There’s a popular narrative that evil investment bankers are intentionally underpricing traditional IPOs to steal from companies, lining banker pockets and those of their fatcat Wall Street clients. The proof is seemingly obvious: IPOs are 50x oversubscribed! The price explodes by 50 to 200 percent mere hours after the IPO, representing hundreds of millions of dollars in “money left on the table”! Proponents of this view believe the Direct Listing, or now the SPAC, is the panacea for these woes.

An IPO is far from perfect, but this narrative is almost completely false. To understand why first requires taking apart the IPO process, how stock markets work, and what the “price” of a stock means. You can’t fix or improve something without understanding how it works and what’s broken.

First things first: the “price” of a stock is the price of the last trade

If a private company raises $50 million at a $950 million valuation, minting itself a unicorn, does it mean that every share of that company will trade at that price? Not exactly. It just represents the price of the last trade.

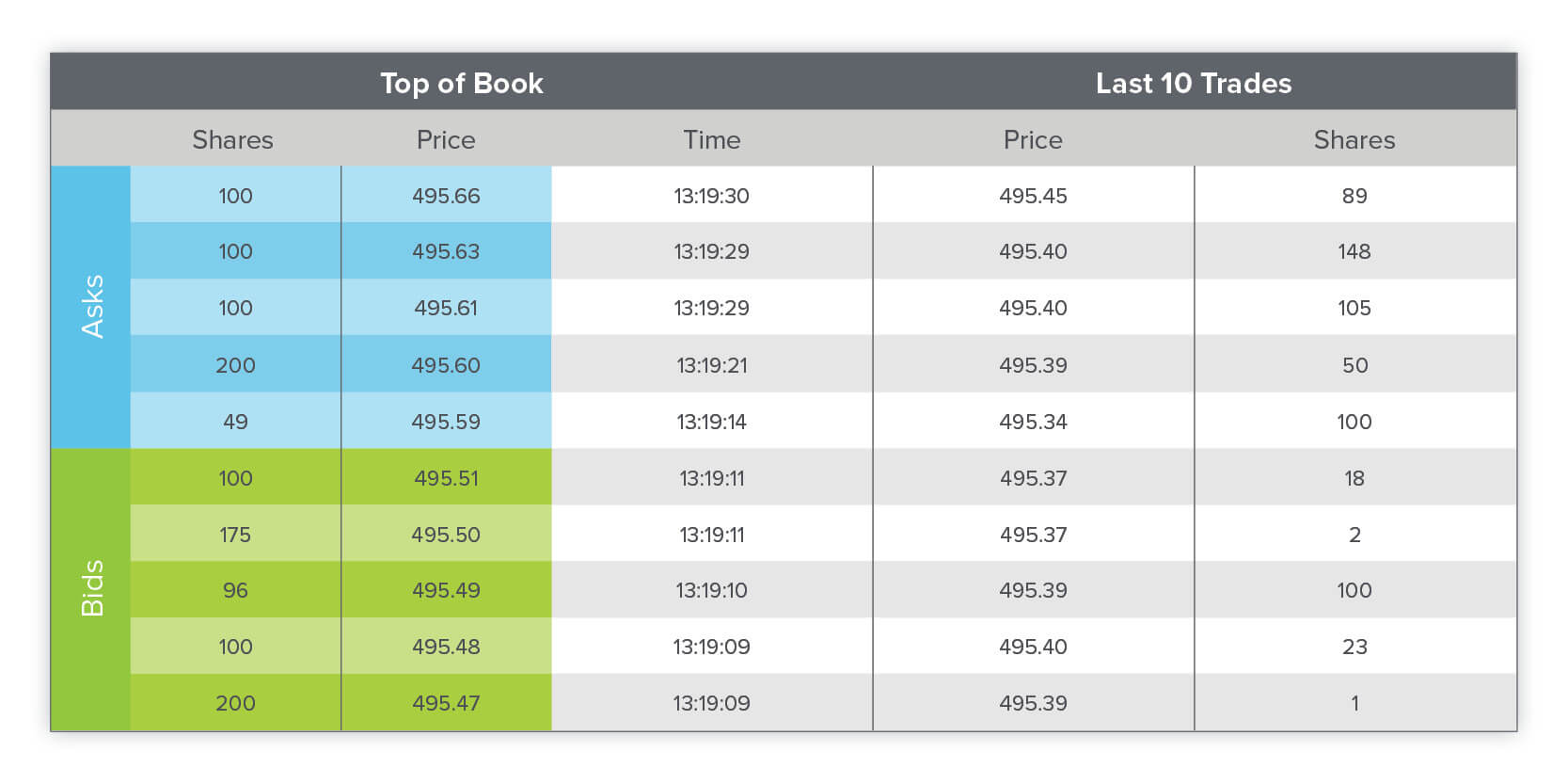

While the public markets conceptually represent a deep pool of buyers and sellers, sometimes that pool is shallower than meets the eye. For example, the quoted “price” of Apple stock represents the price at which the last trade was conducted, regardless of the number of shares that transacted. For Apple, as of the time of writing, a price of $495.45 was set from a trade of 89 shares, as you can see below. (As a reminder, none of this is investment advice; please see a16z.com/disclosures.)

