OH in South Park, San Francisco (or on Zoom from Big Sky, Montana): “OMG, crazy – that firm just paid 100x revenue to invest in [insert hot startup here] – what could they be thinking?”

When speaking with founders and private growth investors, we hear countless references to “multiples paid” on current or near-term revenue; both obsess over this because a higher multiple translates to a higher valuation.

For founders in particular, if a seemingly similar company to yours was ascribed 10x, 20x, 50x or 100x revenue, then why shouldn’t your company be, too? But much of the clamoring over why one company deserves a 10x vs 20x revenue multiple suggests that many see the multiple as only an input to valuation.

While multiples are indeed often an input for valuing mature, slower growing companies, in the private, high growth tech market, entry multiples tend to be a byproduct of the valuation process: What investors are really trying to understand are possible exit values. If a company is expected to be very valuable on a probability-weighted outcomes basis, the investor can afford to pay a higher entry valuation, and implicitly, a higher entry multiple. In other words, the ends (like the possible exit values) can justify the means (a seemingly higher present-day valuation).

To determine possible exit values for later stage companies, tech growth investors often focus on two key and interconnected questions: (1) How long could this company grow at high rates; and (2) What will its margin structure be over time? So while two companies might have similar revenue numbers today, their actual expected revenue, cash flow, and ultimate outcomes could be very different, depending on how investors answer these two questions… and therefore, those two companies ought to have different present-day valuations and multiples.

And in fact, the answers to these questions — runway for high growth and long-term margin structure — will be key factors in how companies are valued. Understanding these factors, as well as the role of multiples, can help tech founders and their teams focus on what matters during the valuation process, as they build and seek ongoing investment in their companies.

How valuation multiples work

Why did multiples become a shortcut-heuristic for estimating valuations in the first place? It starts with the complexity involved in valuing companies in general. Simply put, a company is worth the present value of its future free cash flows. But, accurately forecasting the size, timing, and risk of cash flow over many years can be incredibly challenging, so many investors often rely on valuation multiples as a proxy for determining what a company is worth.

A multiple is a company value divided by a metric. Two common public markets multiples are earnings multiples (price per share / earnings per share) and EBITDA multiples (enterprise value / EBITDA). While both earnings and EBITDA multiples are widely used, we often see investors in public and private technology companies resort to revenue multiples (enterprise value / revenue).

The most common reason to use revenue multiples is these quickly growing companies are either unprofitable or deemed to have “immature” margins that don’t reflect how profitable they’ll be in the future. A revenue multiple could therefore be viewed as a shorthand for an EBITDA multiple; for example, a company expected to have 40% long-term EBITDA margins could be valued at 25x EBITDA at scale; that 25x EBITDA is equivalent to 10x revenue (25x EBITDA multiple * 40% EBITDA margin).

Multiples are not only used to value companies today but also to value companies several years down the line. For example, in a discounted cash flow analysis, an investor would model cash flows for an interim period (typically 5-10 years) and then can apply a multiple at the end of the forecast period to estimate the terminal value (i.e., cash flows beyond that forecast period). For businesses that are unprofitable, breakeven, or modestly profitable, the interim cash flows in the forecast period tend to be inconsequential to company value, which is ultimately largely determined by this terminal value.

The conventional wisdom finance professionals are often taught is that you should not pay a higher multiple today than what you’d expect to be paid upon exit — that is, your entry multiple should equal your exit multiple. In that case, if we assume a normalized exit multiple is 10x forward revenue (depending on industry and company type, this could be higher or lower), you wouldn’t pay more than that today.

It’s the prudent assumption many make. However, this simple framework breaks down when applied to tech companies whose growth rates don’t look like that of a “normal” mature company. Imagine there is a hot, bottoms-up $60M revenue B2B software company raising at a $4B valuation. That’s a whopping 67x revenue. But the company expects to grow 200% to $180M in revenue in 2021, and 122% to $400M in 2022. In other words, the entry multiple could be looked at as 22x projected 2021 revenue or 10x 2022 revenue.

