A dynamic new wave of digital-first companies has emerged, driven by a significant decrease in the cost of building a minimal viable venture and further propelled by recent advancements in Generative AI. Founders can now quickly build chatbots/companions, education tools, image generation tools, lightweight SaaS apps, and games for customers around the world. Selling these digital products globally, however, is not yet straightforward.

Founders currently need to stitch together multiple complex tools including payment platforms, support tools, tax calculation and remittance services, marketing and retention products, and more in order to support the regulatory, currency, and language requirements that come with selling in many geographies. A simpler option is starting to emerge: companies can sell through a Merchant of Record (MOR) platform that abstracts away this complexity and enables founders to fully focus on building their products.

In this post, we cover what’s required to sell digital products vs. physical products, the current landscape for entrepreneurs looking to sell their digital-first products globally, why an MOR platform can simplify the global selling experience, and how platforms can get in front of the right customers and build long-term value.

How we got here

The 2010s saw an explosion of direct-to-consumer online businesses, driven by several factors: the ubiquity of the smartphone, the ability to reach customers via social media, services like AWS that negated the need to buy/rack servers, and perhaps most importantly, operating systems like Shopify that greatly simplified selling physical products. Creative, smart, but non-technical entrepreneurs could spin up a website, collect payments (via Stripe), and coordinate logistics all from one platform.