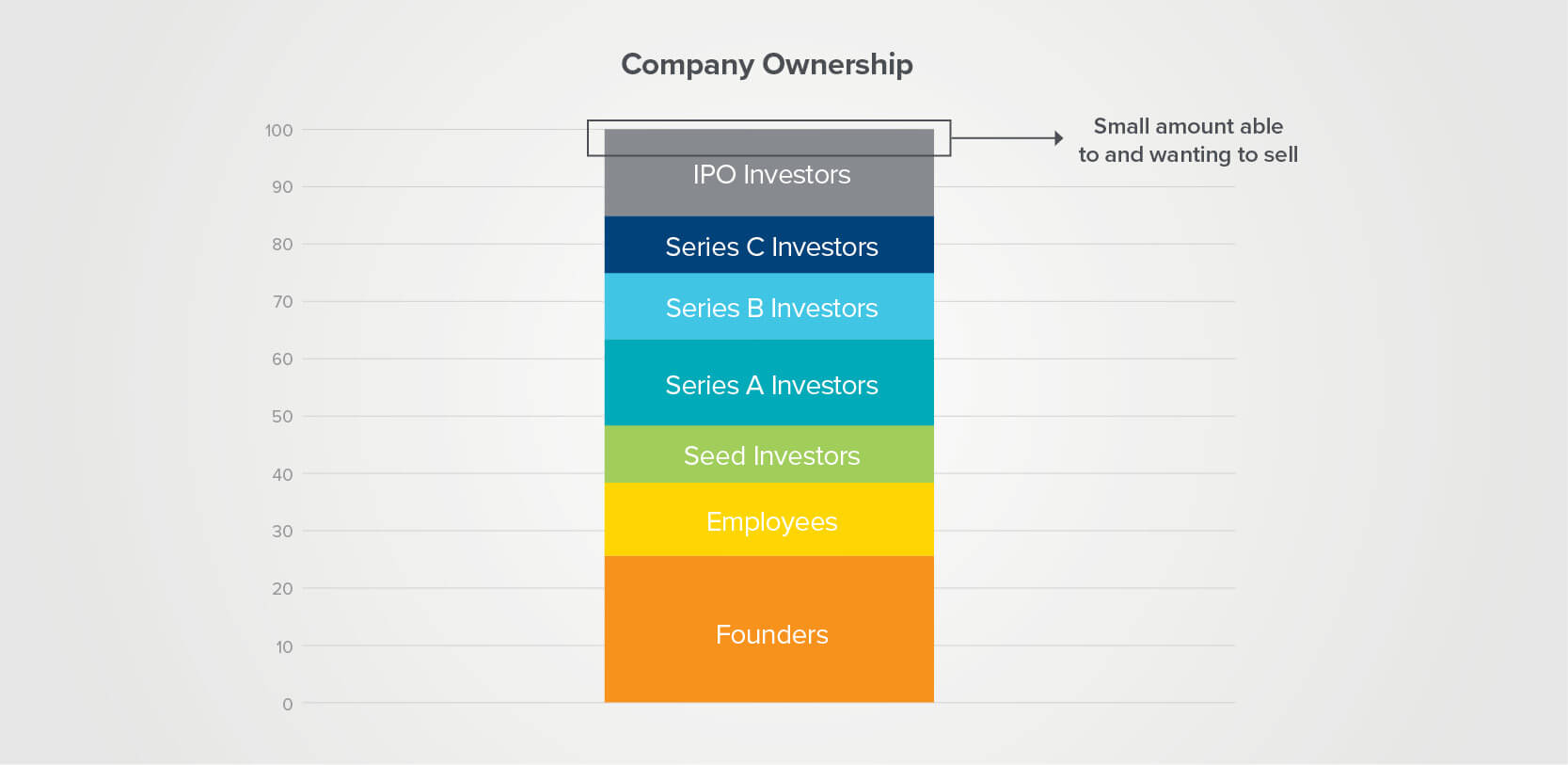

And although a company may have, say, 100 million shares outstanding, many of those shares might be “out of circulation,” so to speak — held by insiders (employees, founders, investors) who don’t want to sell or are unable to sell. The freely trading shares are called the “free float” and sometimes represent a miniscule percentage of the total shares of the company. As you’ll soon see, this is particularly true for an IPO, where perhaps 1 to 3 percent of the total shares are trading when the market first opens — a very small amount of available supply against a larger pool of demand. The price you see always represents the conditions of current demand and current supply, which are in a very unique (and volatile) state soon after a company goes public.