We think about this framework in the context of how long it takes to feel “in-the-money”, meaning the value of the investment is beginning to appreciate. In this case, at the end of 2021, we may feel “in-the-money” because our implied forward (2022) multiple will be “normalized” at 10x. Until that point, the investment is “dead money” (i.e., no appreciation in value). But assuming the company grows at a 40%+ compounded rate thereafter, we can overcome that 15 months of “dead money” and still generate 30%+ annual returns.

The sage advice often given is that an investor should pay for a valuation on the normalized 10x revenue today, not on projected revenue two years from now. Sure, investors would prefer to pay the lowest price possible. But if that company continues to grow at a very high rate, good returns are possible. In order for investors to feel comfortable paying higher multiples on today’s revenue, they need to be able to underwrite long runways of high growth and attractive long-term margin structures.

Where high growth runway comes in

As growth investors who believe in companies executing big, risky visions, we look at how long a company could grow at a high rate when assessing potential investments. This growth could be a function of product differentiation, go-to-market operations, sheer market size, new geographies, and expansion into adjacent categories.

An example of such a business is Salesforce, which defined a new category for SaaS and continues to be a benchmark for SaaS companies to follow. When Salesforce went public in 2004 as a new kind of CRM provider, its S-1 indicated the CRM applications market was $7B. Since then, the company has expanded its scope, earning $17B revenue (and still growing nearly 30% year-over-year) in just the last fiscal year alone. If an investor could have identified Salesforce’s ability to maintain such prolonged growth upfront, invested in its 2004 IPO, and then held on through to today, they could have made ~70x returns: equivalent to ~30% IRRs over a 16 year period. Not too shabby! Of course, as always, past performance is no guarantee of future results, and this example should not be relied upon when making any investment. But it’s indicative of the mindset and the powerful effects of growth persistence.

If a company grows at an elevated rate for a long period of time, investors can afford to pay what seems like a nosebleed multiple. This is because that growth rate can overcome multiple compression and still empower the company’s valuation to appreciate at a high rate.

