Exit options for startups, and their investors, were relatively straightforward for years — the companies could either go public or be acquired. Now the menu of possible options has significantly expanded, as Direct Listings and SPACs have also become tested-and-proven pathways to the public markets.

All these choices add complexity for founders and investors, and subtle implications for valuation, dilution of shares, liquidity, and more. So we outline the available exit paths for founders, as well as the implications unique to each option.

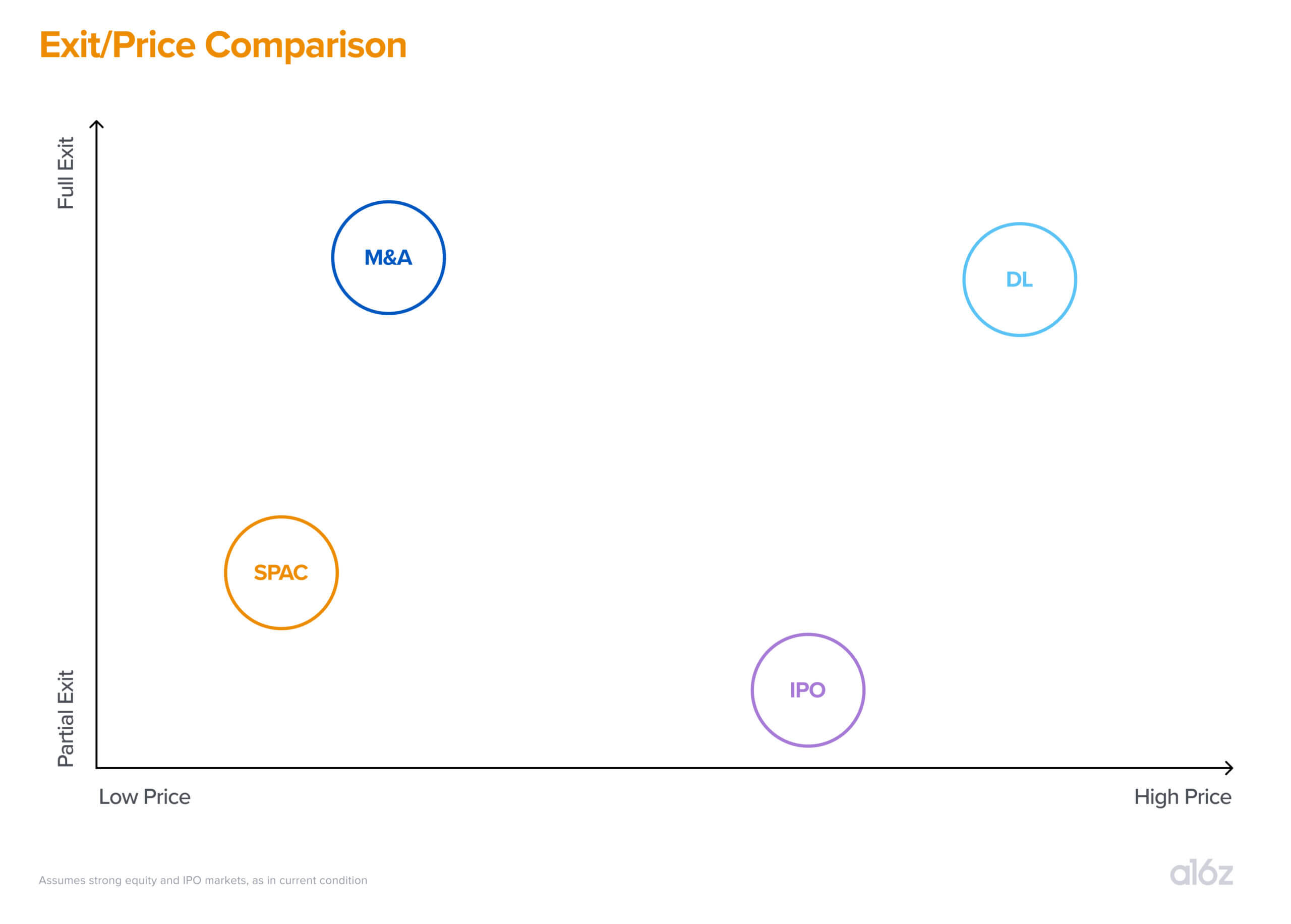

But to begin, the below chart illustrates how the four main options compare; we’ll explain the dynamics behind each.

