Everyone knows that founders have been on a whipsaw over the past several years. Pivoting from growth at all costs in 2020 and 2021 to efficiency in 2022 and 2023 meant slashing budgets, shelving new projects, doing RIFs, and picking fights with your cloud provider over your bills. That’s hard work, and founders should be commended for doing it.

But now, the market is stabilizing and companies’ optimization1 cycles2 are coming to a close.3 Efficiency alone doesn’t build a generation-defining company—it’s table stakes. So this raises the question: what now? What should founders aim for in 2024?

This is the year for growth-stage companies to become Great.

A Great company brings the most innovative products to the market and continuously evolves them to meet changing demand.

A Great company has a strong, defensible business model that can win market share from incumbents.

A Great company uses a tough market as an opportunity to break away from the pack and outrun its competitors.

A Great company has the potential to be a $5B+ public company.

And the best way to become Great is to refocus on generating fast growth.

How does Greatness actually show up in your financials? Below, we analyzed data from 78 US-based or -centric companies founded after 2000 that have a $5B+ market cap and highlighted what it takes to be Great by the numbers—and why growth is especially important on that journey.4

Growth

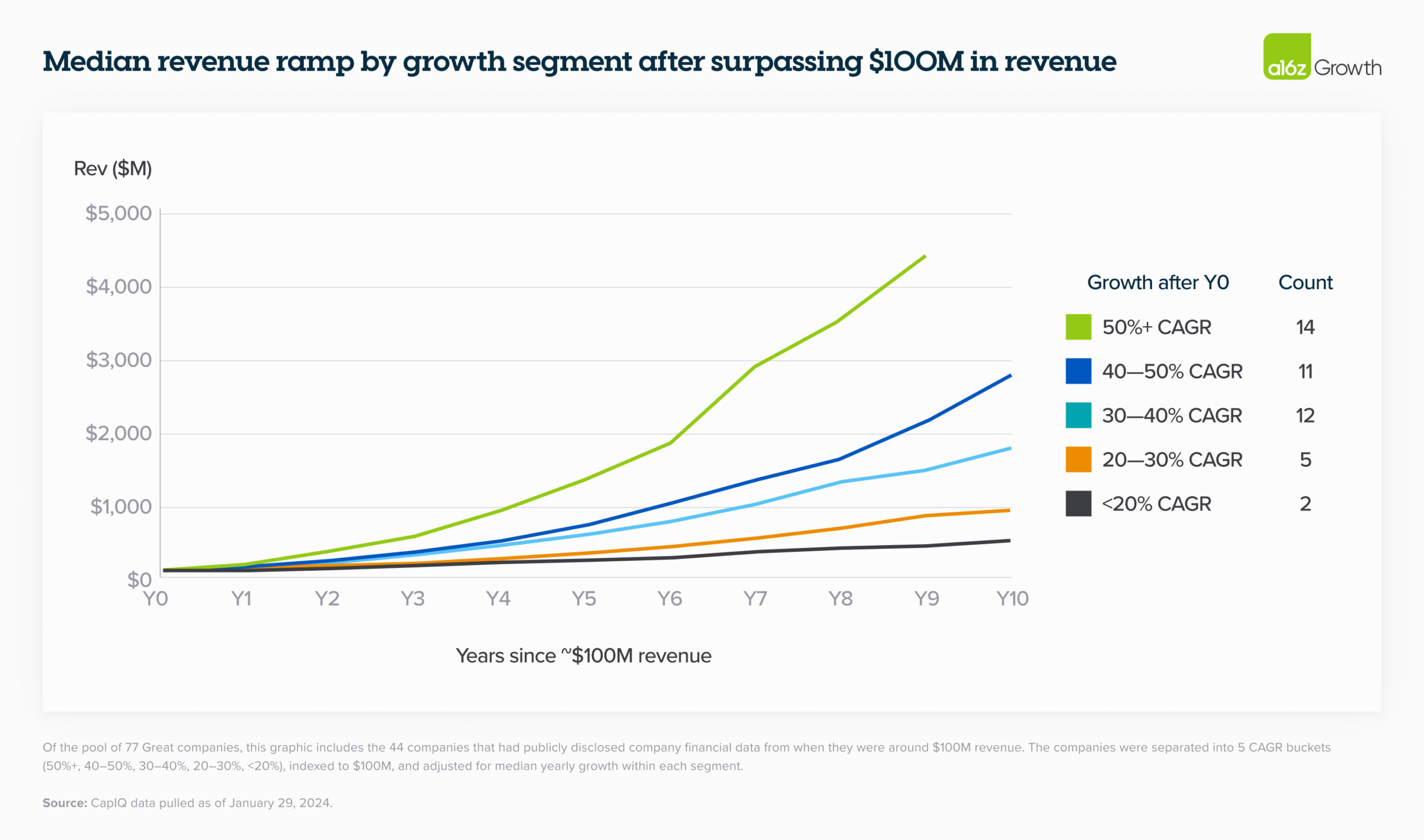

Of the companies whose data we reviewed, we found that 33% grew at a 50%+ compound annual growth rate (CAGR), and 84% of them grew at over 30%.5 It doesn’t matter how much you grew over the last couple years—they were tough!—but if you’re operating at north of $100M revenue and want to be Great, these are the growth rates you need to be shooting for.

Efficiency

Efficiency data over the past 20 years is spotty, but one trend is clear: if you’re >$100M of revenue, your operating leverage—or the growth of your operating expenses—should be lower than the growth of your revenue going forward (barring anything like massive product bets). The important thing here is the trend: is your operating leverage moving in the right direction quarter over quarter?

Eventually, though, the market will expect you to be above the rule of 40 at the time of, or within 12 months of, going public.