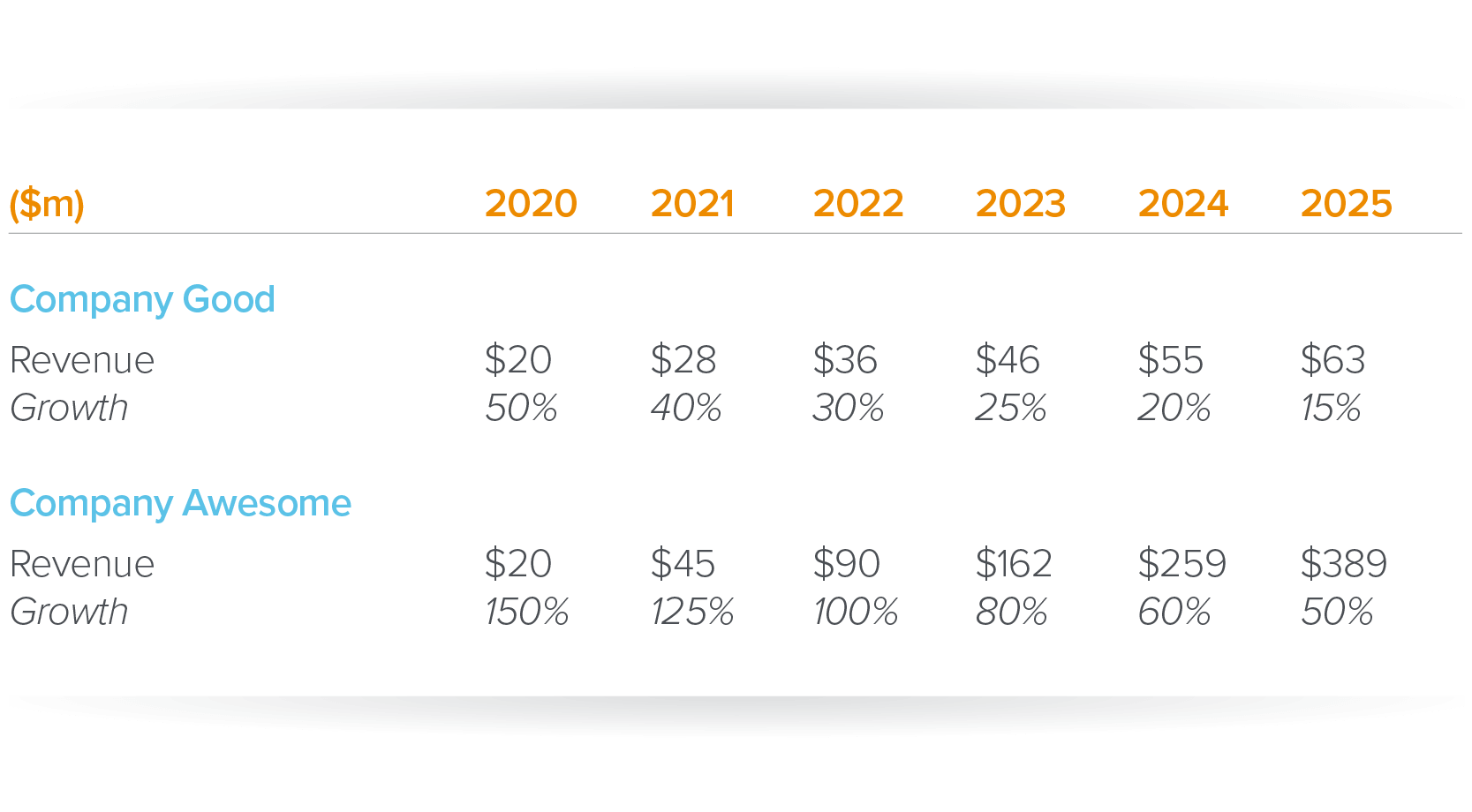

Let’s look at an example for how an elevated growth rate might play out from the time of investment to a potential point of exit. In the world of private tech companies, imagine two $20 million revenue companies that are largely identical: same revenue scale, same current and long-term gross margin and burn profile, same cash and debt on the balance sheet, same market. The only significant difference is Company Good is growing 50% year-over-year, while Company Awesome is growing 150%.

The management teams of both companies may want to be valued at 15x 2020 revenue — in other words, both companies would be worth $300 million. But would that be a good deal for the shareholders entering at this stage? Let’s assume the below is the probability-weighted likely scenario over the next five years.

If we believe both companies will trade at ~10x revenue upon exit in 2025, Company Good would be worth ~$630 million and Company Awesome would be worth nearly $3.9 billion. Ignoring dilution and balance sheet changes, Company Awesome would have made investors ~13x, while Company Good would only have returned ~2x. Because Company Awesome maintained growth at a much higher rate, its investors would have had a much better return.

These two companies should not have been valued at the same multiple at the time of investment. Had investors been targeting 30% returns over five years, Company Good should have been valued at ~$170 million or ~8x revenue at entry, while Company Awesome could have been valued as high as $1.05B, or ~52x revenue.

Where long-term margin structure comes in

Eventually, for almost all companies, growth rates start to slow down. Once growth approaches more moderate levels, the company will be expected to generate cash flow, and investors will talk about earnings, EBITDA, and cash flow multiples — not revenue multiples. As such, when evaluating a potential investment, we spend considerable time forming a view on what the long-term margin structure will look like: How many cents of cash flow will every one dollar of revenue yield?

In 2009, Workday had just 19% gross margin. Workday has two segments: subscription services (primarily software) and professional services. While subscription services gross margin was lower than we often target at 52% for a software business model, the overall company had a 19% gross margin because of the drag from professional services segment gross margin at -19%. In Workday’s early years, the company was professional services-heavy (46% of 2009 revenue) to get its enterprise customer base up and running properly. Not surprisingly, professional services tend to be concentrated at the beginning of customer deployment, so as Workday has matured, subscription has grown to 85% of revenue, as of the last fiscal year. Even though professional services still operate at a negative gross margin (-9% in last fiscal year), the subscription services is now in the mid 80%s and brings the overall gross margin to 70%+.

When private company investors invested in Workday in 2009, they would not have valued Workday as if it was going to be a <20% gross margin business forever with low cash flow generation potential. They likely thought about an exit outcome in which the business was at 70%+ gross margin and could consequently generate 25%+ free cash flow margins at scale; in the last fiscal year, Workday had 17% free cash flow margins while still growing 29%. (As before, past performance is no guarantee of future results, and this example should not be relied upon when making any investment).