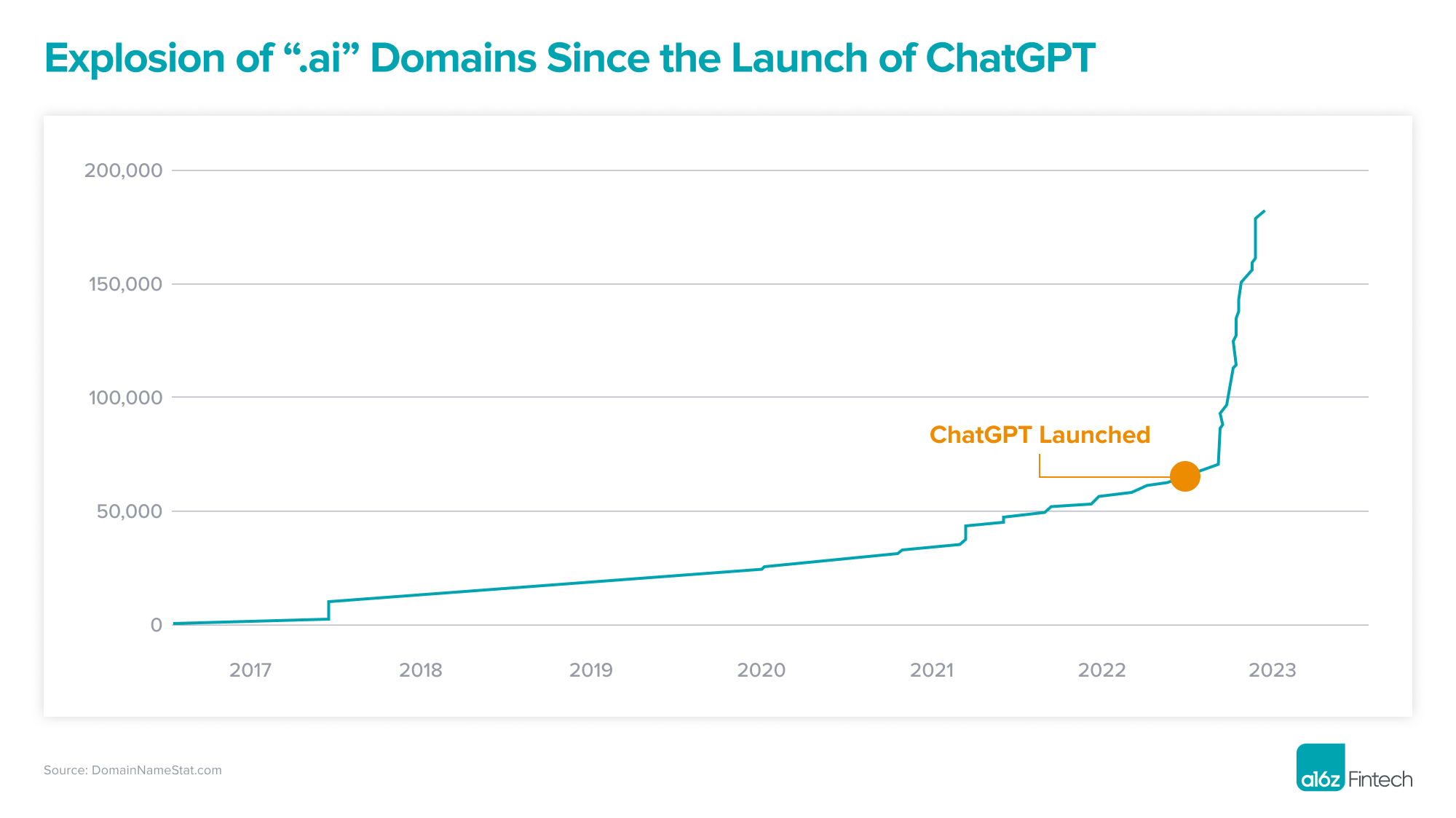

This next wave of digital-first companies has been building steadily over the years. It has accelerated with leaps in Generative AI that captured developer imagination, particularly with the launch of ChatGPT in November 2022. The products these entrepreneurs are building are digital in nature and can be easily sold around the world to anyone with an internet connection (no shipping necessary!).

Existing e-commerce platforms focus almost exclusively on physical products and usually serve customers selling in one primary geography. They lack the complete feature set these digital-first products require:

- Global vs. single geography: Selling in multiple geographies dramatically increases complexity and can require setting up merchant accounts in multiple geographies, pay-in and pay-out orchestration in local currencies, tax remittance, and more.

- Digital vs. physical products: Selling digital products requires features that physical products do not including metered billing, subscriptions, license key management, and retention and upselling tools.

Thus, similar to how Shopify and Stripe enabled the D2C, physical e-commerce product wave, we believe there is an opportunity for new platform companies to emerge and empower this wave of digital-first, AI-enabled, default global companies.