Valuation

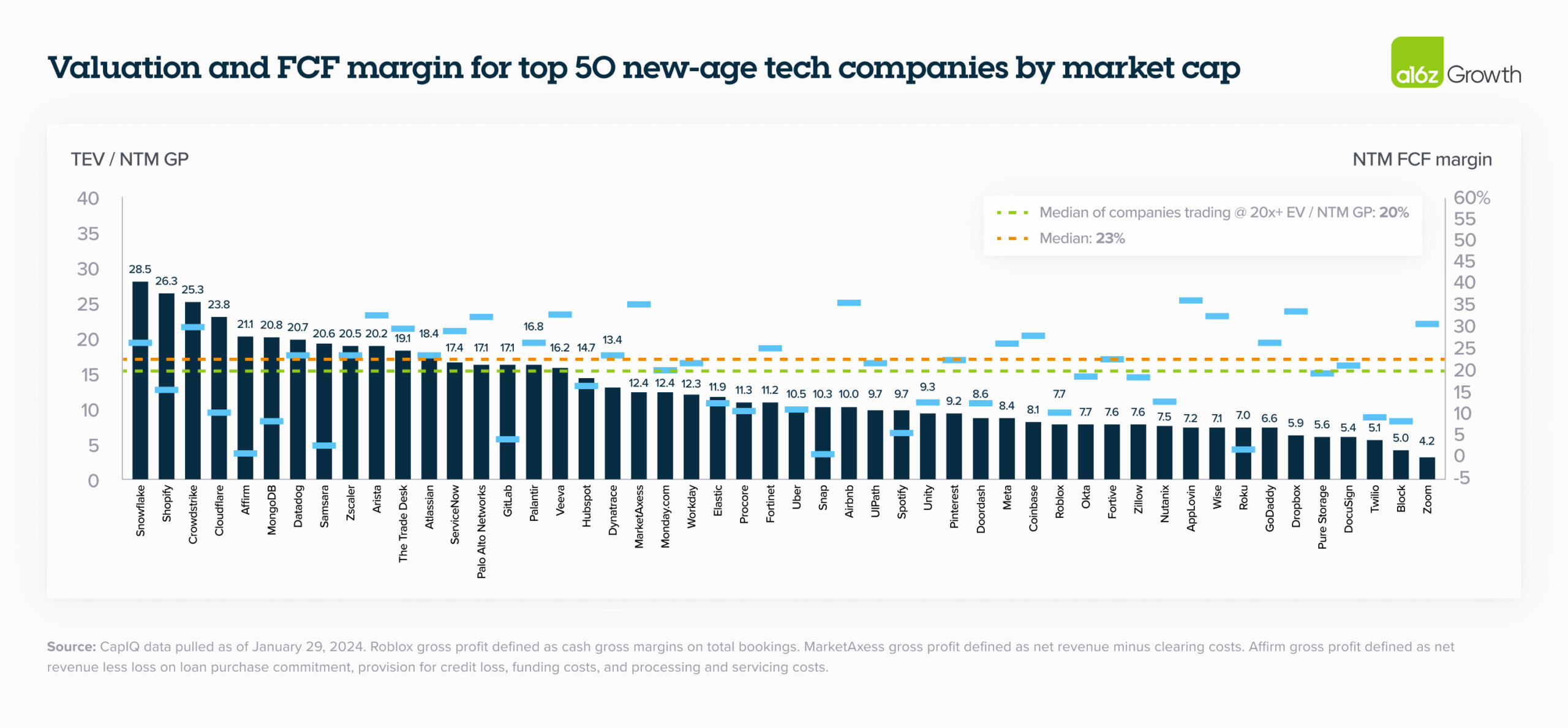

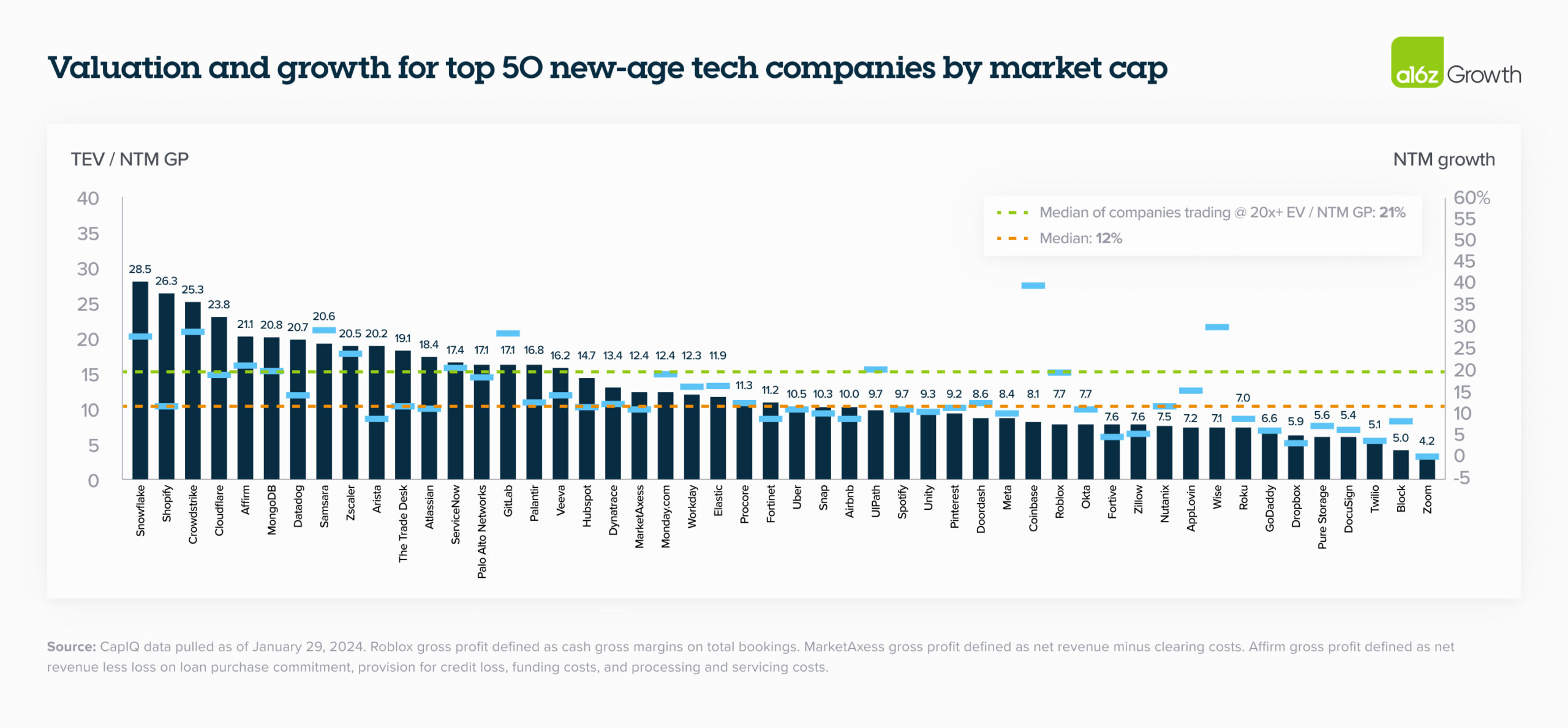

The truly Great, highly valued companies all have excellent growth and margins. But to illustrate why growth is more important, we pulled together 2 charts illustrating the valuations of the top 50 new-age—or, founded post–2000—tech companies by market cap: one that measured valuations as a function of free cash flow margin and one that measured valuations as a function of growth.6

Taking a look at efficiency, there’s no meaningful difference in the median free cash flow margin between the top-trading companies—or the companies trading over 20x—and the remainder of the companies.

But when we take a look at growth, it’s clear that the companies trading over 20x are also the companies that grow the fastest: at 21% NTM growth instead of the median 12%.