A price without a quantity is not a price

When Google announced its deal to acquire Fitbit, Fitbit stock was at $4 a share. But the deal was announced at $7.25 per share. Why didn’t Google just buy all of the shares at $4?

When Salesforce announced its intent to buy Tableau on June 10, 2019, the stock popped by 50 percent. Why didn’t Salesforce just buy all of the shares at the June 9th price?

The answer: in M&A, this would be called a “control premium,” but it’s really just an application of the classic economic laws of supply and demand. A new buyer who wants to buy every single share of stock (or more than 50 percent) represents a shift in the overall demand curve (more aggregate demand), therefore pushing the price up. The buyer typically knows they’ll have to pay more to convince 50 percent of shareholders to sell — that’s different from the price of a single share trading hands and isn’t relevant for a block.

The opposite of a control premium is a “block discount” — the lower price often required for a seller to move a large volume of stock. Just as a control premium represents a shift of the demand curve, a block discount — a large amount of shares offered for sale, all at once — represents a shift of the supply curve. Twilio just did a $1.25 billion share sale at a 11.2% file to offer discount and a 5.2% last trade discount because of the shift in the supply curve (increase in aggregate supply) of Twilio stock. Does that mean the bankers on the Twilio offering stole money from the company to give to their favorite institutional investor clients? No. Instead, they attempted to determine the market price for a single $1.25 billion share transaction; not surprisingly, that price is lower than that of a $5 million transaction.

Who buys stocks, anyway?

To understand the dynamics behind an IPO pop, it helps to understand the different types of investors in the stock market. There are effectively four kinds of investors, all of whom play a role in how and why things trade:

Much of the volume of the stock market is not net new buyers and sellers. While NYSE and NASDAQ are the two largest “stock exchanges,” there are dozens of other venues that collectively trade more volume, such as BATS and EDGX (owned by CBOE). High frequency trading firms and market makers often trade between venues — perhaps finding a partial bid on one exchange that is a penny above the ask on another exchange. The same “share” might be traded back and forth several times on its way to finding an investor who actually buys it to hold it. It’s not uncommon on a day of high volatility, such as the first day of trading for an IPO, to see the total volume of shares be a high multiple of the IPO offering size, but most of this represents arbitrage and gambling of the same shares back and forth.

How the traditional IPO process works

When a company goes public with a traditional IPO (and not a Direct Listing), it first sells stock to (primarily) institutional investors. It’s very similar to a VC fundraise, except a company might meet with hundreds of investors, most of them nowhere near Sand Hill Road (and of course the stock being sold will be publicly-tradable from day one, versus privately held in the case of a VC raise). The company prepares a presentation and hits the road (pre-Zoom!), hence the term “road show.”