The landscape today

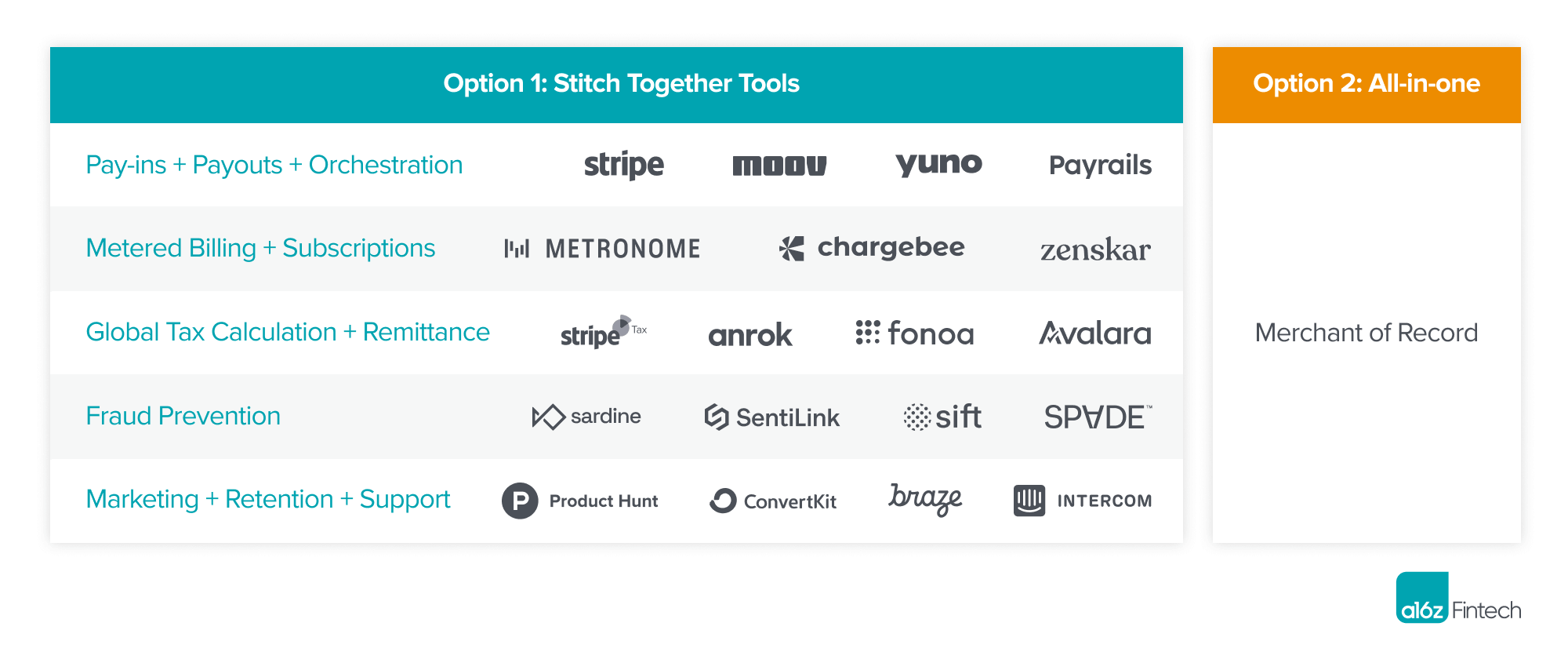

There are currently two primary paths for entrepreneurs to sell their digital-first products globally:

- Stitch together best-in-class point solutions for maximum flexibility from a technical and pricing perspective

- Use a Merchant of Record that abstracts away the complexity of stitching together tools with an all-in-one platform

To most effectively sell software/digital products globally, founders will require:

- Pay-In + Payout + Orchestration: To accept payments from customers around the world in their preferred (often local) payment method. This can require setting up merchant accounts in different countries, plugging into payment gateways, and orchestrating between them.

- Metered Billing & Subscriptions: To maximize revenue potential by charging customers based on their usage via metered/usage-based billing platforms and managing customer subscriptions.

- Global Tax Calculation + Remittance: To calculate, file, and remit sales tax in jurisdictions where customers are located and where threshold amounts have been reached (i.e. when revenue exceeds a specific dollar amount in a given geography a company is selling in) in compliance with tax laws.

- Fraud Prevention: To prevent fraud globally, by either plugging into best-in-class point solutions or fraud orchestration platforms, without increasing customer friction.

- Marketing + Retention + Support: To attract, retain, and upsell customers from around the world, while providing product and payment support to minimize churn.

While larger companies can build processes internally for this, for new startups, the integration, coordination, and upkeep of a variety of vendors can take developers away from their highest value use of time: building their product.

Enter the Merchant of Record

A Merchant of Record (MOR) is an entity that accepts payments on behalf of a business such as the Apple App Store for mobile apps, as we have written about previously. The MOR is authorized and held liable for these transactions, which includes processing payments, managing payment processor fees, managing refunds and chargebacks, providing billing-related customer support, and ensuring businesses remain compliant with global tax regulations. The Merchant of Record gains a direct, standalone relationship with the end customer–the MOR’s name is what a customer sees on their bank statement for instance.

