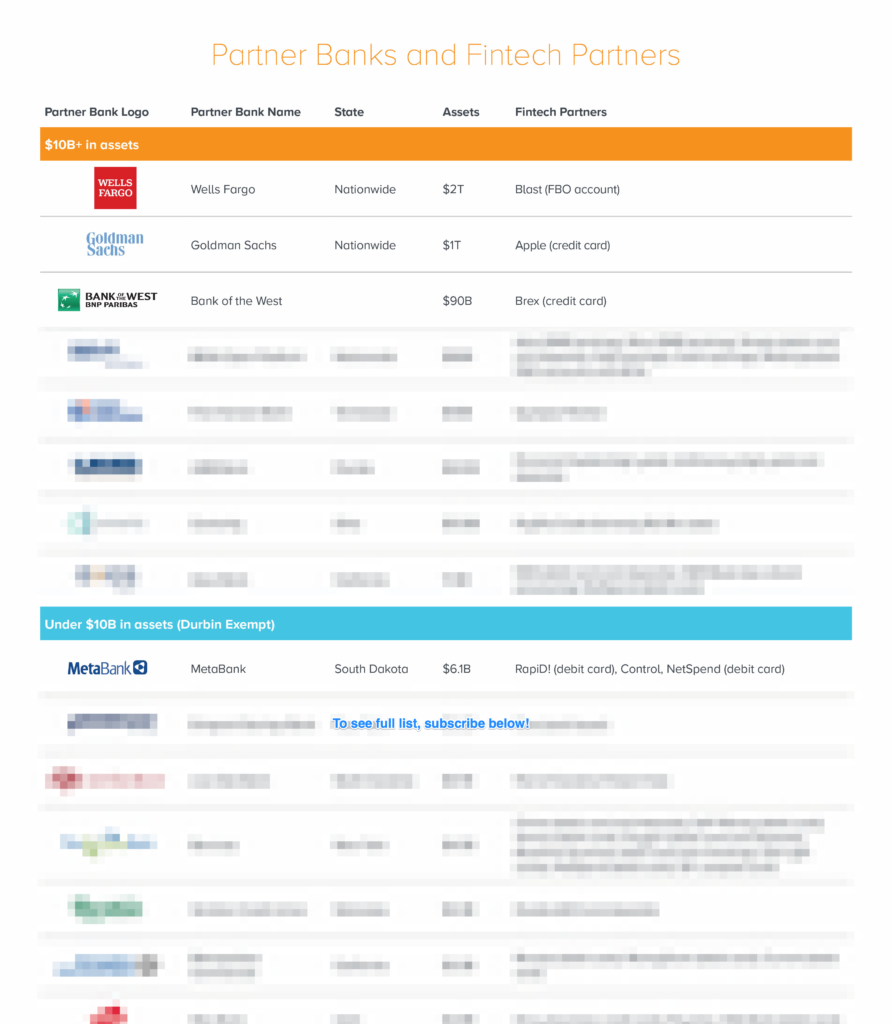

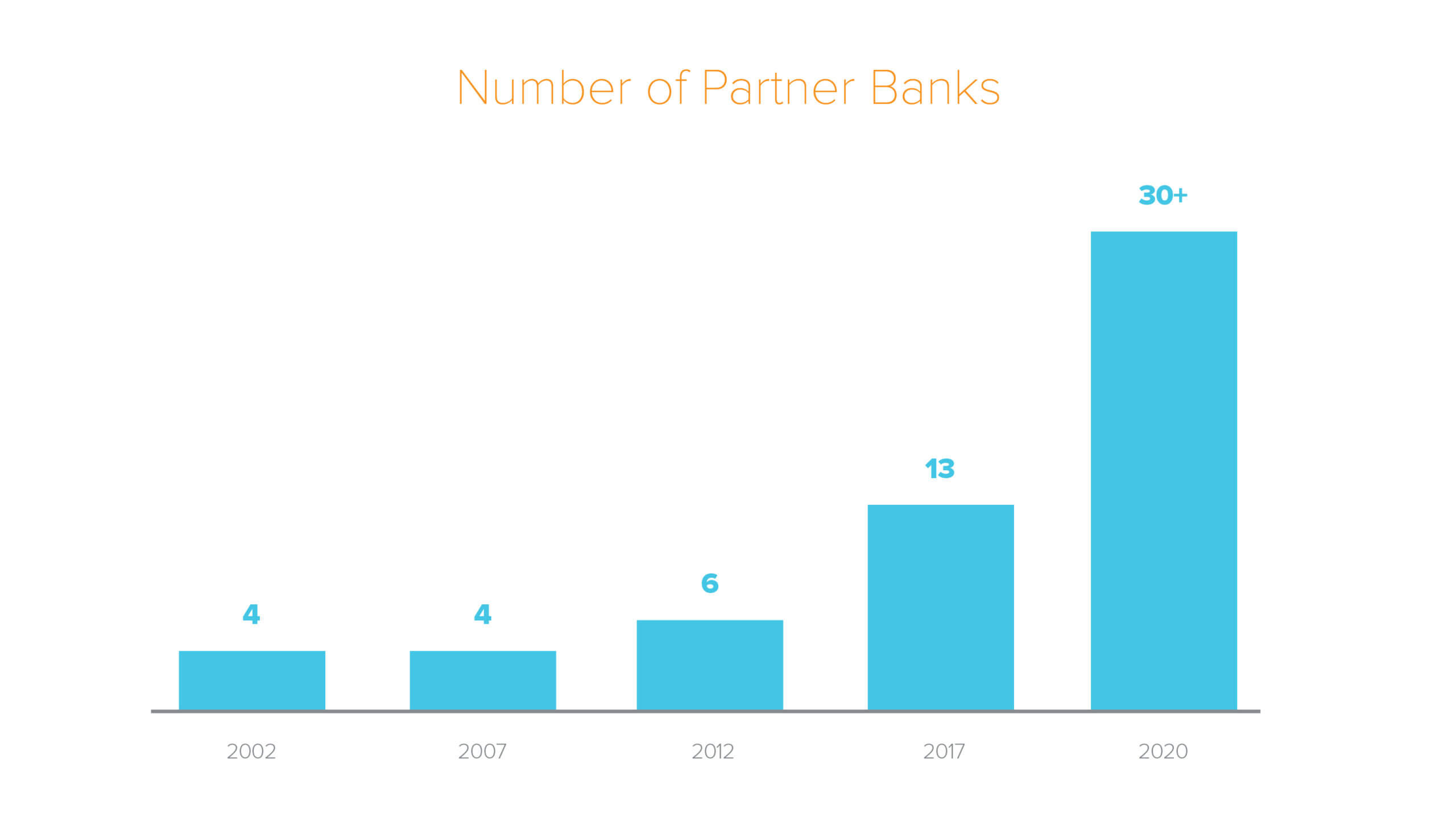

Partner banks, chartered institutions that provide fintech companies access to banking products, have exploded in recent years—by our count, their ranks have grown more than five times over the past decade. Today, there are more than 30 partner banks representing hundreds of fintech relationships and financial services. These partnerships come in all shapes in sizes, from mega-banks like Goldman Sachs, which powers the Apple credit card, to Hatch Bank, which has $68 million in assets and started with a single fintech partner, HM Bradley.

The rapid rise of this trend begs the question: Why has the number of partner banks increased so suddenly over the past decade? For one, the relationship is mutually beneficial. Fintech companies are able to offer banking products without the regulatory overhead of becoming a bank, while banks harness these partnerships to improve their returns by gathering low-cost deposits or growing asset-light fee streams. In addition, it has become increasingly easier to form these partnerships. Eliciting a partner bank used to require a herculean effort, due to both compliance concerns and technical hurdles. Now, thanks to the rise of companies that provide banking infrastructure as a service, fintech companies can launch products in a matter of months, not years.

As the partner bank network has grown and fintech time-to-market has decreased, entrepreneurs are better equipped than ever to continue innovating in financial services. Still, it’s a complicated many-layered space. In the graphics below, we aim to provide greater visibility into this interconnected and expanding ecosystem: the banks, the fintech companies, and the many services these partnerships afford. We’ve mapped out how partner banks and fintech companies collaborate to provide greater value and additional services for consumers. To view and download the extended list of more than 30 partner banks and fintech partners, including the products they offer, subscribe to our fintech newsletter.

