bet, on the other hand, might be a decision to build internal data centers and repatriate data from the cloud, or for an incumbent to replatform, such as when Adobe moved its creative suite to the cloud. In both cases, the initiative requires a big upfront investment that requires long-term dedicated engineering resources and capabilities, but if successful, it delivers compounding advantages over the long term.

The mix of short- and long-term, offensive and defensive bets depends on your product and business priorities. At the board level, it can be helpful to discuss the thinking behind your priorities as well as your expectations for the returns on your R&D spend.

R&D Questions for Board Discussion

- What product development priorities are you currently investing in?

- Why do those priorities make sense in the current market?

- How much are you investing in each product development priority? How did you decide that amount?

- If you succeed, what will it deliver in terms of existing product performance and features or new products?

- How much existing customer pull do you already see for proposed new products?

- What do you hope a new feature or product will return in capital or customer value?

- What risk is associated with failing to maintain parts of the core product?

Answering these questions is an annual exercise, and then requires monthly and quarterly management against performance goals that align to product progress.

Recently, I heard from a public company founder who had done a more intensive zero-based budgeting exercise. They felt that product and engineering spend had drifted, and they were spending on numerous R&D areas without a clear understanding of the business objective. It’s likely not necessary to do this intensive of an exercise annually, but if you need a hard reset of R&D priorities, it’s another tool to consider.

3. Performance manage your product and engineering teams

Once you’ve allocated R&D with a clear set of expectations and timelines, performance management of your technical teams becomes the key to assessing whether the money you’ve allocated is translating into the product and product performance you expected. The down side of Metcalfe’s Law, which says a network becomes more valuable as it increases in size, becomes a very real challenge at the growth stages. Adding more people—in this case more engineers—requires exponentially more communication and vision alignment, and can also become a drag on productivity. (In fact, most growth-stage companies I’ve spoken with who have gone through RIFs found they got more efficient.) Add to that the long time horizon of some bets and the increasingly distributed and remote nature of engineering teams, and it can be easy for underperforming product or engineering teams—and underperforming R&D budgets—to go unchecked.

Missed timelines and overshot budgets tend to be the leading indicators that your R&D investments, in the fullness of time, won’t deliver your expected objectives. Many companies are increasingly relying on engineering management tools to help optimize performance. While I won’t go into the details of performance management for technical teams here, the important thing for realizing the ROI of your R&D is to measure product delivery and performance. (For a deeper look at effective engineering management, we recommend An Elegant Puzzle: Systems of Engineering Management by current Carta CTO Will Larson, who was previously an engineering leader at Stripe, Uber, and Calm).

Ultimately, applying a framework and rigor to ROI is as critical for R&D as other areas of spend. I hope this serves as a starting point for how you should think about assessing your R&D spend when the path and math are not as straightforward, and especially as you continue on your journey of building an enduring company.

Thanks to Justin Kahl, Santiago Rodriguez, Sarah Wang, and Alex Immerman for their contributions and feedback.