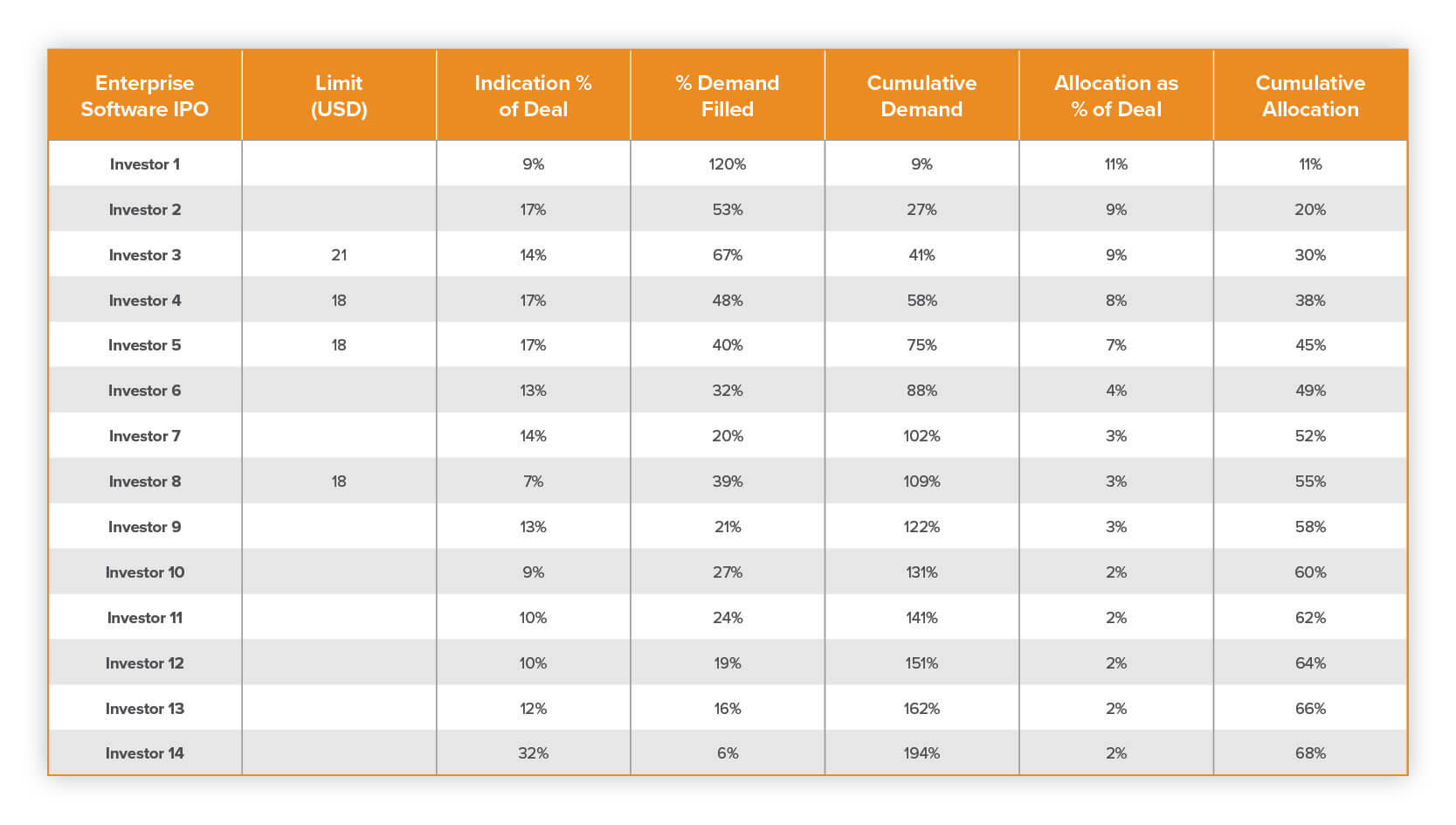

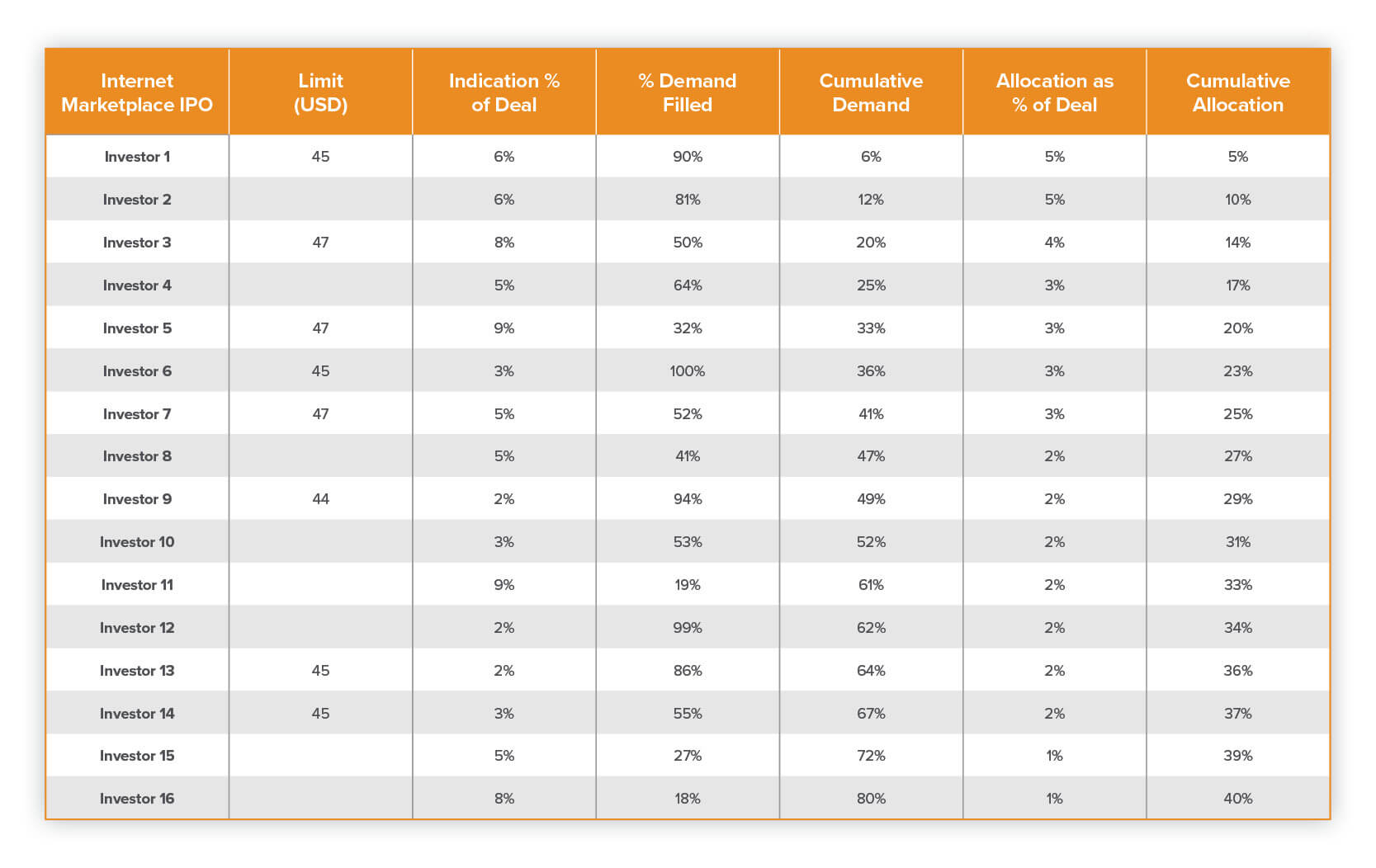

Investors place their own limit or market orders. You can see an actual order book from two recent IPOs below (investor names have been anonymized). Yes, it’s from Excel. But it’s important to distinguish the “input modality” (does it matter if a Limit order is placed over the phone, in a Chrome browser on an “order” page, via an email, or via carrier pigeon?) from the pricing process.

The ultimate price at which the IPO shares will be transacted is where the supply and demand cross, because in an institutional fundraise, all buyers must get the same price. Critics will say the price is “handpicked, more art than science” but whether this is done algorithmically or by hand, the same outcome happens. Venture backed companies can’t sell the same Series A shares at different prices at the same time to different buyers — rather, they pick one price and pick the investors at the same time. An IPO works the same way.

For example, if a company wants to raise $500M, and the orders show that it can raise $375 million at $18/share, but $700 million at $15 share, the offering will be priced at $15 and $500 million will be sold. That doesn’t mean that there aren’t investors who are willing to pay more than that — in fact, we know that there is $375 million of demand at $18 — but just that the market clearing price for the desired volume ($500 million) is $15. Naturally, we wouldn’t be surprised to see the stock trade up to $18 the next day in recognition of that demand, but that doesn’t impugn the decision to price the IPO at $15. This is reason #1 why the actual trading price of a stock might differ from its IPO price: supply and demand.

The selection of investors also mirrors that of a VC fundraise. If the company is lucky enough to have choices, it may choose to sell those shares to VCs it thinks may add value, be long-term holders, etc. In the case of an IPO, these tend to be longer term buy and hold investors (our “research” bucket from above), and are scored by bankers based on this proclivity to buy and hold. Think T Rowe Price, Fidelity, Ballie Gifford, et al.