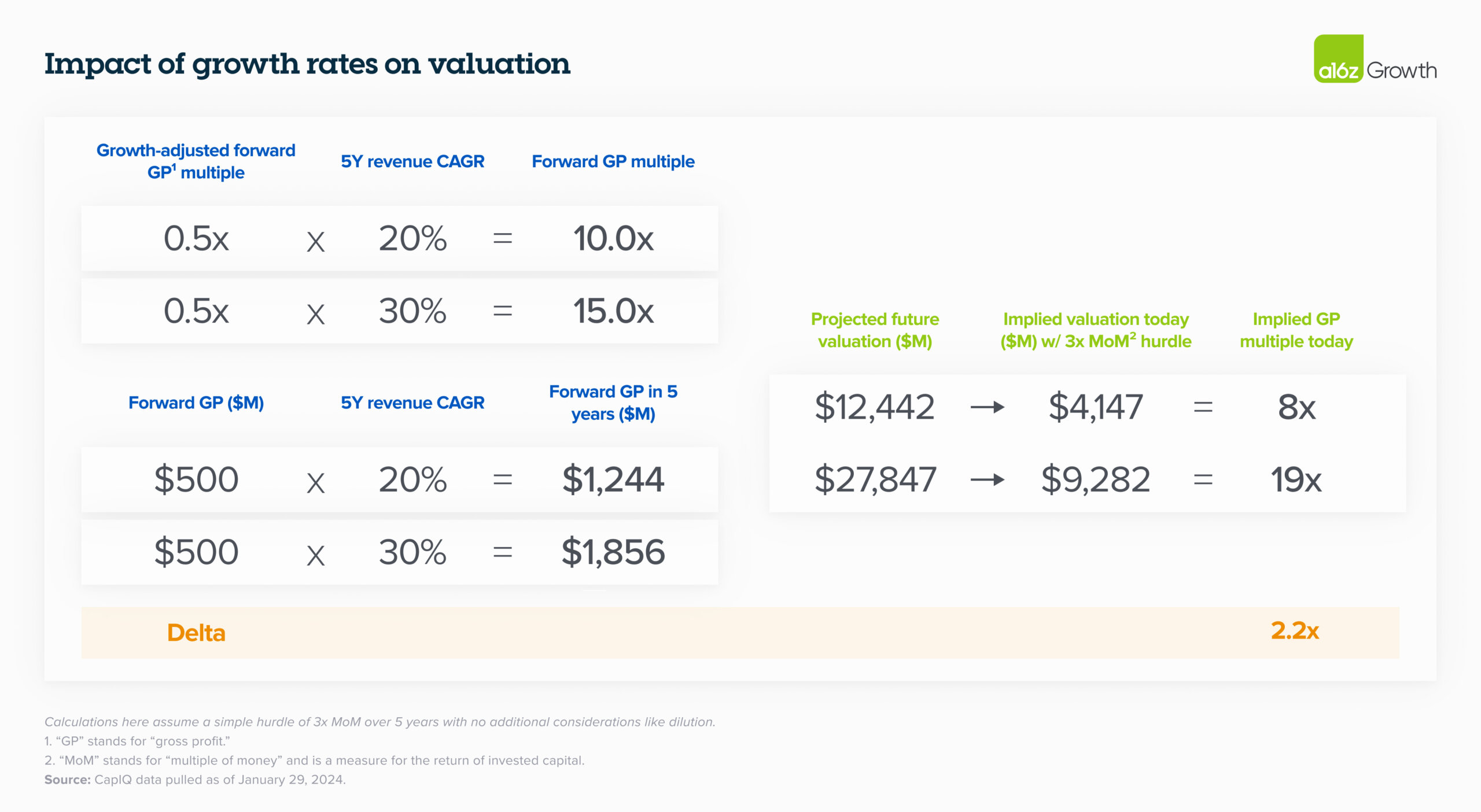

So, why is growth more valuable? This isn’t rocket science, but sometimes high growth over many years can be hard to grok. Here’s the simple math. If you’re growing 30% over the next 5 years instead of 20%, you’re going to be 1.5x bigger on a forward gross profit basis, and you’ll be trading at 15x forward gross profit vs 10x. That’s a 2.2x difference in valuation today.

That’s why some of Greatest companies trade so much higher than the median. For instance, Crowdstrike—who’s projecting 30% growth next year—is trading at 25x, while Fortinet—who’s projecting 8% growth—is trading at 11x.7 (Please note that this isn’t investment advice from me or a16z!)

What’s next

Here’s the best part. When I started my career in growth investing, there were 3 Great public companies: Meta, Workday, and Tripadvisor. Today, there are almost 80, and that’s because founders have built amazing products on the back of platform shifts in tech—like mobile and cloud—that allowed them to deliver innovative products to many more people, much more quickly. AI is going to turbocharge this expansion, and I expect there will be 200–300+ of these companies over the next 5–10 years. By the numbers, the above is what I think it takes to be one of them.

Getting back into the growth mindset is definitely a shift from the last 2 years. But think about it this way: the work you did to get efficient in 2022 and 2023 was the hard part of building a business. Consider 2024 an opportunity to recommit to why you got into this game in the first place—to build amazing new products, outrun the competition, and reach users across the globe.

In other words: 2024 is the year to be Great.

Many thanks to Stephenie Zhang for her contributions to this post.

Sources and footnotes