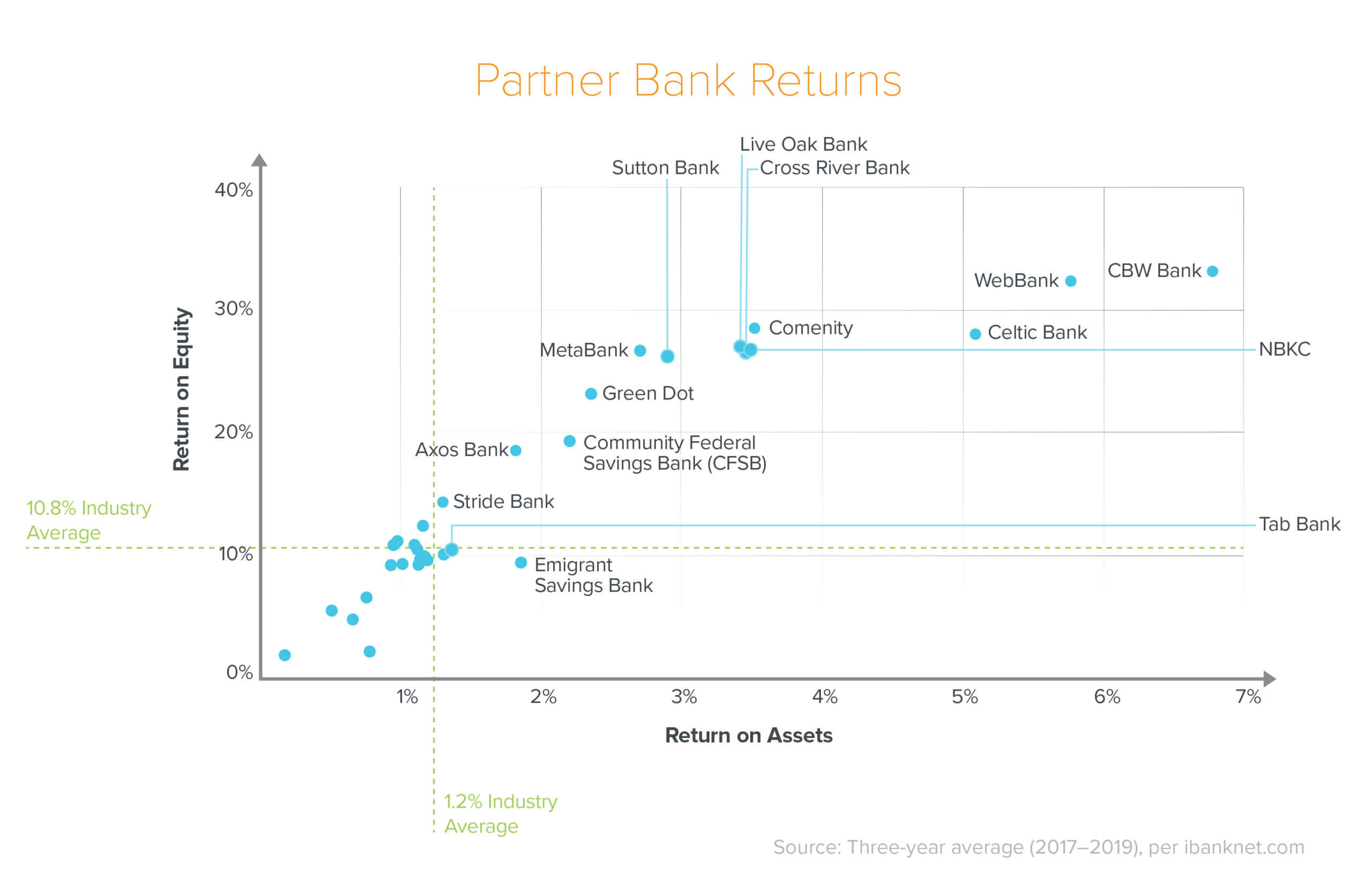

This recent swell in partner banks benefits both the banks and the fintech companies—that marriage of necessity can work well for both parties. A survey of partner banks’ returns shows that many operate at profitability levels two to three times above average.

