This first appeared in the monthly a16z fintech newsletter. Subscribe to stay on top of the latest fintech news.

IN THIS EDITION

- Fintech products ease more Americans into the stock market

- In defense of the IPO, and how to improve it

- What’s inside your (mobile) bank?

- Reimagining the debit card

- Better models for SMB lending

Want more a16z?

Sign up to get our best articles, latest podcasts, and news on our investments emailed to you.

Thanks for signing up.

Fintech products ease more Americans into the stock market

Anish AcharyaThe percentage of Americans who own stocks is falling, according to the Wall Street Journal: only 55 percent own stocks today, compared to 67 percent in 2002. This trend is worrisome because investing in public markets has traditionally been one of the most important wealth creation mechanisms in the U.S., in addition to home ownership. Understanding this, historically, the government has enacted a number of policies to improve access to public markets and home ownership, such as many changes to the tax code and legislation that famously made 401(k)s opt-out instead of opt-in (lesson: intelligent defaults can change the world). How do we ensure a new generation of Americans can participate in the wealth creation that public market investing can bring?

Though there is no silver bullet, we are seeing a number of promising approaches catalyzed by fintech products. Among the most interesting is Stash’s “stock back” program, which is essentially an alternative form of rewards. Individuals who pay with their Stash debit card at a given merchant (say, Starbucks) receive fractional shares of that merchant’s stock as a reward for spending. This is clever for a number of reasons. One, it compounds the idea that consumers “vote” with their dollars, as the places you spend money then become the companies you’re an investor in. Second, typical rewards cards provide a narrow benefit – they’re most often only available to prime consumers and are usually subject to a great deal of breakage (now more than ever, when most folks aren’t traveling). This runs contrary to the appreciation that is typically expected of a buy-and-hold investment strategy. Finally, Stash’s program gives consumers who might not otherwise be investors an opportunity to participate in the market and learn about its opportunities (and risks!), which is hugely important from a financial inclusion standpoint.

While the feature itself is interesting, the underlying capabilities that enable it are even more so. The rise of fractional shares, turnkey brokerage infrastructure, and the broad trend towards zero dollar trading have made a program like this economically viable. That’s becoming increasingly common for non prime-focused products like Cash App or Stash. Lastly, through the rise of products like Robinhood and Public.com, investing is becoming a cultural norm for Gen Y and Gen Z. These products encourage all individuals to participate in and have a point of view on investing, rather than operating under the assumption that it’s strictly for the wealthy.

As the national dialogue on income equality and financial inclusion continues, I’m encouraged to see technology companies pave the way for the consumers that have often been excluded. Whether it’s Yotta encouraging emergency savings accounts, Dave.com providing overdraft protection, or Stash enabling broad participation in public market investing, I believe that the private sector could be an inflection point for the country’s financial health – and that fintechs will lead the way.

- The Most Human Technology Ever Made Anish Acharya

- What Happens to Design After AI? John Maeda, Paul Bakaus, and Anish Acharya

- What’s Next for Consumer AI? | Josh Elman Joins a16z Josh Elman and Anish Acharya

- Building AI Agents for Enterprise Operations Pablo Palafox, Luis Paarup, Anish Acharya, and Olivia Moore

- Investing in Ethos Anish Acharya, James da Costa, and Olivia Moore

In defense of the IPO, and how to improve it

Alex RampellThere’s a popular narrative that evil investment bankers are intentionally underpricing traditional IPOs to steal from companies, lining banker pockets and those of their fatcat Wall Street clients. The proof is seemingly obvious: IPOs are 50x oversubscribed! The price explodes by 50 to 200 percent mere hours after the IPO, representing hundreds of millions of dollars in “money left on the table”! Proponents of this view believe the Direct Listing, or now the SPAC, is the panacea for these woes.

An IPO is far from perfect, but this narrative is almost completely false. To understand why first requires taking apart the IPO process, how stock markets work, and what the “price” of a stock means. You can’t fix or improve something without understanding how it works and what’s broken.

Read the full post

- Investing in Probook Alex Rampell, David Haber, Olivia Moore, and Seema Amble

- Investing in Town Alex Rampell and Justine Moore

- Investing in Lassie Alex Rampell and Olivia Moore

- Investing in Stitch Alex Rampell and James da Costa

- Ben Horowitz on AI Infrastructure, Economics and The New Laws of Software Ben Horowitz and Alex Rampell

What’s inside your (mobile) bank?