Traditional IPOs

The IPO or initial public offering is the oldest, traditional option for “going public.” It involves a company issuing new shares as a way to raise new capital, and sometimes selling existing shares from founders, investors, and other shareholders in the public markets.

How it works: In an IPO, a company picks an underwriter, or an investment bank, that it will work with throughout the process. The underwriter helps the company prepare investor materials, draft the key SEC filings, pick the offering date, and provide the financial analysis to land on initial valuation and the size of the offering. Together the company and underwriter go on a “roadshow” where they meet with large institutional investors to market the deal. During this period, the company will respond to investor questions while also building an order book based on investor demand. Finally, the company and underwriters will determine the final offering price and allocation based on the level of demand for the deal. A critical part of the deal is allocation, in which the company and underwriters decide on how much each investor gets from the offering. This step is critical as it helps the company establish its long-term investor base. The day after the IPO is complete, the stock will open and begin to trade freely on a public exchange (typically NYSE or Nasdaq).

How it’s trending: We’ve been in a period of (relatively) fewer IPOs, due to a decrease in both the number of deals per year as well as the average float percentage (amount of the company’s equity offered in the IPO). The number of U.S. IPOs declined significantly over the past two decades, from about 300 per year from 1980-2000 to about 108 per year from 2000-2016, partly due to companies staying private longer (including the “quasi-IPO”).

Recently, however, we’ve started to see a reversal of this trend — in 2020 there were 172 U.S. IPOs that were not SPACs (special-purpose acquisition companies, an option we’ll discuss next). We expect this uptick in IPOs to continue given the massive and growing backlog of $1 billion-plus private companies; there are currently 700+ unicorns representing ~$2.2 trillion of value globally.

Meanwhile, available floats remain low and have declined as the standard of companies coming to market increases — stronger companies tend to have less need to raise cash and can do it at a higher price. As less of each company is being sold in any given offering, competition among institutional investors for the limited allocation increases, driving up the prices of their bids for all.

The scarcity of supply is exacerbated when you consider the limited liquidity available on the first day of trading. Only a small subset (~20%) of the deal is allocated to small hedge funds that are expected to “flip” the stock (i.e., willing to sell on day one, in contrast to the majority of allocation, which goes to long-term holders). For hot deals, this imbalance between limited supply and strong demand from institutional investors with unfulfilled allocation contributes to the first day trading “pop”. Hot deals also tend to attract significant interest from retail investors, adding to the one-day pop. (Our partners Scott Kupor and Alex Rampell have broken down the dynamics and data of recent IPO pops here and here.)

IPOs are generally one of the higher-priced exit outcomes when factoring in the deal price (price at which the company sells shares) as well as the opening trade (first trade in the open market). Part of this is due to presumed quality — IPO investors seek high-quality companies that balance seemingly predictable near-term operating results with upside potential long-term to drive returns. This suggests a stronger typical candidate profile for IPOs compared to companies that may have to (rather than choose to) pursue other exit alternatives such as SPACs

What it means for startups, founders, and investors: In a hot tech IPO market where desirable deals are massively oversubscribed, significant pops after IPO create more intense demand that pushes up pricing for subsequent deals. As such, the hot market itself becomes a valuation driver — this, combined with supply scarcity and the high quality of companies going public, contributes to the strong pricing performance we’ve seen for top tech IPOs. (More on guidance for CEOs here.)

Here’s how this plays out for companies: When a company hits the road to market their IPO to investors, they go out with an initial filing range, typically set at a ~15% valuation discount to their public peers’ trading multiples. This discount is used to entice investors into the IPO. A strong market with lots of investor demand can result in an issuer re-filing during the marketing period with an upwardly revised range. For a hot deal, final pricing may be struck even above that level. When this happens, the ~15% valuation discount effectively goes away. Since 2019, the average price for enterprise tech IPOs has increased by 18% from the midpoint of the initial range to final IPO pricing. [Source: Cap IQ]

The takeaway: IPOs will continue to be an attractive option, especially during hot markets, for solid companies (as well as for investors looking to drive returns post-IPO). Demand tends to drive higher prices.

SPACs

SPACs (special-purpose acquisition companies, or “blank check” companies), surged in popularity in late 2020 and early 2021 as an exit alternative for venture-backed businesses.