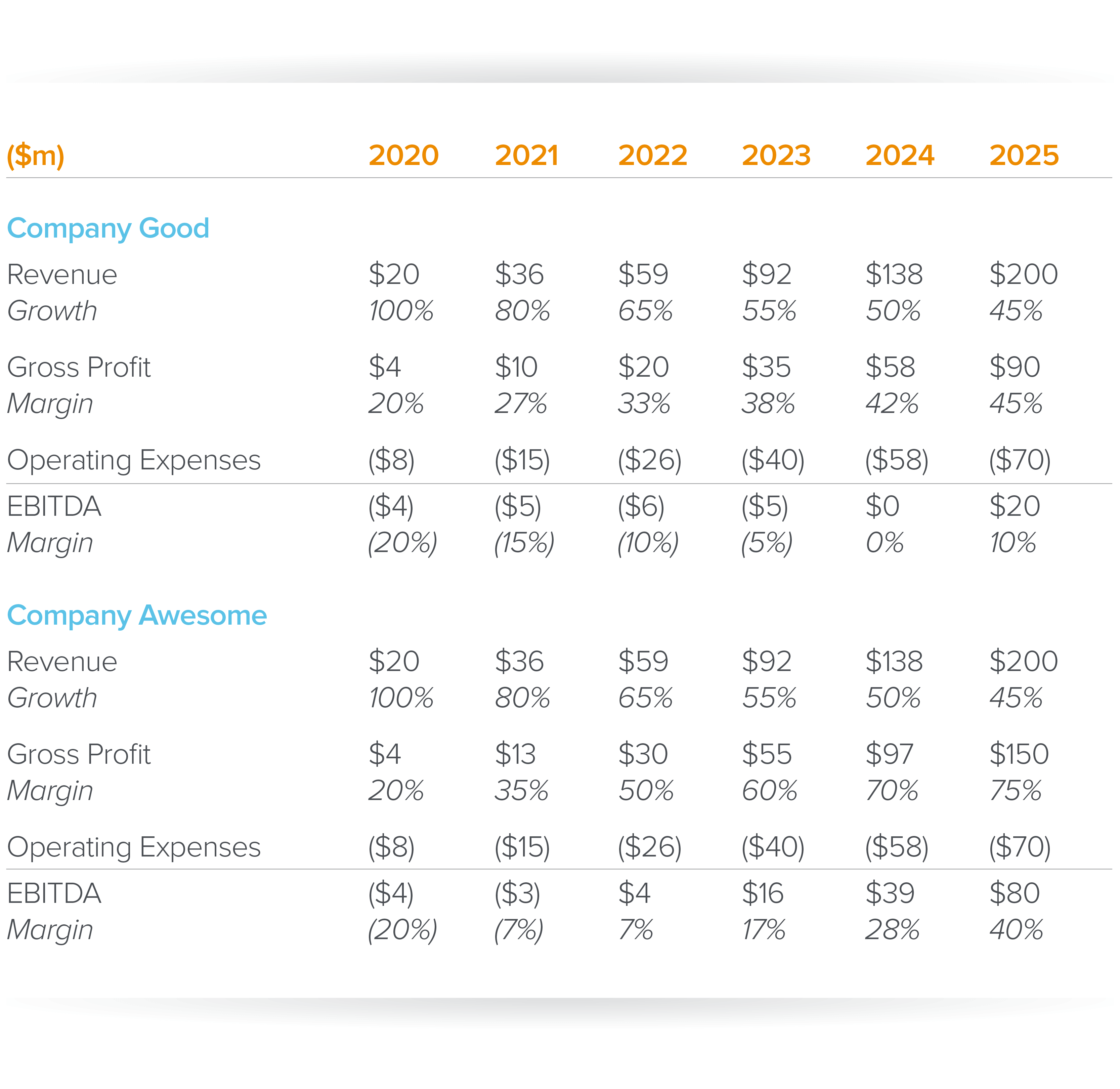

Let’s go back to our hypothetical of Company Good and Company Awesome, and change a different variable. Imagine two $20 million revenue companies that are largely identical — same revenue scale, same growth rate, same current gross margin, same operating expenses, same cash and debt on the balance sheet. This time, though, while the growth rates remain the same, the only significant difference is the core product for Company Good is software-enabled hardware, while the core product for Company Awesome is software.