Angela StrangeIt’s intuitive that digital-first banks would gain market share at a time when most of us are especially reluctant to visit public places. For customers who typically might not have sought out a “neobank,” COVID has provided the extra push to get new account openers to consider a challenger brand. What’s less intuitive, however, is that the biggest winners of the past six months, in terms of new accounts opened, have been megabanks like Chase, Bank of America, and Wells Fargo. For consumers scarred by the 2008 financial crisis, those brands may be perceived as “safer” than fintech alternatives, but that doesn’t nearly explain the sharp increase in share of new accounts.

SOURCE: CORNERSTONE ADVISORS. CHARTS PROVIDED HEREIN ARE FOR INFORMATIONAL PURPOSES AND SHOULD NOT BE RELIED UPON WHEN MAKING ANY INVESTMENT DECISION

SOURCE: CORNERSTONE ADVISORS. CHARTS PROVIDED HEREIN ARE FOR INFORMATIONAL PURPOSES AND SHOULD NOT BE RELIED UPON WHEN MAKING ANY INVESTMENT DECISION

Mobile banking used to be accepted as a less robust experience of what one could do in a branch. You could check your balance on the go and perhaps pay a bill, but anything more complex required a visit to the physical location – or at least the desktop web version. Now that many consumers want to do all of their banking online, the pressure on banks to offer them an equal, if not better, mobile experience is high. Still, it’s only the largest of banks – here, defined as banks with over $10 billion in assets – that would even come close to being considered “full-featured” from a mobile banking perspective. And that’s to say nothing of consumer-friendly features offered by some of the newer entrants, such as overdraft protection.

SOURCE: S&P GLOBAL

So why the large gap in feature sets? The biggest challenge is that most banks are reliant on third-party technology vendors, such as FIS, FiServ, and Jack Henry. And while the newest versions of some of these cores might provide a more modern experience, many banks are “stuck” on older versions not compatible with newer modules. To state the obvious, if something is not on your third-party vendor’s roadmap, then it’s not on yours.

Larger third-party tech players are trying to evolve their models. FIS, for example, recently launched a subscription model to reduce the financial burden on banks, as well as to provide more modularity. But given the complexity of these core banking systems and the speed at which consumers are requiring mobile first-financial services, it no longer makes sense for one vendor to be a one-stop shop for all things.

Thus, some newer core providers (such as Thought Machine) focus on a few key aspects – checking and savings accounts, lending – then provide APIs into their systems so that additional solutions built by other vendors can plug in. For banks that are hesitant to “rip and replace,” but who still want to launch new products or to improve the operational efficiency of existing systems, there are players like Moov.io. Moov can provide the connective tissue (say, to port data into a new, flexible ledger) or the APIs for more reliable ACH payments, based on their open source libraries. This could allow banks to use a new core system for a new product, or to gradually improve their legacy infrastructure.

There may be thousands of banks in the U.S., but with the exception of the “megabanks,” they all run on a handful of infrastructure providers. That’s why we, as consumers, generally have the same frustrations with the user experience!

But imagine a future where banks are able to choose solutions from best-of-breed providers that work together seamlessly, while also maintaining the ability to develop their own custom solutions by leveraging modern APIs. This would benefit newer entrants, who will be able to build solutions faster, as well as existing banks, who will be able to provide more modern experiences to their customers – and perhaps come closer to leveling the playing field for smaller and community banks competing with far larger peers. But most of all, it will benefit us as consumers. Even post pandemic, we will be able to accomplish all of our banking needs by just using our thumbs.

- The Fintech Playbook for Latin America Santiago Suarez, Gabriel Vasquez, and Angela Strange

- Stablecoins, AI Agents, and The Future of Global Banking Dileep Thazhmon and Angela Strange

- Everything, Everywhere is Compliance James da Costa and Angela Strange

- From Copilots to Agents: Rebuilding the Company Around AI Angela Strange, Gabriel Vasquez, and Carlos García Ottati

- Big Ideas 2026: The Enterprise Orchestration Layer Seema Amble, Angela Strange, Alex Immerman, and David Haber

Reimagining the debit card

It’s a well-known fact that Americans prefer to use debit cards over credit cards. In fact, according to a 2018 study by TSYS, approximately 54 percent of Americans prefer to use debit cards, while only 26 percent prefer credit cards. According to a Fed payments study, debit card transactions were almost double that of credit cards in 2018: 87 billion debit card payments, versus 45 billion credit card payments.