How it works: Going public via a SPAC involves a two-step process in which the SPAC sponsors (investors) create a publicly traded blank-check entity and combine it with an existing private target company to bring the target company public. The SPAC (already publicly traded after having raised lots of cash) and the target company agree on a pre-money valuation. The money sitting in the SPAC becomes the “money raised,” with typically a PIPE (Private Investment in Public Equity, a further institutional fundraise) done at the same time. PIPE deals are often done in SPAC transactions to (i) raise more capital to enable sponsors to acquire bigger companies that are supposed to be IPO-ready; (ii) build an institutional investor base with investors the sponsor believes will be long-term holders of the company’s stock; and (iii) get validation from investors both on price and quality of the target. PIPE investors are large private investors such as mutual funds and hedge funds and they benefit from buying the company stock at a discounted price.

Unlike a pure M&A (typically a full exit for existing investors), or a traditional IPO (temporary lock-up of shares for existing investors), the existing investors of the SPAC target company can choose to partially sell in the merger (typically under 20% of their shares) without the negative signaling risk associated with secondary stock sales in a traditional IPO. This is one of the benefits of selling to a SPAC; providing partial liquidity to target investors is expected by investors in a SPAC transaction. The other big benefit is that companies that have less-proven business and financial models can go public sooner than if they were to pursue a traditional IPO path.

How it’s trending: In 2020, total capital raised by SPACs represented 50% of the total IPO market, with the first quarter of 2021 eclipsing the full 2020 number. [Source: Morgan Stanley ECM and LionTree Weekly SPAC Dashboard]

The timing of a SPAC has changed: It used to take an average of ~3.5 months to obtain SEC and shareholder approval following the SPAC merger announcement to close. This timetable has increased by about two additional months, primarily because of increased scrutiny by the SEC on how SPACs are accounting for warrants and utilizing forward-looking statements.

What it means for startups, founders, and investors: While SPACs have grown as an exit option, the effective cost and ownership dilution of a SPAC are much greater than those of a traditional IPO. This is largely due to the direct value transfer from existing shareholders to SPAC sponsors and shareholders in the form of:

- Sponsor promote (“finder’s fee”): typically 15% to 20% of the SPAC size

- Sponsor warrants: purchased by sponsor for a nominal amount

- SPAC shareholder warrants: “sweetener” received with shares purchased at the SPAC IPO

Additionally, transaction fees are higher, because bankers are paid to take the SPAC public, handle the merger, and also raise the PIPE. All this leads to SPACs being a more expensive option for startups than traditional IPOs or direct listings (which we’ll discuss next).

This is likely to remain so, due to the underlying structure of sponsor promote and the valuation discount associated with less-proven companies.

The increased time it takes to go public through a SPAC is also putting additional pressure on SPAC sponsors to lower the target’s value at the time of the sale to a SPAC. That’s because PIPE investors commit to investing at the value of the target at the time of the merger announcement. Given the longer time between merger announcement and closing, PIPE investors are now taking a lengthened period of market risk. In addition, SPACs haven’t performed as well to date — post-merger SPAC stock price performance is mostly negative. That’s because many companies that went public via SPACs had less-proven business and financial models and have underperformed relative to the projections provided at the time of their SPAC IPOs.

Due to this combination of taking on greater market and timing risk, along with underperformance, PIPE investors over the last six months have sought greater protection via a higher haircut on target valuation. As a result, the traditional 15%-20% discount has now increased up to 25%-30%.

Advantages of SPACs over traditional IPOs include the ability to share projected financial forecasts with investors (which is not allowed for traditional IPOs other than through sell-side research analyst models at the time of the IPO) and the potential to partner with top-tier sponsors that can bring hands-on operating expertise to the business. These advantages can be meaningful for certain types of companies, especially those that may not be ready for “prime” time.

The takeaway: SPACs are a costlier and more dilutive option, but they offer an alternative for companies that have a less clear path to the public markets via traditional means.

Direct listings

Direct Listings, or DLs, have emerged as an alternative to a traditional IPO. Spotify used this path in 2018, and Slack in 2019, bringing greater attention to the practice. Outwardly, DLs look a lot like traditional IPOs — companies debut on the New York Stock Exchange or Nasdaq, with bell-ringing and other trappings. The key difference in a Direct Listing is that no shares are sold by the company itself, and therefore no capital is raised.