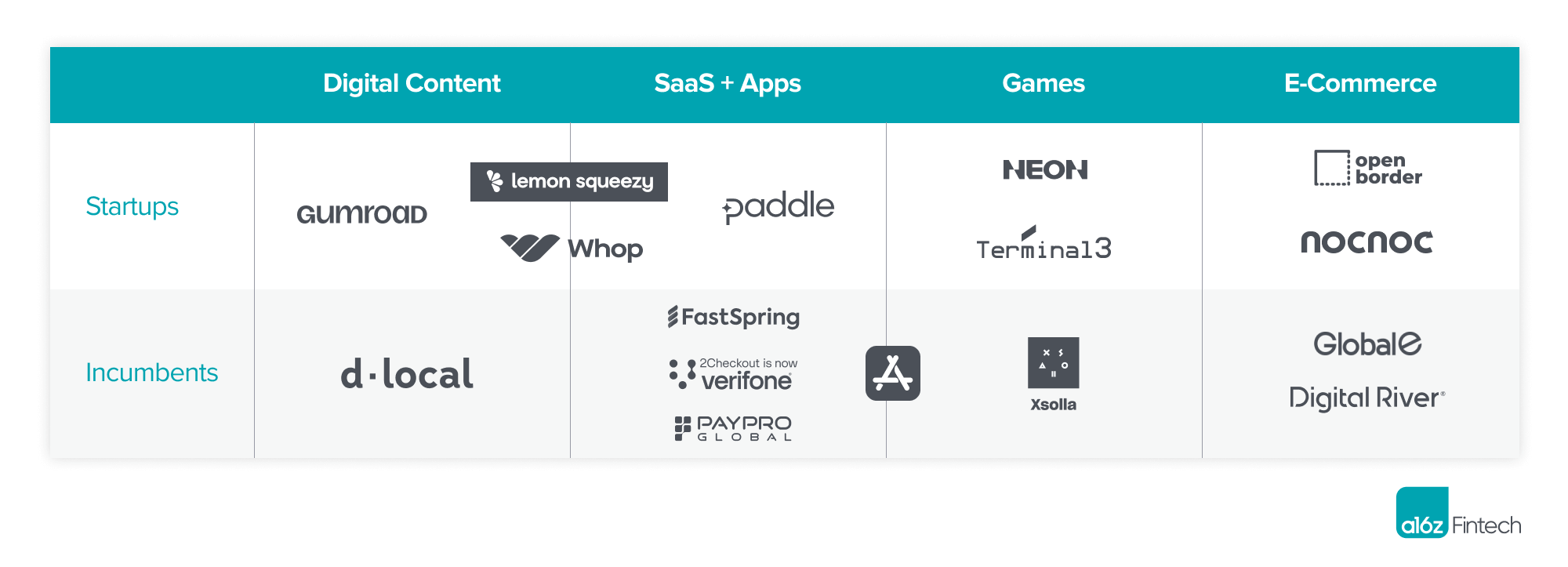

Here’s a non-exhaustive list of emerging Merchant of Record platforms, as well as several incumbents across product categories:

Beyond making the selling experience for merchants simpler, MOR platforms also have an interesting opportunity to create network effects. The MOR controls the final customer experience at the point of checkout, and thus the MOR can cross-sell products from other merchants on its platform. For example, Digital River was successful in creating network effects in the ‘90s, not only by cross-selling SKUs from other merchants at the point of checkout, but also a broader set of financial services products (e.g., insurance for electronics).