But that consumer preference comes at a cost. One of the many benefits of a credit card is that it allows consumers to build up their credit scores as they make payments, as well as earn rewards for purchases. Meanwhile, rewards for debit cards were discontinued by many banks after the 2008 financial crisis. What this means is that consumers paying with a credit card are effectively getting a 2 percent rebate on all purchases, depending on their credit card reward program. (Put another way, those using a debit card are paying 2 percent more for everything they buy.)

However, credit cards are not without pitfalls. Most glaringly, more than half of Americans have credit card debt, resulting in over $1 trillion in consumer credit card debt in the U.S. Banks often charge more than 20 percent interest rates on credit cards, and the fees associated with late or overdraft fees is a huge market (worth more than $34 billion in 2017). Given skewed bank credit and underwriting models, near-prime and subprime customers are much less likely to be approved for credit cards, which means credit access is often limited to higher earning individuals. There’s also an element of consumer trust (or lack thereof) in banks – many consumers are wary of bank credit cards, often associated with fees and other “gotcha” expenses.

Thus, one of the most interesting trends we’re seeing is consumer fintechs embracing and supercharging the debit card to help Americans. Chime’s debit card launched with a no-fee guarantee to build trust. It now also offers 1 percent APY on savings, which is one way to offset credit card appeal. Last week, the mobile bank Current launched rewards – previously, a major draw of credit cards – so its users can build point equity with each debit card swipe. Other companies are leveraging financial products that act like debit cards, such as secured credit cards or charge cards, to help consumers build credit. When it comes to credit, millions of Americans have been burned or snubbed by traditional banks. Fintechs are using this opportunity to make debit more powerful. We’re excited to see more fintechs come up with innovative products and features that make the debit card work for everyone.

