Watching the generative AI space shape up over the past several months has reaffirmed my belief that, as product cycles mature, different types of builders have leverage at different moments in the cycle. And, at this early stage in generative AI, technologists and product pickers will likely have the biggest impact on which companies emerge as winners.

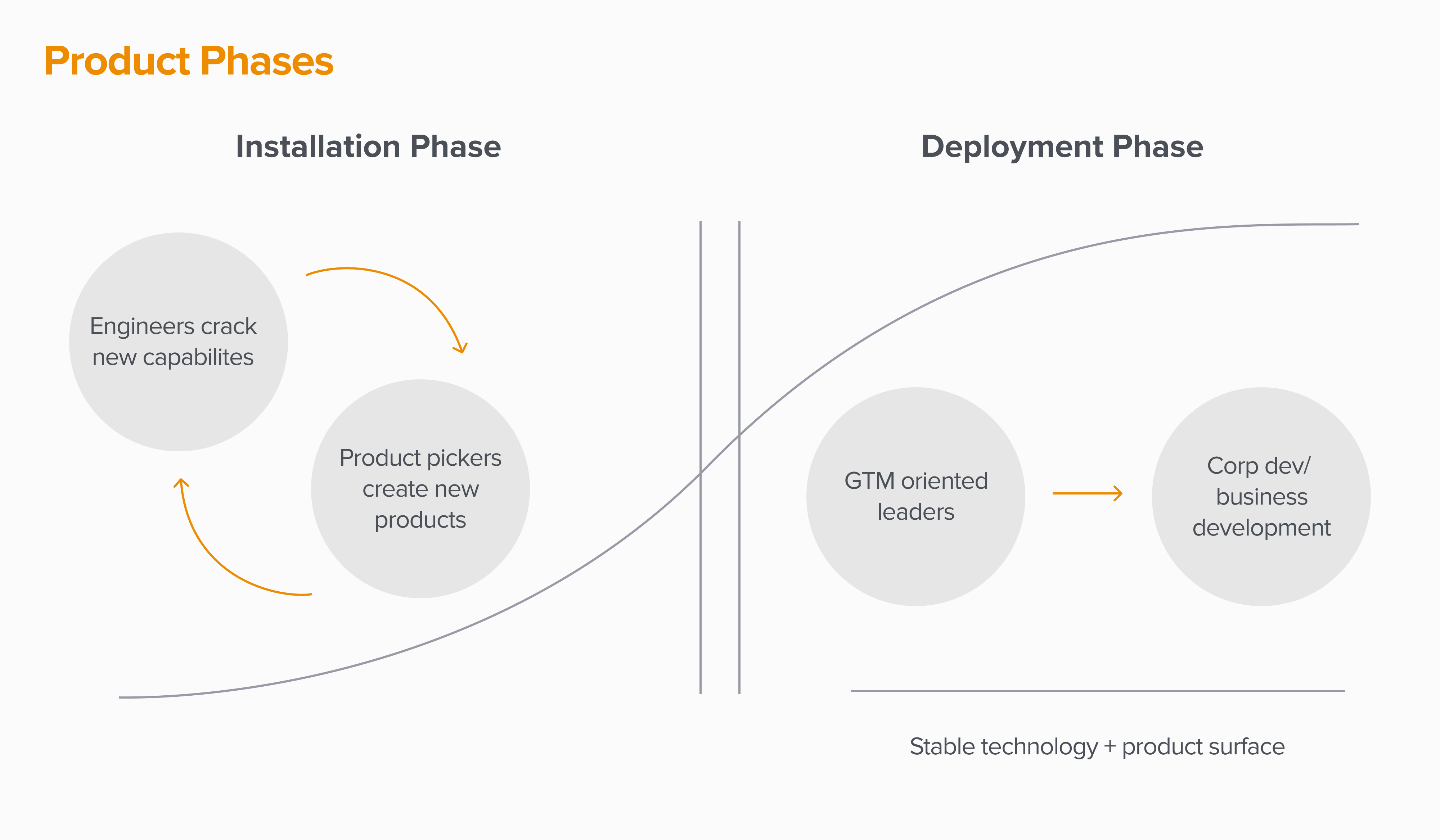

Typically, technologists and product designers have the leverage early in a product cycle as new capabilities and product patterns emerge and stabilize. Technologists and product pickers are the kings in this stage because of the rapid feedback loop between new capabilities exposed by the technology and new compositions of those capabilities delivered to customers by product pickers. This is too soon for a purely GTM-oriented founder, as the underlying technology and product patterns have yet to stabilize; word of mouth is the biggest driver of customer adoption. This corresponds to what Carlota Perez would call (in Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages) the “installation phase” of a new technology, when exuberance drives rapid installation and adoption of new technologies, lead by tinkerers and technologists.