Potential for developer-first distribution

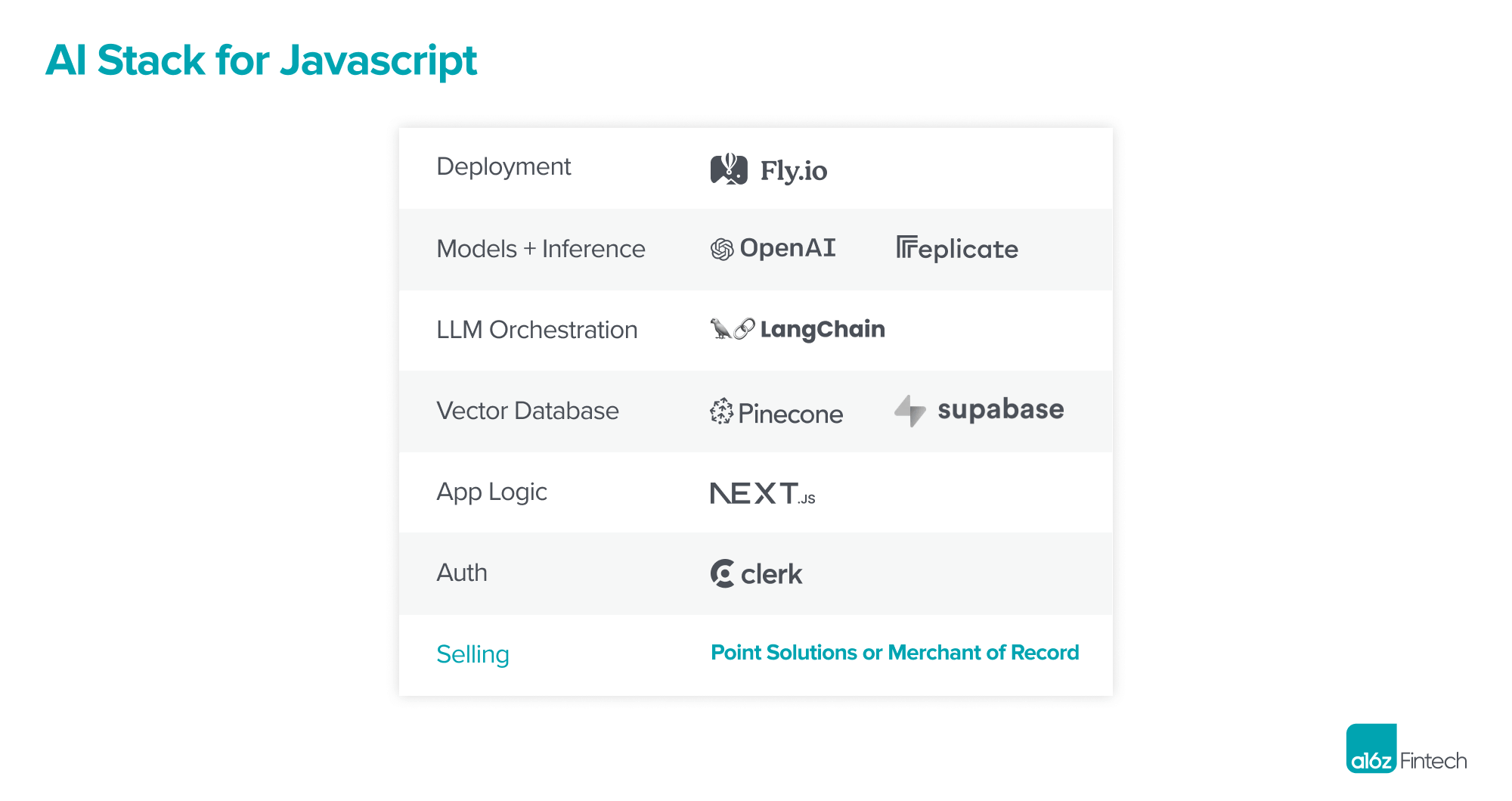

Unlike in the physical-product wave, this digital-product wave is mostly being led by technical founders—opening the opportunity for a developer-first platform (i.e., APIs with great documentation) and community-driven developer distribution. We believe there is an opportunity for point solutions or MORs to become the standard for a “Selling” function in the emerging javascript stack to build AI-based applications. (Github repository here!)

What’s next?

Just as merchants who started their businesses on Shopify went from startups to household names, we imagine the same will happen for this next-generation of digital, AI-enabled, default global companies. These companies will need simpler platforms, whether they be point solutions or Merchant of Record ones, to reach their global customer base. If you’re building here we’d love to talk to you.