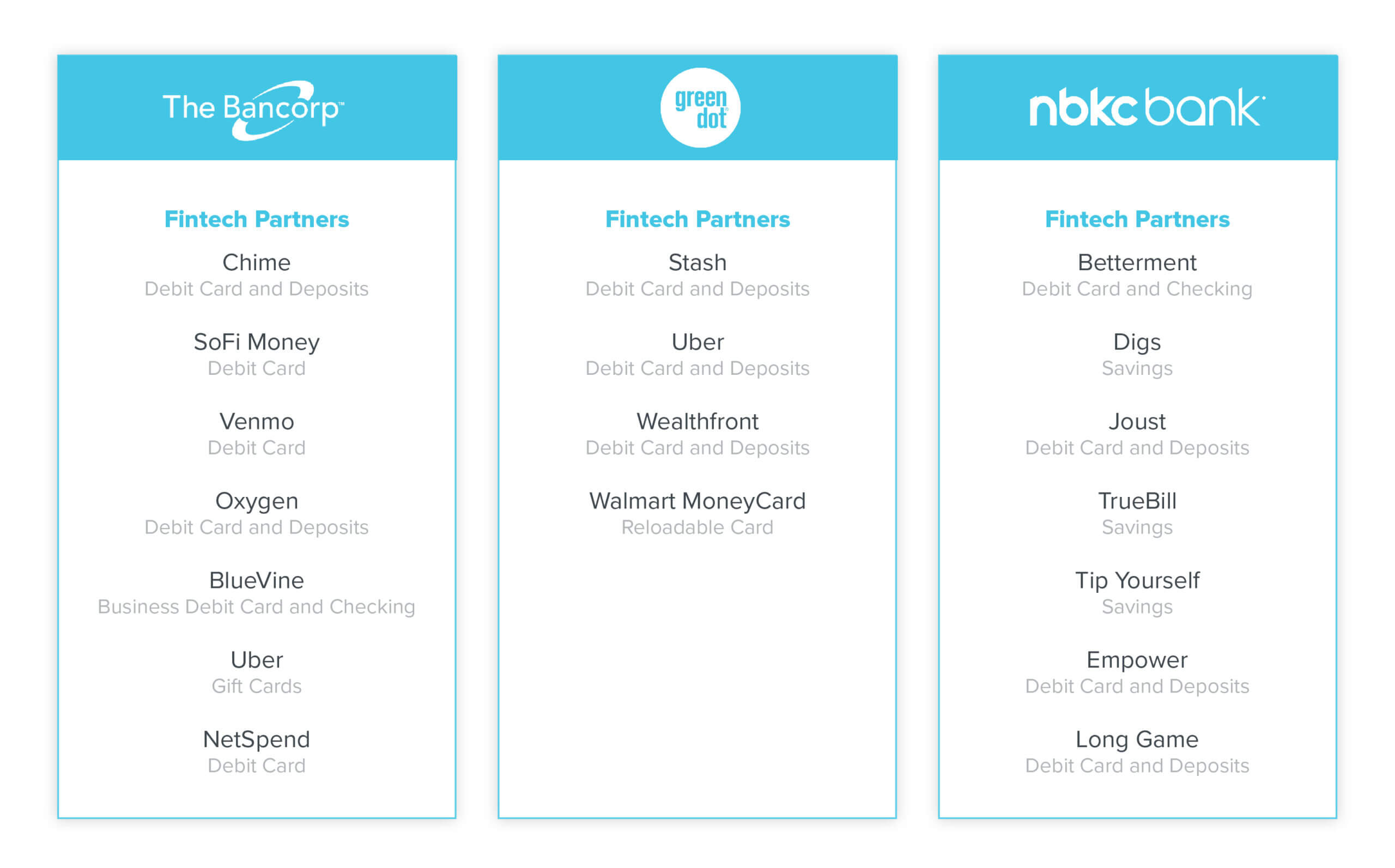

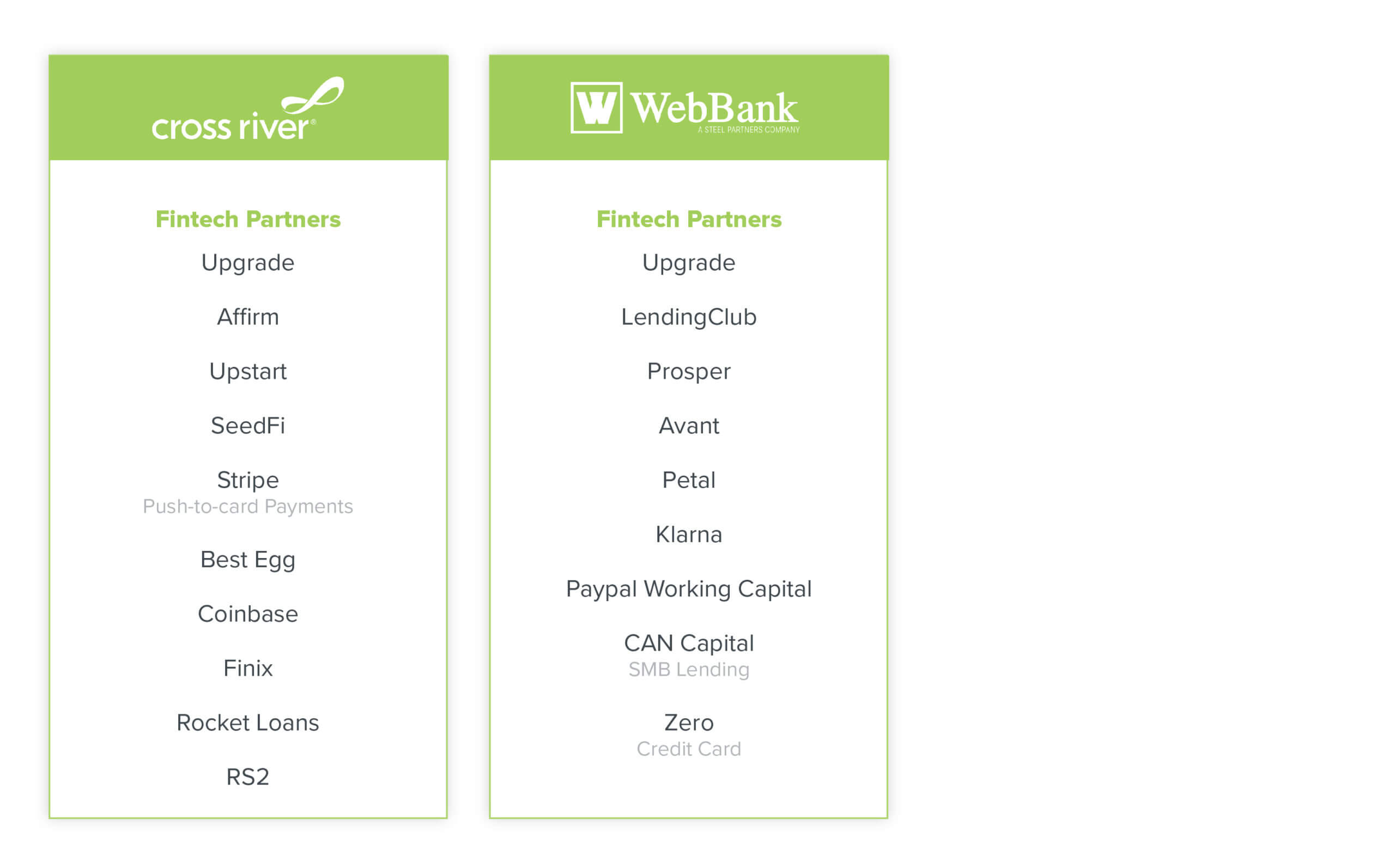

Many of these banks specialize in different forms of partnerships: Bancorp and Green Dot focus on powering consumer banking experiences, for example, while Celtic Bank, Cross River Bank, and WebBank mainly pursue partnerships with lenders.

Select Categories and Prominent Partner Banks

Consumer Banking (Debit Card and Deposits)

Bancorp, Green Dot, and NBKC have partnered with a number of consumer fintech companies that aim to offer full-stack consumer banking services. These banks have relationships with some of the largest neobanks, as well as corporates like Uber and Walmart. Green Dot has had a partnership with Walmart since 2006.

Consumer Lending

Cross River and WebBank and have the largest rosters of lenders as partners.

