“Growth-stage venture” has emerged as its own asset class, and we think it’s the most important asset class in the world. But we also think that most people misunderstand what it’s about. It’s not just a structural change in fundraising, or about valuations, or staying private. Late-stage venture is about late-stage founders. It’s about a specific kind of person, who can keep deploying dollars attractively, indefinitely.

The existence of founders like Ali Ghodsi or the Collisons has proven that the right kind of person can keep growing ambitiously, forever. Technology has gotten so powerful for company-builders, and yet remains so non-diffused in the economy broadly, that killer founders who understand how to use it will always be an attractive destination for investment dollars, versus anything else, and they will ultimately create the majority of the asset class’s returns. You may as well accept that these founders are the asset class; let them cook.

The alpha in startups is the founder’s decision-making

The starting premise of tech companies is that technology is the leverage. But technology is not enough. Technology on its own, even if applied optimally and enthusiastically to solving business problems, eventually reaches its limits like anything else. Technology on its own does not differentiate a company, or tell you how to chart your own path. That’s the founder’s job.

The alpha of founder-led companies is in the founder’s decision-making. Founders carry the burden of deciding when to surf the wave of tech best practices (which is most of the time!) versus when to zig when others zag, and make brave decisions against the consensus. Only the founder can make and communicate these decisions legitimately, whether it’s betting on a new architecture like Databricks’s “Lakehouse” model, or critical acquisitions like Facebook buying Instagram. The alpha in a company is in the founder’s ability to spot non-obvious potential from their vantage point, apply it early and aggressively, and course-correct with new information.

Venture Capital exists on the premise that great founders have an unfair advantage at these capital allocation activities, compared to anywhere else. The alpha is in every decision the founder makes that goes well, and the opportunity set perpetually refreshes itself as technology improves. The VC’s job, frankly, is to find those rare founders who can consistently do this, and give them the freedom to operate, a long-term mandate, and resources that actually help. That’s the job.

Private markets have grown the way they have because there is so much demand to get exposure to this alpha. Any dollar invested into the software can either go to founders who immediately know what to do with unfolding technology potential, and therefore growth potential; or they go into other asset classes where there is inflexibility in where the returns come from, lagging ability to adapt, and only your principal to lose. To us, that’s an easy choice.