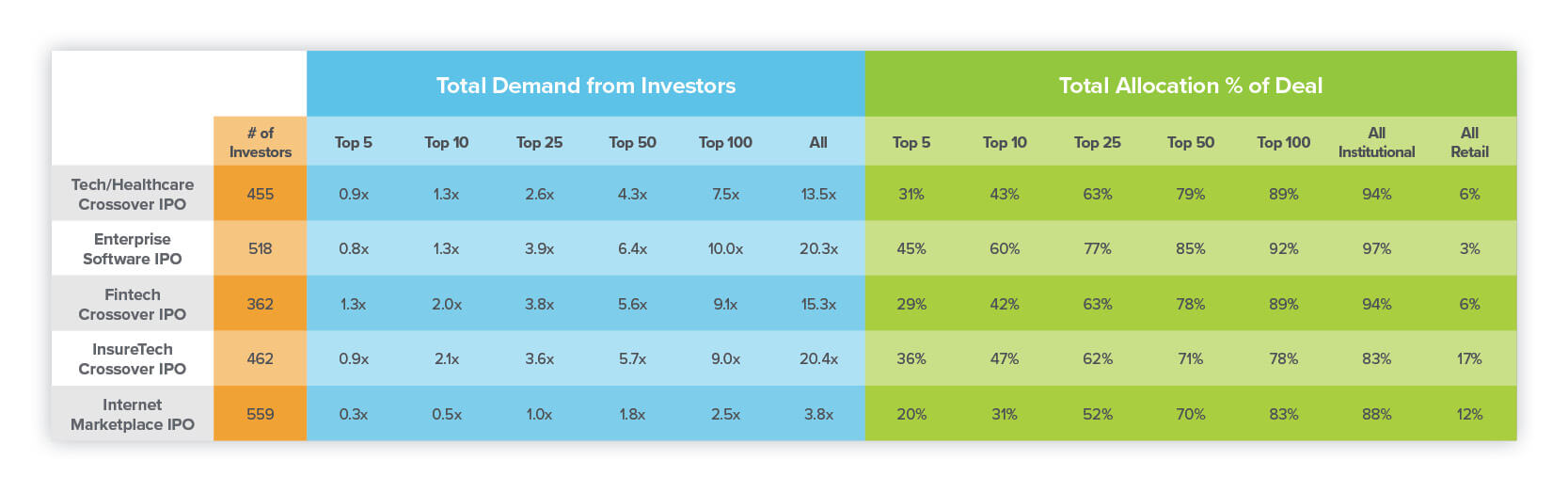

But, if the IPO market is “hot,” lots of other demand shows up — sometimes gamblers, sometimes arbitrageurs — all expecting to get less than their desired allocation. They know this, however, so they try to game the system by perhaps asking for 10x what they actually expect to get, which leads to the apparent “over-subscription.” The gamblers and arbitrageurs will invest in IPOs only if they think the price will instantly go up. This creates a certain “Market for Lemons” aspect to IPOs, because if IPOs stop popping, this part of the demand curve dries up, and certainly has before in a cyclical fashion that matches the disappearance of dramatic IPO pops. As a friend says, “IPOs pop because they pop.” The “winner’s curse” proves true here as well; if the gamblers and arbitrageurs get their orders filled anywhere near the volumes they ask for, look out below! This is reason #2 why the actual trading price of a stock may differ from its IPO price: the investor mix.

The following morning, the stock opens — or actually, it doesn’t! In order for there to be a trade, somebody has to sell, and underwriters will in fact intentionally allocate shares to investors who will “provide liquidity” by selling. Employees, pre-IPO investors, and founders are traditionally locked up (often for 6 months post the IPO) — an underwriter construct, not an SEC construct — so the only way for there to be a trade is to have one of the investors who bought the day before agree to sell. The only shares that can be traded are the same ones that the underwriter allocated the night before.

But many of the investors who bought last night don’t WANT to sell — even with a large pop, they have no interest in making a theoretically large profit (percentage wise) on a tiny position in a giant fund (a “100% pop” for a $25M position out of a $5B fund is meaningless…when selling $25M would likely depress the price anyway). This, in turn, drives the opening price higher — if a gambler wants to buy stock, and nobody is selling, the best way to pry shares loose is to increase the bid. And thus this is reason #3 why the actual trading price of a stock may differ from its IPO price: the need to incent an IPO buyer to in fact sell her shares at the open.

This “flip requirement” is a real phenomenon that shows an anachronism of the IPO, a key reason for the pop (only tiny supply flipped), and the reason why the pop doesn’t really matter — even though, without a doubt, free profits are stupidly being handed away to lucky IPO participants (but not necessarily at the company’s expense). Professor Reena Aggarwal at Georgetown has studied this extensively using DTC data and found that the median IPO shows 7.3% of IPO shares flipping, with the mean at 15%. More recent IPOs over the past 4 months have shown about 20% average flipping volume, which, though an imperfect measure, can be determined by comparing Order Book allocations to subsequent quarterly SEC 13F filings by the investors to whom an allocation was made. Much of this (due to the liquidity requirement/desire) happens in the first opening trade. Even though the flipping volume has increased, the float has decreased in the past decade; from 2002-2007 an average IPO was at 28% of total shares outstanding, but in 2019 that figure was at 16%, and for some of the hottest IPOs (e.g., Crowdstrike, Zoom, Datadog) less than 10%.