How it works: In Direct Listings, money is raised only through the sale of existing shares by founders, VCs, vested employees, and other investors, rather than through the issuance of new shares to institutional investors as is done in an IPO. These shareholders are allowed to sell their shares directly into the public market. This means that in a direct listing the company can’t hand-select the institutional investors it wants as shareholders, as happens in a traditional IPO as part of the book-building process. The market-making (or price discovery) really happens via an opening auction in which the exchanges (e.g., NYSE, Nasdaq) or their designees (“market makers”) solicit “bids” (the price and volume at which a buyer wants to transact) and “offers” (the price and volume at which a seller wants to transact). The auction occurs until a sufficient number of orders are “matched” — buyers and sellers are willing to transact at an agreed-upon price and volume to open the stock. This is aimed at creating a more efficient, orderly method of price discovery.

The advantage of this approach is that it potentially addresses some of the (heavily debated) pricing issues of traditional IPOs by erasing the traditional IPO discount and therefore the contrivance behind the first day pop. Enterprise tech companies that have gone public via a traditional IPO since 2020 have seen their stock trade 33% above the IPO price on the first day of trading, suggesting that the investment banks have underpriced IPOs and a significant amount of money was “left on the table” by the issuers (though not all agree with this view). This has brought increased scrutiny to IPO pricing on several fronts.

In a DL, the first day’s trading is based on the price at which buyers and sellers are willing to transact, rather than a price set by a company and its underwriters, leading to full price discovery at the open (comparable to the opening price on the first day of trading for a traditional IPO, which includes the first day pop) — though it’s still mediated by the exchange’s market makers.

How it’s trending: There have only been ten DLs so far, representing barely 1% of the total capital markets debuts over the same time period (it should be noted, though, that that includes three of the top five opening trade volumes of all time in the history of going public). The after-market “pops” have also been more muted in direct listings than we’ve seen recently for more traditional tech IPOs, suggesting DLs are achieving their purpose, albeit with a small sample size so far.

One factor to keep an eye on: Earlier this year, the SEC approved a proposal by the NYSE and Nasdaq that allows companies that are going public through a DL to raise primary capital (by issuing new shares). This change has the potential to meaningfully change the way private issuers think about public-listing alternatives, i.e. traditional IPOs, SPAC IPOs, or DLs.

What it means for startups, founders, and investors: Advantages of DLs include the lack of a 180-day IPO lock-up, so existing shareholders can sell at any time (including the first day of trading), and equal access for all buyers, so that retail investors have the same ability to buy shares as institutional investors. The potential downsides to DL are that there is no primary capital raised (although this may change in the future, as noted) so it may not be the best option for companies needing to raise money. In addition, companies going the DL route are required to provide financial guidance to the public — this leads to better financial transparency for all investors. (Companies should be mindful of their accountability to achieve these stated targets, however.)

The takeaway: The majority of VC-backed companies may not be well-suited for DLs, but better-known, higher-quality, and well-capitalized companies should consider them as an option, due to the absence of a typical IPO discount, and the structure that makes a DL’s first trade equivalent to a first day pop price of a traditional IPO. Unlike SPAC IPOs and traditional IPOs, existing shareholders can sell as much as they desire assuming there is ample trading liquidity.

M&A

How it works: Unlike traditional IPOs, SPAC IPOs, or DLs, a sale of a company through a merger-and-acquisition is a true exit whereby the existing shareholders of a target sell 100% of their ownership to a buyer. M&A processes can vary widely from highly structured sale processes to bespoke conversations between a company and any given number of potential buyers. Typically a company works with an investment bank to identify potential acquirers and structure a process that meets their needs. In this process, bankers will help the company establish valuation expectations, key points of deal structuring, and assess financing options (cash, debt, equity, or a mix between the different options) to pay for the target. After buyers sufficiently diligence the target, they present offers and begin the negotiation process with the target. Once the target agrees on a final offer, the buyer and seller sign a final purchase agreement and the transaction can move towards a closing. The final step post-close is for the buyer and seller to merge the two companies’ operations.

How it’s trending: Economic optimism and abundant capital have fueled record-level M&A activity on a global basis. Global M&A volume through August 2021 was $4.0 trillion, the highest year-to-date levels of M&A activity ever. For the same period, the technology sector continues to be the most active industry with over $1.1 trillion in M&A volume, up 182% from the prior-year period. [Source: Citi Global Executive M&A Summary]

As pandemic uncertainties have lifted, business leaders are recalibrating their strategy and accelerating the adoption of technology. In addition to corporate buyers, private equity (PE) fundraising has been brisk in YTD 2021 — PE firms now have more than $1.9 trillion of dry powder. And while the creation of new SPACs has slowed, there are 435 SPACs with $133 billion still searching for targets. This abundance of capital and low interest rate environment bodes well for a continued strong level of M&A activity during the second half of 2021. [Source: Citi SPAC Weekly Update]

What it means for startups, founders, and investors: Despite the full exits available for shareholders in an M&A, these types of exits may not represent the best valuation outcome.