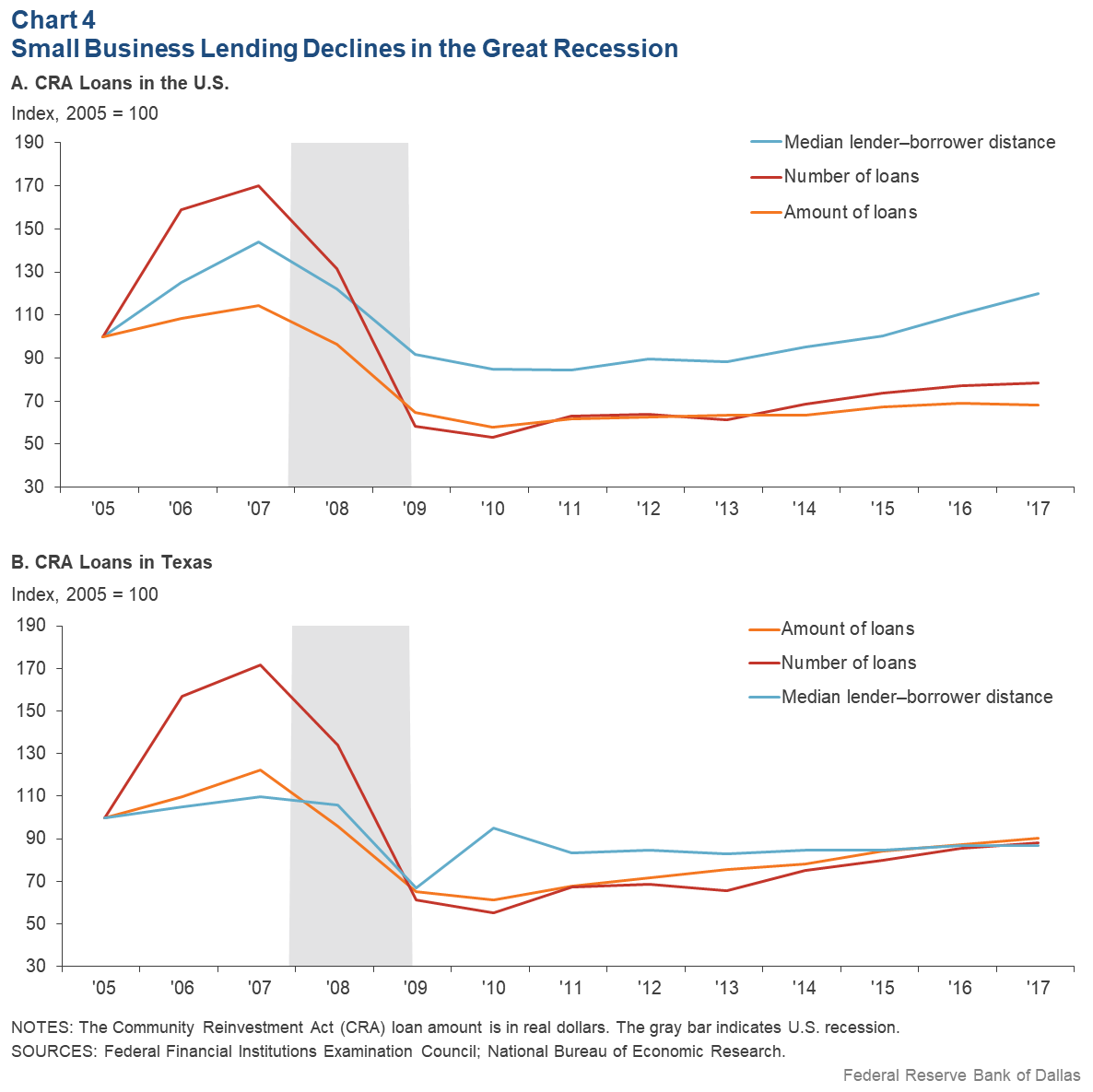

Better models for SMB lending

Seema AmbleCOVID-19 has prompted a scramble in the world of online SMB lending, as delinquencies pile up. But the resulting shift is correcting long-standing issues in small business lending around distribution and risk selection. In the past month, Amex announced it would acquire Kabbage for up to $850 million, while Enova announced it would acquire OnDeck for $90 million; both acquisitions were facing distress due to COVID-related delinquencies. Meanwhile, Stripe Capital launched lending partnerships with Lightspeed for its point of sale (POS) customers, as well as with the home service software provider Jobber. While COVID may have been a catalyst, these events reflect a key shift in online SMB lending.

Traditionally, SMB loans were most commonly offered by community banks. The application process was often painful, due to the paperwork required and the time to a credit decision. Around 15 years ago, SMB online marketplace lenders like Kabbage, OnDeck, and Funding Circle emerged, digitizing the application process and newly connecting into data sources like Quickbooks. Then COVID-19 hit, hurting sales for many SMBs. Since the median small business had less than a month of cash reserves, delinquencies for online lenders like OnDeck increased. For many small businesses, PPP loans helped ease the burden, but didn’t cover all expenses. OnDeck’s delinquency rate went from 11 percent at the end of December to 45 percent by April, and the company was forced to increase its reserve for credit losses and tap an existing credit line.

But COVID only accelerated the impact of a few pre-existing structural issues in online SMB lending around distribution, risk selection, and diversification. Scaling distribution for SMB software is difficult in general, but particularly for lending. The cost of originating and servicing small loans is comparable to larger loans, but the interest and fee revenue is far less. Plus, the failure rate of SMBs is already high – one in five SMBs go out of business in the first year. That rate is higher still for SMBs in need of loans, which has made the unit economics for SMB lending historically difficult. OnDeck struggled with this, as evidenced by the low LTV to CAC (which had halved, pre-COVID from 3Q 2019).

In addition, online lenders have historically attracted riskier consumers. Thirty-two percent of online lender applicants chose their lender because they were denied by others, namely community banks.

Finally, the lack of diversification is an achilles heel. SMB loan originations typically drop precipitously during recessions, but banks usually don’t go out of business as a result, partly because SMB lending is just one portion of their business. However, marketplace lenders that didn’t have the base of deposits that banks had, like OnDeck, saw their balance sheet – and loan-funding investors – disappear quickly.

Going forward, we’ll see two models prevail, both of which will offer SMB lending through an existing customer relationship:

1) Embedded loans, in which lending is tied to software that the SMB customer already uses as an operating system. This is similar to the Stripe models launched this month. Here, home services businesses manage their day-to-day clientele via Jobber and merchants manage their retail businesses via Lightspeed’s point-of-sale.