Later, as the product patterns commoditize and the goal is to maximize market share for products that are already working, marketing-oriented founders have the advantage. This is why GTM-oriented founders dominate markets like SaaS: The underlying enablers have stabilized and hardened, and there is a lot of competition (it’s crowded), so the battle shifts from the feature war to a GTM execution game. Finally, as the marketing patterns and best practices stabilize, and markets consolidate around a few winners, business development and corporate development leaders (at new companies and incumbents) have leverage.

These two cycles (marketing- and business-development-led) correspond to the “deployment” phase that Perez outlines, where new technologies are widely deployed throughout industry and society, delivering the benefits more widely than in the installation phase.

Learning from other fast-growth markets

Of course, the frenzied development pace within the generative AI space is not new. These same dynamics (at the same pace) also played out in the early days of the Facebook Developer Platform and the iPhone App Store. During this time, in 2008, we were building Social Deck, and we rapidly grew to over 1 million users within one month of launch. We achieved this by inventing and leveraging new capabilities on mobile — like SMS notifications and an address book for social graphs — and also inventing new product patterns (real-time multiplayer/social apps didn’t exist on mobile at the time). At that time, knowing how to “build for mobile” was a competitive advantage that only a small number of technical and product-oriented founders understood, and I came to believe from that experience that having differentiated technology and products is how all great businesses are built.

However, when we built our second mobile company, Snowball, in 2014, we found that many of the same efforts fell flat. We did invent new capabilities (intercepting and routing notifications) and introduced new product patterns (extending the homescreen and the notifications feed on Android), but none of these were enough to drive breakthrough product growth. On reflection, I realized that by 2014 the product and platform surface for mobile had largely stabilized, and there wasn’t either the speed or the significance of changing capabilities to unlock product-led growth. What was needed at that time was expertise in GTM and distribution, which is why product- led companies like ours and Cover were out-executed by our distribution- oriented competitors.

Generative AI is in the installation phase

We’re seeing the early phases of this cycle play out in GenAI: The underlying technology capabilities are changing weekly and, thus, engineers and technologists are highly advantaged. They’re able to evolve product patterns and improve customer value and experience on a weekly basis. In recent weeks, for example, we’ve seen the introduction of multi-modal input and web browsing to ChatGPT, and the introduction of the ChatGPT plugin architecture, which broke an assumption that the right third-party integration point into the OpenAI ecosystem was to wrap products around its API. If a founder can’t quickly adjust to these changes, they won’t be able to keep up with the market.

Related, the new product patterns are often completely divergent from existing product patterns, but that’s not always apparent early in the cycle. This can make it appear as if incumbents are advantaged over startups. For example, we’re seeing large language models (LLMs) integrated into email, spreadsheets, documents, and other knowledge-worker artifacts — however, we haven’t yet asked whether these artifacts even make sense in a world of widely deployed LLMs. Why have a GPT model write an email for Alice just so another GPT model can summarize said email for Bob?

(For more of my thoughts on designing products for generative AI, read my piece on probabilistic products.)

Now is the moment for programmers and product designers in generative AI

If there’s a lesson to be learned here, it’s that founders need to carefully assess which phase a market is in and think through how that matches their superpowers. In generative AI, where the application architecture is unstable and is likely to shift as the underlying platforms and capabilities rapidly evolve, it’s the perfect time to be technical/product-oriented founders who can rapidly re-design their experiences to incorporate the newest platform features and product patterns.

Furthermore, this market is likely to be dominated by these types of founders for longer than most, because the GenAI platform surface is being discovered more than designed (i.e., the characteristics of the platform are emergent, as opposed to something like the iOS API that’s designed in a fixed way). Because we still don’t fully understand what these platforms are capable of, any attempts to codify ideal use cases and user behaviors is very likely premature.

All of which is to say: If you’re a programmer or product designer, now is the perfect time to build. What are you waiting for?!

* * *

The views expressed here are those of the individual AH Capital Management, L.L.C. (“a16z”) personnel quoted and are not the views of a16z or its affiliates. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by a16z. While taken from sources believed to be reliable, a16z has not independently verified such information and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. In addition, this content may include third-party advertisements; a16z has not reviewed such advertisements and does not endorse any advertising content contained therein.

This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by a16z. (An offering to invest in an a16z fund will be made only by the private placement memorandum, subscription agreement, and other relevant documentation of any such fund and should be read in their entirety.) Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Andreessen Horowitz (excluding investments for which the issuer has not provided permission for a16z to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://a16z.com/investments/.

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others. Please see https://a16z.com/disclosures for additional important information.