Source: Bloomberg. Charts provided herein are for informational purposes only and should not be relied upon when making any investment decision; past performance is no guarantee of future results.

But does the flip mean that the IPO was priced incorrectly? Not necessarily. To give a concrete example: assume a company sells 10 million shares at its IPO at $15/share. The next morning, 15% (1.5 million shares) are flipped at $25/share. Does that mean the company could have sold all 10 million shares in the IPO at $25/share? It’s an unprovable counterfactual, but the laws of economics — and the observed behavior of control premiums and block discounts — suggest very strongly to the contrary.

Think about it like a startup company that completes an oversubscribed Series A round to raise $10 million at a $40 million valuation, only to see a secondary transaction for $200,000 happen (due to the oversubscribed excitement!) at $70 million the next week. Does that mean the company could have raised $10 million at $70 million, and was ripped off by its Series A investors? Or that the secondary buyer even had $10 million, and not just $200,000, of demand? Of course not; the same is true in an IPO.

What else could we do within the construct of a traditional IPO to impact the amount of the pop? Remember those lockups we talked about earlier? Lockups are a contractual restriction on the volume of shares that are available for trading. Typically, lockups last for 6 months post-IPO and prevent any pre-IPO investors or shareholders (VCs, founders, employees) from selling or hedging any shares. The theory behind lockups is that we want the stock to “season” in the market and we worry that pre-IPO holders may have an informational advantage relative to new investors. The “seasoning” is intended to prevent them from taking advantage of this information to dump their shares on unsuspecting new investors.

What if we eased or got rid of lockups? Let’s say the lockup goes away, which would allow VCs and founders to sell stock immediately. Would this lower the pop and lower gambler/arbitrageur profits? Certainly, because now supply has been increased against the same demand (or even lower demand, forecasting a lower pop!). But how does this help the company? Why would the company be able to raise money at a higher price (or the “post-pop” price)? If anything, it might dramatically decrease “gambler and arbitrageur” interest in the company, since they see a lower chance of a pop. Who cares about the gamblers and arbitrageurs, you say, but this could very well lower the price that the company raises money at — to clear the whole block.

What about a Direct Listing?

A Direct Listing is an excellent mechanism if a company needs no capital and if its existing investors want more flexibility to exit the stock without the constraints of a lockup. It just “flips the switch” from private to public. So, unlike a traditional IPO, the company is not selling shares to anyone; rather, existing shareholders are instead selling some portion of the shares they own to (often) a new set of institutional investors. Why does this matter? One word: dilution. In a traditional IPO, the shares that the company is selling to public investors are newly created (so-called primary shares). That means if the company has 90 million shares already outstanding and wants to sell 10% of the company at the IPO, the total number of shares outstanding post-IPO is now 100 million (10 million IPO shares). So, if you are a founder who owned 20% of the company pre-IPO (18 million shares divided by 90 million), you now will own 18% as a result of the dilution (18 million shares divided by 100 million).

But what if a company needs capital, and doesn’t want to do a traditional IPO?

Many are proposing that the company execute an institutional fundraise on Sand Hill Road — with far fewer buyers than an IPO and hence less aggregate demand! — followed by a direct listing. Or raise convertible debt that converts at a fixed discount to the closing public price — from the relatively few firms that buy convertible debt at scale — followed by a direct listing. But both of these mechanisms aggregate less demand, and rather than being closer to a market price, are farther from it. They decrease the chance of a “pop” but they do nothing to aggregate more demand from more prospective buyers. Thus, this path is unlikely to materially reduce the potential dilution from a traditional IPO.

What about combining a direct listing with the ability for the company to sell primary shares? This is the latest news from NYSE and the SEC (NASDAQ likely soon to follow), and is a terrific development, but is a true gamble if the company is in need of significant capital. A company burning $200 million/year that raises $500 million in its “oversubscribed” IPO would not be in good shape if it raised only $100 million (20% of the IPO/flipped shares) instead at a higher price in the Direct Listing’s opening trade; as we’ve already shown, an order book often indicates demand at higher prices, just insufficient to clear the desired block. You can achieve no pop and likely a higher price, but potentially no solvency, either.

There’s also the game theory of this whole situation: If there’s no lock-up, and any number of shares can hit the market at any time, might I be overpaying for my stock right now? Should I bid at the opening? Maybe I should wait a little longer, since there’s no stabilization agent (underwriter) and I don’t want to be an idiot!