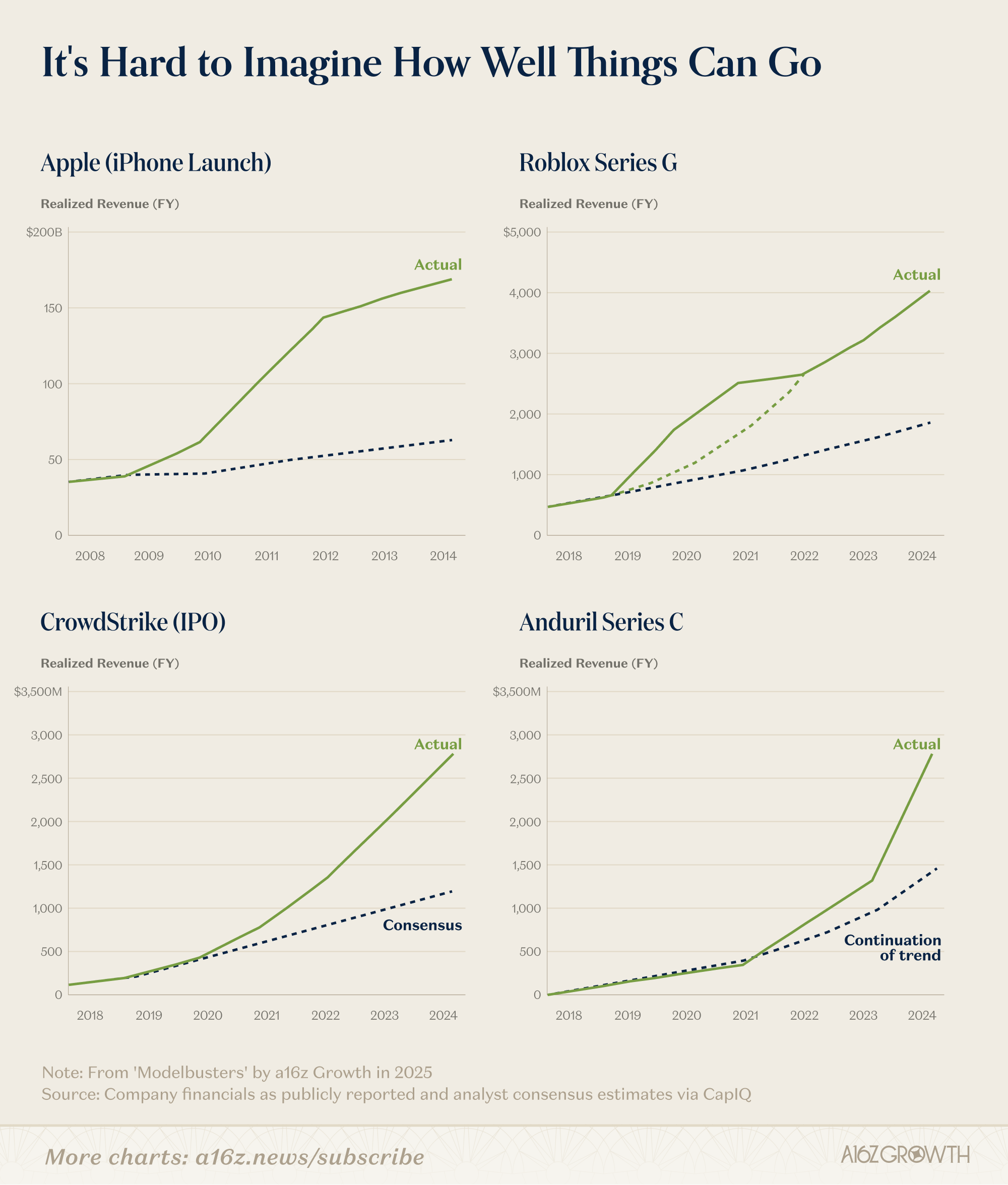

It’s hard to imagine how well things can go

It used to be common practice in Silicon Valley for Venture Capitalists to replace the founder with a “professional CEO” after Series B or so. With hindsight, we can see how foolish that practice was. (A16Z, twenty years ago, helped legitimize a new model for venture capital where technical founders learned how to become ruthless business operators, while retaining command over their product and tech stack. The rest of VC has since conceded the point.) The error was in a failure to imagine how well things could go, if the founder simply got to remain in founder mode. The VC’s job is to not make this mistake.

This cognitive error is shockingly persistent, even in our industry. It goes against every investor’s instinct to expect 100% a year revenue growth, over and over again, without eventually slowing down. (For example, in the public markets, not a single analyst thought that Apple or Visa could keep growing at the rates they did for two decades.) It is human nature to eventually concede a terminal value that seems reasonable. But not for elite founders.

When founders go public, the popular narrative is that they suddenly have to make quarters, and suddenly have to care about earnings. This is true, but sort of misses the point. Founders are not afraid of pressure to perform; not if they’ve made it this far. What founders don’t like is the pressure to do the consensus thing, that pervades analyst calls and shareholder feedback, rather than make the bets that would result in that continued 100% growth. It goes against their instincts about how to make good decisions, and about where the alpha in the company comes from. And each generation of founders learns from the previous one; that’s why they’re staying private longer.

Who’s in the car?

When Andreessen Horowitz made its mark in early stage venture fifteen years ago, we got a lot of flack from established investors, from how they perceived our “founder-friendly” and “service-oriented” approach to founders. If startups “are a lottery ticket”, as investors would joke to each other, then why make so much noise about marketing, hiring, or platform services, just to win more deals? The conventional wisdom was that founders and investors were fundamentally at odds with one another; you weren’t supposed to throw your lots in together.

Founders appreciated it, though. The founder’s job is a lonely existence; there are few people outside your company who can genuinely help you, and there are few people you can absolutely trust. (As they learned after Travis Kalanick got fired from Uber: you can be the greatest founder of a generation, but your investors may have other priorities.) There are only a small number of people “in the car with you” on the founder’s journey.

Late-stage founders are protective of who they let in the car. The median investor or board member, particularly outside board members, are not going to have skin in the game with founders in the same way. And most early stage investors, grateful of them as you are, are probably not going to be able to help founders all that much at larger scale. Founders at this point are expanding internationally, going multi-product, and they only need help if it’s at the pace they expect, at the scale they’re after. Very few investors genuinely check both boxes: they can actually help, and they can actually be trusted.

We built our business to make sure we can keep serving founders, and remain in the car, for as long a time horizon as the founder could ever want. Founders know that their investors are a tool kit for achieving objectives; we take the responsibility seriously.

Founders are it

The whole premise of tech companies as attractive investments is because technology yields increasing returns to scale. If there’s one thing we’ve learned, working closely with these success stories, is that this is true because founders make it so.

Founders are the rare individuals who can keep up with the rapidly changing opportunity set, apply the full force of their leverage to their vantage point, and put dollars to work forever. So long as technology keeps on delivering non-obvious opportunities, this will remain true.