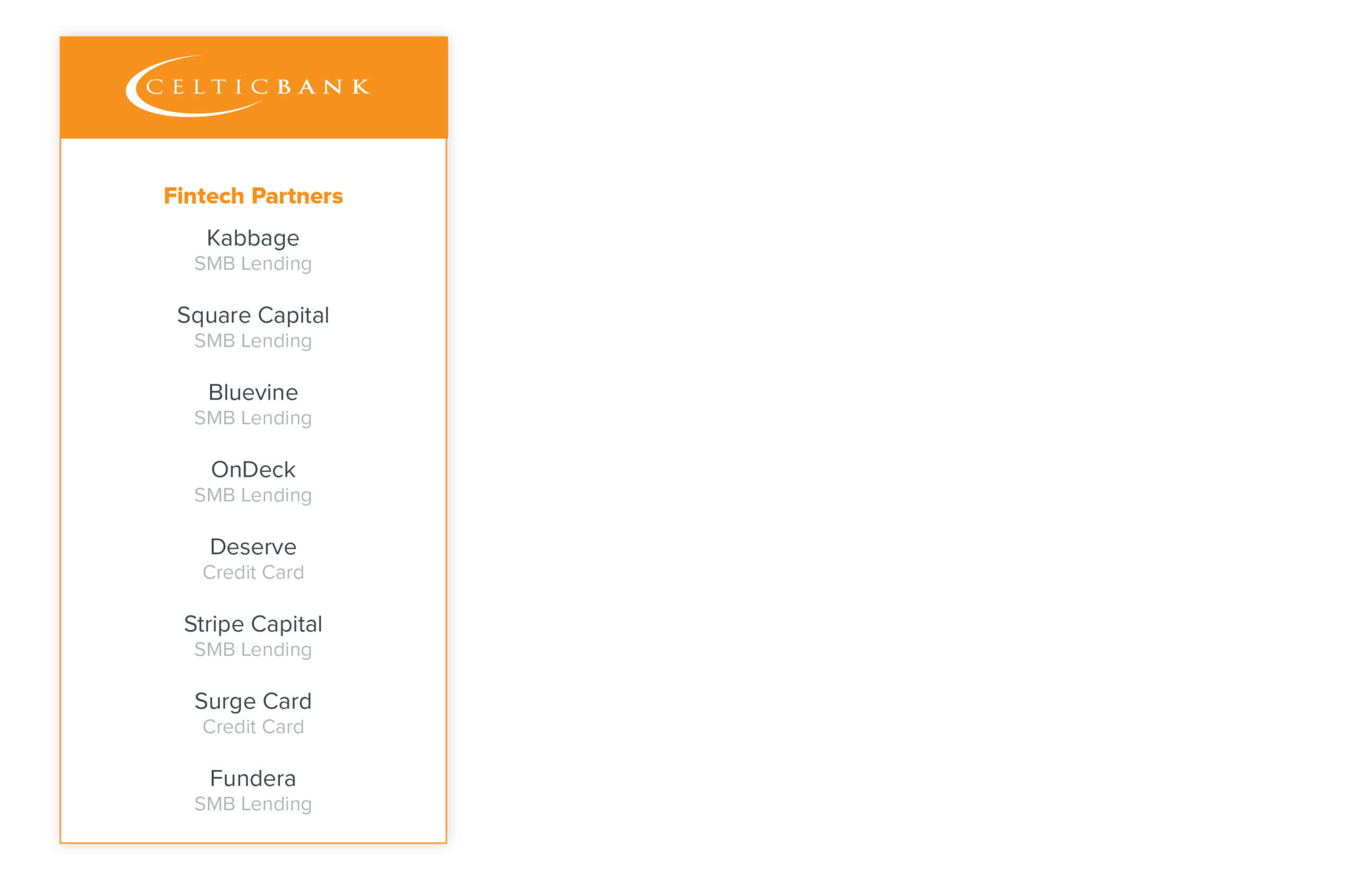

SMB Lending

Celtic Bank is a leading provider of SMB loans and has been an early partner to SMB-lending fintechs. Celtic has been engaged with Kabbage, for example, since 2008.