There are several reasons for this:

Lack of asymmetric information advantage: Potential acquirers have expertise in the industry, sector, technology, and competitive landscape of the private target, and can value it much better than IPO investors. Thus the private target insiders have much less information advantage against acquiring firms. In contrast, IPO investors have less expertise and information than insiders, which can lead to higher valuations in the IPO market.

Financial projection haircut: Acquirers conduct careful due diligence on the target’s forecast to determine if it is realistic. One pitfall for any buyer would be to take at face value any forecast that appears overly optimistic about future performance relative to historical performance. In most cases, a significant “haircut” is applied to the forecast to offset the optimistic nature of the long-term plan. In an IPO, the issuer guides research analysts working on the IPO to the issuers’ two-year projection, which then is shared with institutional investors during the IPO roadshow. Issuers determine the “haircut” to their internal projections to have some cushion to meet or exceed their projections after their IPO. These haircuts are significantly lower than the haircut applied by an acquirer and the sell-side research analysts take them at face value

Higher pricing multiple at IPO and greed: At times when the equities markets are humming, there’s an additional reason that M&As may not represent the best valuation outcome. We’ve witnessed a historic rebound in the public equity market since the March 2020 low. We’ve also witnessed a strong tech IPO market. As long as there’s a strong equity market, there will be a strong IPO market. In a hot IPO market, an M&A exit price is often lower than what the same target can potentially achieve by going public. This assumes the target is mature enough to do either.

The obvious question: Why is the IPO valuation premium higher in a hot IPO market than a control premium (the premium paid over standalone valuation of the target or its publicly traded price if the target is public) a target can achieve in an M&A exit?

That’s because as tech IPO aftermarket performance increases, IPO investors become much more willing to pay a higher multiple at IPO pricing, expecting that the IPO will still have its first-day pop. IPOs generally do not pop 50% on the first day of trading based on fundamental, long-only mutual funds adding to their IPO-allocated positions. These pops are generally driven by short-term focused hedge funds and to a lesser extent, retail day traders.

The takeaway: M&As provide a “true exit” for investors, but generally lower valuations than IPOs (in a hot IPO market).

Secondary sales

An additional liquidity option has emerged in recent years as companies stay private longer and a lack of liquidity becomes a bigger issue for employees and investors. As a way to compensate and retain employees, many private companies are now looking to provide interim liquidity to early employees (and other shareholders), instead of requiring them to wait for a public offering or M&A to see liquidity.

This can be done through a secondary sale, in which private company stock is sold by an existing stockholder to another private party, with the proceeds going to the selling stockholder. While secondary sales have clear direct benefits for employees (who receive interim liquidity) and for companies (which retain valued employees), they are part of a broader innovation trend in how companies are financed and valued. This trend can help alleviate many of the mispricing issues that penalize companies and shareholders.

How it works: First, the basics: There are two ways to structure a secondary sale. One is a buyback of shares by the company, funded by existing cash on the balance sheet or cash from an equity round. The second is a direct purchase of shares by a third party, either paired with an equity financing of the company or as a standalone transaction.

In a company-sponsored buyback, the company decides which shareholders may sell (usually this is an option reserved for employees who have worked for the company for some time) and places limits on how much they are allowed to sell. It is fairly typical to limit the amount any one employee may sell to ~10% of vested shares to ensure that the employee continues to have meaningful equity incentives. This type of secondary sale is less common for venture-backed private companies because they typically don’t have consistent cash flows to complete such repurchases. Further, they see greater returns on investing their available cash in the growth-drivers for the business (product development, customer acquisition, etc.).

More common are direct transactions with third parties (often referred as secondary market transactions), in which there are a broad range of buyers including existing investors, dedicated secondary funds, large family offices, high-net-worth individuals, and retail investors. This is sometimes done as a one-off negotiated transaction typically initiated by a broker and involving a limited number of sellers. When it involves hundreds of sellers, a structured liquidity program such as a formal tender offer is more efficient. A third-party tender offer is a company-sponsored liquidity event that gives shareholders the opportunity to tender (sell) their shares to outside investors. The company brings the buyer to the table, sets the price, and manages the entire transaction. This makes it possible for companies to control which new investors enter their cap table.