Once again, the management teams of both companies want to be valued at 15x their 2020 revenue — in other words, both companies would be worth $300 million.

Would that be a good deal for shareholders entering at this stage? Let’s assume the below is the probability weighted likely scenario over the next 5 years.

If we believe both companies will trade at ~30x EBITDA upon exit in 2025, Company Good would be worth ~$600 million and Company Awesome would be worth $2.4 billion. Ignoring dilution and balance sheet changes, Company Awesome would have made investors ~8x while Company Good would only return ~2x. Because Company Awesome with its software business experienced much higher gross margin expansion, its investors would have had a much better return.

These two companies should not have been valued at the same multiple at the time of investment. Had investors been targeting 30% returns over 5 years, Company Good should have been valued at ~$160 million or ~8x revenue at entry, while Company Awesome could have been valued as high as ~$650M, or ~32x revenue.

Putting it all together: When to use revenue multiples, and when not to

Of course, figuring out potential long-term growth rates, margin structure, and exit outcomes for any one company is much more complex than this. But here are some questions and themes we often see come up around the topic of revenue multiples, and how we think about addressing them, since it can help founders and others not have to feel they need to rationalize their entry multiple, even just to quickly compare their company against another.

Clearly, founders should focus primarily on other factors as outlined above, but to share more on how investors think: We often pursue this kind of rationalization as a spot check, generally after going through the valuation process. When the multiple is implied, investors will then compare it to others seen in the public and private markets to get more comfortable. Think of it like a gut check, a way to determine if the valuation feels “reasonable”.

If you still feel the need to compare to other companies using multiples, there are a few alternatives to a simple revenue multiple. These don’t mean anything in absolute terms, but they can be helpful in comparing one company’s valuation to another’s.

Growth-adjusted multiples. Public markets investors often look at PEG ratios, which are P/E multiples divided by earnings growth. For high growth tech companies, we can examine revenue (or gross profit) multiples divided by their respective growth rates. Here’s an example: Solid Software Co.currently trades at 8x forward revenue, ~1/3 of the ~24x multiple that Incredible Software Co. trades — sounds cheap! But Wall Street expects Incredible Software Co. to grow ~80% over the next 12 months, 4x faster than Solid Software Co. at ~20%. On a growth adjusted revenue multiple basis, Solid Software Co. is actually more expensive at 0.4x vs. Incredible Software Co. at 0.3x, which may help Incredible Software Co. investors rationalize paying ~24x revenue (don’t ask us how to invest in Incredible Software Co.; this is not investment advice for either of these two hypothetical companies).

“Rule of 40”-adjusted multiples. These account for growth and cash flow margin: just take your revenue multiple, divide by rule of 40 score, and compare across companies.

Standard revenue multiples. At some point in a tech company’s life, these do become a useful shortcut for comparing relative valuations. This is typically when a company is growing ~50% or less, and there is greater clarity about long-term margins — as in, when it starts to look more like a “normal” mature company. In growth investing, this may be the point of “exit”, but this is not always the case.

While we do not care about entry multiples per se, we do dedicate a lot of effort to approximating a range of exit multiples. This may seem counterintuitive because we are forecasting a multiple 5+ years from now, rather than determining one for today. However, multiples are more relevant at that later point in time when growth has slowed to ~50% or less and long-term margins are better understood. For our analysis, we always apply a range of exit multiples to reflect the variability not only in growth and margin for that company but also to account for external market conditions.

Similarly, while companies are still in their early and fast-growing phases, we do encourage founders to think about their valuation as a function of a range of likely outcomes. If you’re a founder, and an investor tells you they can never ever pay more than 15x current year revenue, you should consider the mentality of that investor, and consider partnering with one who has the same long-term value creation view as you to ensure alignment in values. Ultimately, determining a valuation is a delicate balance between many factors. But if founders understand the mindsets and the math behind entry multiples, they are more likely to find the right long-term partner for their vision and company.

—