- "We're going to continue to have these cycles where people will build new workloads, they will optimize the workloads, and then they'll start new workloads. I think that that's what we continue to see, but that period of massive—I'll call it, 'optimization only and no new workloads start,' that I think has ended at this point. So what you're seeing is much more of that continuous cycle by customers, both whether it comes to AI or whether it comes to the traditional workloads." —Satya Nadella, CEO of Microsoft, 2/2/24 earnings call. Source: CapitalIQ

- "Similar to what we shared last quarter, we continue to see the diminishing impact of cost optimizations. And as these optimizations slow down, we're seeing more companies turning their attention to newer initiatives and reaccelerating existing migrations.” —Brian Olsavsky, CFO of Amazon, earnings call on 2/1/24. Source: CapitalIQ

- "People have really driven themselves through these processes and rationalized themselves and are now in a good place to move forward. You can only optimize and rationalize so much." —Frank Slootman, CEO of Snowflake, earnings call on 11/29/23. Source: CapitalIQ

- Data as of January 29, 2024 and pulled from CapitalIQ.

- Of the pool of 77 Great companies, this graphic includes the 44 companies that had publicly disclosed company financial data from when they were around $100M revenue. The companies were separated into 5 CAGR buckets (50%+, 40–50%, 30–40%, 20–30%, <20%), indexed to $100M, and adjusted for median yearly growth within each segment.

- These include the largest 50 companies by market capitalization within the group of 77. Splunk was excluded due to a recent acquisition (despite still being publicly traded). Data as of January 29, 2024 and pulled from CapitalIQ.

- Source for Crowdstrike and Fortinet growth projections and trading multiples: CapitalIQ data pulled as of January 29,2024.