2) The “bank” model (with a license or not), in which lending is offered in addition to a set of financial products, often starting with a high engagement product like payments or a checking account. Square, for example, started with its POS payments product and later layered in lending.

First off, by embedding lending within a software product like Jobber or with payment processing like Lightspeed, it removes the cost of acquisition completely. The customer is already engaged on a daily basis, making the lender top-of-mind and highly visible. Offering lending first, then trying to add on high engagement products is more difficult. In fact, Kabbage added checking accounts, an insights product, and payment processing. However, the majority of its business is still lending.

Additionally, Stripe and Square avoid the adverse selection issues that online lenders typically face by pre-selecting who they show a loan offer to (there is no direct application for the loan). Between Jobber’s customer information and Stripe’s transaction data, they know their customers and their spending patterns. This model also incorporates additional data points like inventory management that can help measure risk, something a marketplace lender wouldn’t be able to do. This also allows them to avoid the negative customer experience of denying customers a loan.

For now, lending also appears to be trending towards smaller loans of a shorter duration, which are lower risk than those offered by SMB marketplace lenders like OnDeck or Funding Circle. Stripe, Square, and others have been offering the merchant cash advance (MCA) model and other smaller loans. An MCA is a lump-sum loan or “advance,” in exchange for which the merchant automatically pays a percentage of sales, typically daily, until the loan is repaid (in addition to a fee instead of typical interest payments). Effectively, the merchant is selling their future card sales at a discount. OnDeck offered revolving lines of credit and term loans; the average profile was approximately $55,000 and 13 months (for 2019). By comparison, pre-COVID, Square Capital’s average loan was less than $10,000, and less than 9 months in duration. Smaller loans can also help provide data points to help assess customer risk prior to offering larger loans later on.

The new generation of lending models have not focused on providing longer duration and larger size “growth capital” loans to buy things like equipment and facilities yet, although Stripe eventually intends to through its partnership with Jobber. Traditionally, community banks have specialized in small business lending because they rely on personal relations and face-to-face interactions to collect more “soft” information to assist underwriting. As software and payment providers increasingly collect more data on the customer, they’ll likely be able to understand and underwrite bigger risks, better than community banks.

Finally, in terms of diversification, it’s unlikely any lending model can entirely protect itself against the risk of SMBs going out of business in a downturn. But when lending is a smaller part of the overall business, a company like Square can turn off its lending business in a downturn, as it did in March to focus on distributing PPP loans. As a bank, Square will also now have the deposit base as a funding source.

So, while it may seem like SMB online lending has been collapsing, it’s really being reborn. These new lending models combine the streamlined application process and faster approval that marketplace lenders offer with an economically-viable business model that hopefully weathers the next storm.

- Is Software Losing Its Head? Seema Amble, Elena Burger, and Steven Sinofsky

- Investing in Probook Alex Rampell, David Haber, Olivia Moore, and Seema Amble

- Is Software Losing Its Head? Seema Amble

- Investing in Tessera Labs Seema Amble, Eric Zhou, and Joe Schmidt

- Why the World Still Runs on SAP Eric Zhou and Seema Amble

More from the a16z fintech team

Fintech Scales Vertical SaaS

Today, the majority of SaaS company revenue comes from subscription fees. With fintech products and services, the future may look very different.

By Kristina Shen, Kimberly Tan, Seema Amble, and Angela Strange

Online Learning and the Ed Tech Debate

The research behind the Zoom classroom and tech’s potential in everything from improving curriculum to democratizing access to funding higher education.

By David Deming (Harvard University), Josh Kim (Dartmouth College), Connie Chan, and Lauren Murrow

Fintech Pursues Gen Z

Plus: How COVID-19 hit big banks; new credit builder products; an emerging model for high-yield savings, and more.

By Angela Strange, Rex Salisbury, Anish Acharya, Seema Amble, and Matthieu Hafemeister

Big Fintech Goes Global

Plus: A contrarian take on recovery prospects; the controversy behind the Hertz stock snafu, and more.

–Anish Acharya, Seema Amble, Alex Rampell, Rex Salisbury, and Matthieu Hafemeister

Subscribe to get the a16z fintech newsletter in your inbox.

{kind=link}