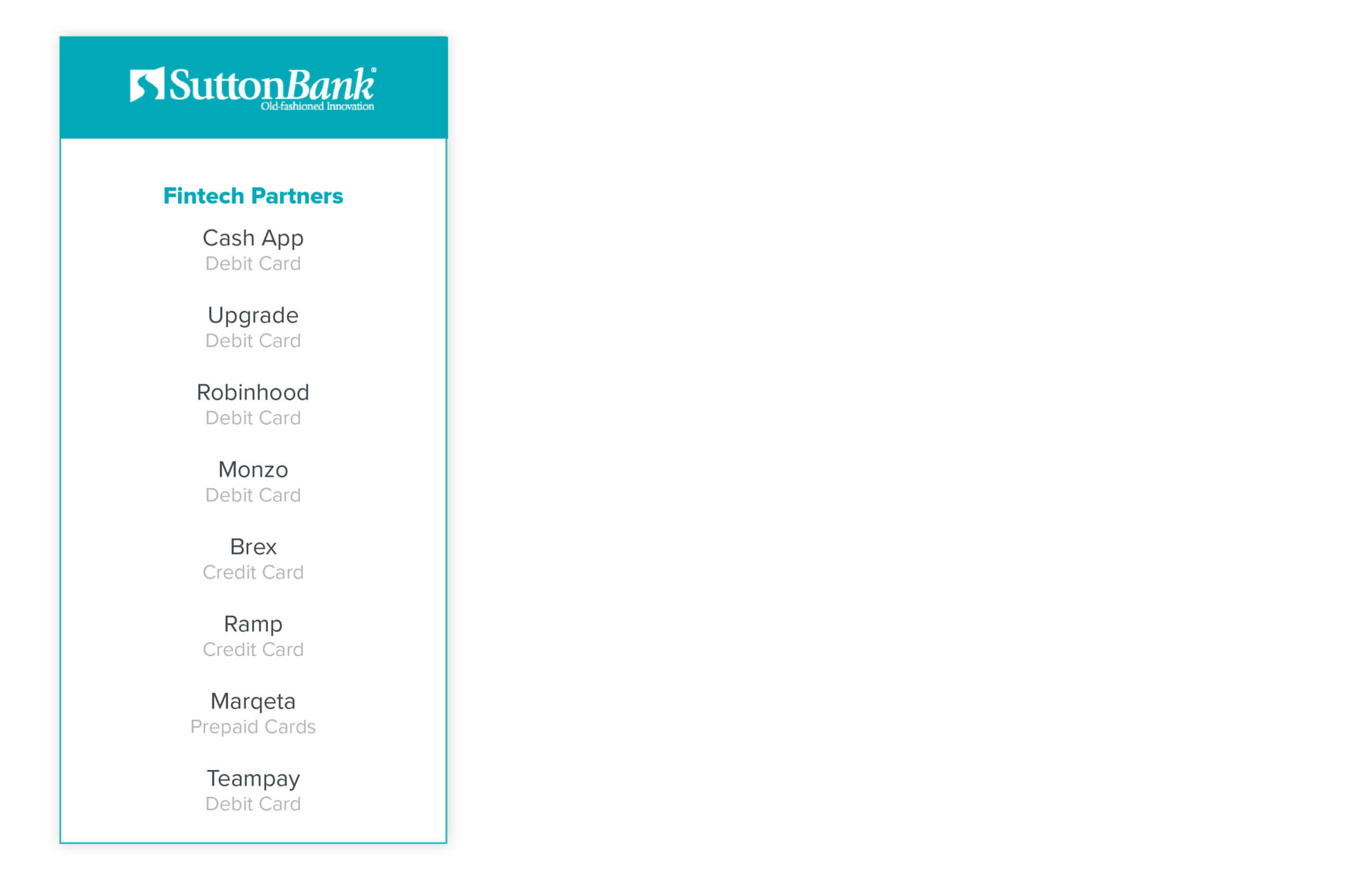

Card Issuance

Sutton Bank provides consumer and business card issuance across debit and credit for large players. Notably, Sutton Bank and Marqeta initially partnered in November 2011; they launched an enterprise B2B solution in 2013.

To view the expanded list more than 30 partner banks and fintech partners, including their assets and the services they offer, subscribe to our fintech newsletter.