Secondary market transactions can be operationally challenging for companies — and this has led to tech innovations whose effects may be felt beyond simply secondary sales.

New automated platforms have emerged, such as CartaX, Nasdaq Private Market (NPM), and Morgan Stanley Shareworks, that automate and manage these sales, enabling companies to (i) reduce administrative and operational burdens; (ii) deal with limitations on stock transfer restrictions; (iii) reduce settlement time; and (iv) provide controlled access to company information. More broadly, technology could have significant impacts on pricing and related issues that currently bedevil liquidity events.

Today, for example, secondary trading prices influence the reference prices for Direct Listings — for Spotify, the reference price was based on the last private secondary trade, and with more recent DLs, reference prices were guided by the volume-weighted average price of their recent secondary trading activity. But as secondary trading becomes more common, we expect secondary trading prices to become even more influential on valuations for all types of exits (M&A, SPACs, IPOs, and DLs).

It’s not hard, in other words, to envision a world in which startups, facilitated by automated trading platforms, will have access to near-continuous price discovery for their shares, rather than being limited to valuation snapshots every year or two, due to the decreased burden on companies of offering such programs.

This closes the gap between secondary trading prices and IPOs and, as access to information in private companies increases, it minimizes the underpricing of IPOs and the one-day pop that leaves money on the table for startups and investors.

How it’s trending: There’s increasing demand from employees and other shareholders for earlier liquidity — for example, in the first nine months of 2021, Carta’s platform facilitated 77 liquidity programs for private companies, with a total offering value of $4.7 billion, compared to 31 programs ($2.2 billion) in 2020 and 24 programs ($0.4 billion) in 2019. [Source: Q3 2021 Liquidity Report, Carta]

Further, the number of investors who have moved into private markets has grown significantly. These investors have a deeper understanding of the private markets and how they operate. As high-quality institutional investors increasingly move into the private side, this highlights a growing acceptance of private markets and creates more buyer-side diversity.

What it means for startups, founders, and investors: The trend is going in the direction of every company eventually offering liquidity to their employees before going public and, as this becomes the new norm, companies may need to offer more frequent liquidity programs to stay competitive. Doing so should not just help private companies compete for talent against each other, but should help startups better compete for and retain talent against public companies.

Plus, the way startups raise primary capital and partner with investors may look very different in the future — as secondary stock sales become more frequent, it should lead to easier price discovery for private company financing rounds. (Carta, for example, raised its Series G in August 2021 after running a secondary sale auction on CartaX in February 2021 that gave the company and investors a true indication of its value.) This consensus on valuation among all parties, enabled by technology and more-frequent secondary sales, can eliminate the need for companies to waste time and energy negotiating price, and companies can therefore focus on different factors in choosing an investor, e.g. the strategic value the investor may bring to the company rather than simply the price an investor was willing to offer.

Still, today, there are many factors that a private company should consider when deciding to enable secondary sales. Will the sale help employee retention, or hurt it (because taking money off the table could make it financially feasible for some to leave)? Will it impact the company’s ability to raise capital in the future? Is it fair to those that are participating as well as those that are not? What impact does the sale have on the value of the company’s common shares, (i.e., the 409A valuation)?

Companies should also keep in mind that, in the near term, because there’s no centralized market trading portal, matching supply and demand can result in less efficient price discovery. This can lead to sellers of private company stock leaving money on the table. Auction-driven price discovery for tender offers is beginning to be widely used to minimize mispricing.

The takeaway: Although secondary transactions are not a liquidity event for private companies, they make it possible for employees and other shareholders to obtain partial liquidity even without an IPO or M&A. Secondary trading markets will continue to evolve over time, leading to better pricing transparency, and automated platforms are easing the burden on companies. Most importantly, they hold the potential of transforming private company valuation in larger ways.

These analyses change as the market changes, and this discussion matrix is based on the current strong equities market that we are seeing. In a softer equity tech IPO market, we expect the pricing delta between IPOs/ DLs to converge with M&A exits. The evaluation framework of deciding which exit is best for your company will change based on equity market conditions.

Navigating exit options requires careful thought and analysis of the relative strength of the company, the makeup of the investors, and the ultimate long-term goals of the founders and investors. While this can be overwhelming for founders who are faced with many options, we hope this decision matrix clarifies the different exit options and can better guide you towards what is right for your company.

-

Blake Kim is a partner on the Capital Network team, focused on enterprise companies.

- Follow

-

Quinten Burgunder is the Chief Of Staff, Growth & Marketing @ MUBI