Hate the game, not the player: Strong stock performance helps build support for more liquidity

Did you ever wonder what it takes to join the S&P 500? It’s a quantitative and qualitative review process, dependent on market cap, free float, and volume. Or take a more inclusive index like the Russell 2000; FTSE Russell periodically reweights its indices, therefore forcing selling and buying of the underlying securities. A newly public company with a small float and a price that depends on small supply can sometimes punch above its weight class and land in a big index, which actually provides forced buying and more actual demand.

When investors and employees want to exit a public stock, if they all dump their shares at once, it will almost certainly depress the price. But given how important passive index investing is (accounting for the majority of inflows to the stock market), getting more “forced demand” is one way of absorbing ever-increasing amounts of supply. Having a strong, stable price and shareholder base brings more buyers to the stock, which allows for movement out of the stock with less volatility. It also allows for a nice reference point for a “secondary” institutional offering — also a block sale, typically at a discount — to bring even more money into the company or provide for an orderly exit of early shareholders.

What about the SPAC?

If the best fundraise (IPO included) aggregates as many potential buyers as possible to raise money at the highest price with the least dilution and lowest fees, it’s hard to understand how a SPAC represents an improvement against those constraints. When a SPAC merges with a target (“de-SPACs”), it’s tantamount to an IPO. The SPAC (already publicly traded, with lots of cash on its balance sheet) and the target company agree on a pre-money valuation for the target; the money sitting in the SPAC becomes the “money raised” (IPO equivalent) with typically a PIPE (Private Investment in Public Equity, a further institutional fundraise / large block sale) done at the same time. As an example, a $500M SPAC might merge with a private company, ascribing a $4.5B valuation to the private company, meaning a $5B post-money valuation of the combined entity. How do we know *this* is the fair price? Should a company meet with one SPAC? Two SPACs? Three SPACs or four? Where is the price discovery?

And while the fee structure of SPACs will likely change, right now it is indisputably a more expensive option with less price discovery. Bankers are paid 5%+ for taking the SPAC public; SPAC investors typically get warrants with their investment; the SPAC sponsor typically gets 20% (of the pre-merger value of the SPAC) for finding a target, so 2% in the above example; a banker is normally hired and paid to handle the merger; a mini-roadshow happens to get approval from the SPAC shareholders AND to potentially secure more cash in the form of a PIPE, for which a banker is also paid.

So what should be fixed?

While we think the focus on IPO pops is a sideshow, there are a number of true opportunities for improvement:

- A focus on aggregating more demand to better improve price discovery

- More innovation on blurring the lines behind public and private

- Improve supply/demand imbalances by reconsidering traditional lockups

The reason for aggregating more demand should be clear. Ideally, every IPO is plugged into consumer retail brokerage platforms (Schwab, Etrade, Robinhood, etc) — and can aggregate all retail demand, combined with a more open platform for reaching the longer tail of institutional investors and investment advisers, all aided by a more electronic roadshow that we’re seeing in the era of Covid. More demand equals better price discovery equals a higher price with less dilution at the block sale.

Why blur the lines between public and private? One challenge for institutional investors is how much to bid on an IPO. They can look at comparables in the public market, they can look at the company’s financials, and they can look at the last (stale) price from a private round. They don’t tend to care about the IPO pop sideshow, given the low supply dynamics that drive that price. But imagine a world where leading up to an IPO, organized secondaries — from the same (expanded) pool of buyers — happen every quarter. There will hopefully be less disconnect between private prices and public prices and more of the cap table will already be in the hands of public, research-oriented investors. Again, less asymmetric information between parties will improve price discovery, reducing potential dilution (not to mention fees, since bankers get paid as a % of the size of the IPO). This is part of what is promising about Carta, which started off as a cap table management solution for private companies, and their CartaX exchange.

Finally, we talked about the traditional 6-month lockup and its impact on pricing by artificially constraining the supply of stock. In many ways, it’s an anachronism of a market of yesteryear in which information dissemination was more analog and thus the seasoning of trading took more time.

An IPO, SPAC, or Direct Listing can each make sense in the right context for the right company, and each will hopefully improve. The handy rule of thumb is: if you need money, an IPO, for all its flaws, makes the most sense and is probably the best option; if you don’t, a Direct Listing may be preferable; if you need money, speed, and certainty, a SPAC may be best.

But hopefully everyone involved in the current IPO debate can agree that the best fundraise happens at the highest price the market will bear with the least dilution and lowest fees, not where 89 shares of stock trade 3 hours later. Focusing on aggregating the most demand, blurring the lines between private and public, decreasing fees, and eliminating anachronistic restrictions — that’s where founders thinking about being public, and capital markets innovators, should set their sights.

Thanks to Alex Immerman, Carl Chiou, Daniel Tay, and many others for reading drafts.